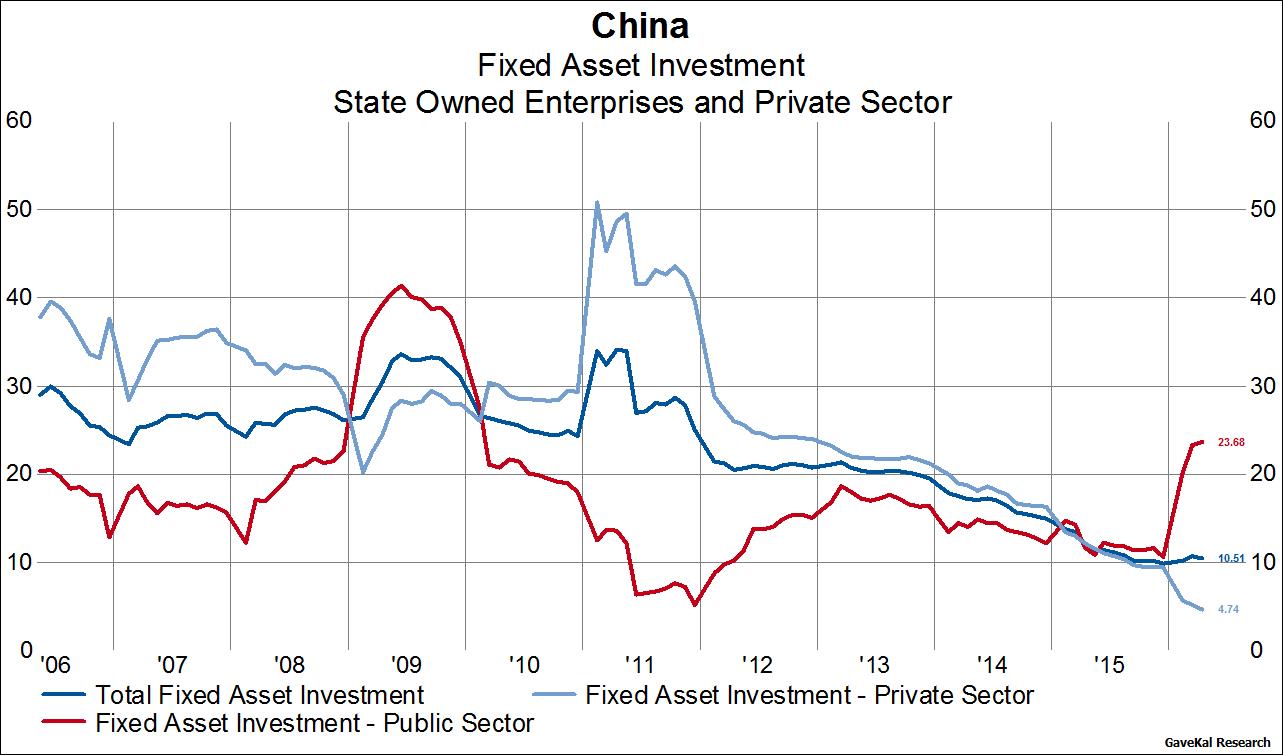

Over the weekend we got the monthly slue of Chinese data around fixed asset investment, credit creation, retail sales, and industrial production. Generally speaking, the data was soft, with misses in all categories. But one data point continues to stand out to us as evidence of the not-so-subtle involvement of government sponsored entities in the Chinese economy. That data point is Chinese state owned enterprises’ investment in fixed assets. It’s growing at a 24% clip as compared to private sector fixed asset investment growing at a 5% rate. Troubling as that may be given the known inefficiencies in government spending which suggests that much of this debt-funded investment will never provide a return on capital, it also highlights the Chinese government’s die hard reluctance to rebalance the economy away from fixed asset investment as the primary source of growth. Furthermore, these data also suggest Chinese over capacity is growing, not shrinking, which all else equal continue to exacerbate the deflationary trends already evident.