Unicorns Blowing a Bubble

by Sundara Krishnaswami

of HiddenLevers

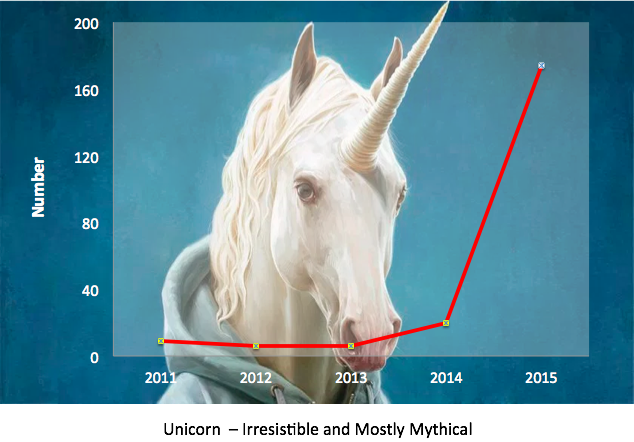

The number of unicorns (private venture-backed companies valued at over $1 billion USD) has ballooned in the past year to 174 from a mere six in 2013. The valuation is only a number given at a certain point in time, and like their namesake, these companies are meant to be rare and magical. So what’s the big fuss? According to several Unicorn founders, the term makes a positive psychological impact on their teams. “It absolutely gives us credibility and the ability to hire some very important people,” says Apoorva Mehta, CEO of Instacart, a web-based grocery delivery company.

Still it is only a number. Not a result. Not a plan. Not a certainty. Not even a high probability. Just a number that indicates potential.

Many startups seem to lose sight of this fact. They seem to focus more on valuations rather than customers and business fundamentals - especially competitiveness and profitability. They chase unrealistic scale ambitions and dilute capital efficiency through unacceptably high rates of cash burn. They disregard what the customer actually needs and wants, and miss out on fine-tuning their products and services to customer needs and wants. Some Unicorns, in their struggle to meet investor expectations on progress, are cutting corners on ESG, regulatory mandates and good business practices.

Precarious Unicorns

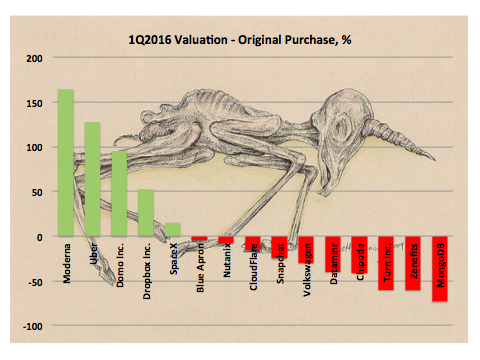

- Instacart. Valuation @ $2 billion USD

On-demand grocery delivery. They are losing money in an economy where the 1099 contract-worker model is thriving, and are reported to be “handing out dollars for 85 cents.” Recall that this category of startups led the way into the 2000 tech abyss.

- Jawbone. Valuation @ $1.6 billion USD

Consumer audio and wearable tech products. Even after 16 years in business, they have not yet delivered profits. While competitor Beats got acquired by Apple Computer for over $3 billion USD, Jawbone still struggles with strategy and execution. Suffering through cash flow and management issues, and accounts payable lawsuits, the company recently took a down round, with its valuation cut in half.

- Snapchat. Valuation @ $16 billion USD

Social media platform with auto-destruct messages and video. With little revenue to show for all its traffic and buzz, the company saw its valuation drop by 25% in 2015. Now back up to its previous high, in its most recent funding round, the company was unable to sell shares at a higher price after a year of growth.

- MongoDB. Valuation @ $1.2 billion USD

Open-source data analytics. The startup doubled in headcount, now with 400 employees. Their category is saturated and competitive, and the company is still struggling to arrive at a sustainable business model. Its valuation has dropped by 75% since 2013. Even with a recent 20% uptick by big investor Fidelity, the startup is still well below even its 2015 standing.

- Theranos. Valuation @ $9 billion USD

OTC blood-testing. This was supposed to be the next big thing in inexpensive disease detection, and is a great hope for cutting medical costs. As opposed to a valuation reduction due to stumbles in core business, this embattled startup is on the brink of ceasing operations for regulatory hiccups. The Centers for Medicare + Medicaid Services are revoking the company’s federal license because it’s facilities present an “immediate jeopardy to patient safety.” Walgreens, a key account, has threatened to walk out, taking with it the main the startup’s main revenue source, and taking valuation likely to zero.

- Flipkart. Valuation @ $ 13 billion USD

Wide ranging e-commerce platform for Indian market, a la Amazon. Among other strategic errors, India’s highest valuation startup has flip-flopped on trying to force shoppers onto its app instead of mobile web, and is losing top-level executives daily. It has gotten a 15% write down in the past 6 months.

- Gilt Groupe. Valuation @ $ 250 million

Flash-sales fashion e-commerce. Sold for a fraction of its private market valuation ($1.25 billion USD) to Saks, Gilt had raised a total of $286 million USD, which means that the founders walked away with nothing. The whole flash sales category has come undone since its heyday, and Gilt was lucky to have an exit at all. Amazon’s MyHabit, a Gilt clone, is shutting down in May 2016 completely.

- DropBox. Valuation @ $10 billion USD

Cloud-storage. Valuation has dropped by 28% since September 2015 amidst reported revenue growth problems and signs that market for its business is cooling off. They keep a gleaming $100k chrome panda statue in their lobby as a sign of Silicon Valley extravagance that must not be repeated.

Zenefits - Posterchild for Unicorn Don’ts

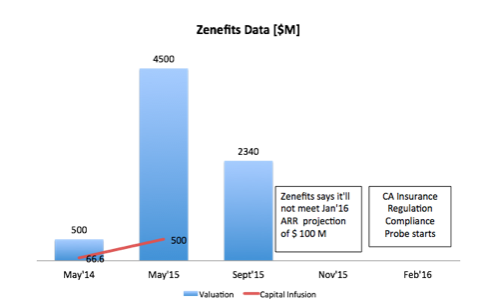

Zenefits started like a rocket, with fundamental competitive advantages. It built a zero-cost HR services offering of as a pathway to attract a wide customer base. It then monetised this customer base as a direct insurance marketing channel and made revenue off the insurance commissions. Great on paper, but the execution of its business model was hasty and flawed. Zenefits chased a fast dollar and cut corners on integrity. A huge venture capital infusion led to over-hiring, money being wasted on office entertainment, rampant unlicensed insurance brokerage and a repulsive work culture.

Today, the startup is under investigation for regulatory violations, and faces high employee turnover and low morale. It has fallen well short of its $ 100 million revenue projections and investors have cut their valuation by 60%.

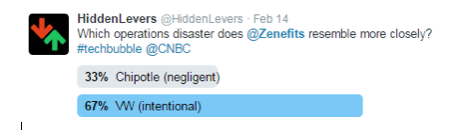

Culpability is what is at issue here. Is the pressure on high growth-potential startups leading to careless mistakes, like the Chipotle food scare or worse, leading to wholesale unethical conduct a la the Volkswagen emissions scandal?

Volkswagen manipulated their diesel car emissions to pass mandatory tests while the cars actually emitted emissions up to 40 times the legal limit. They got caught. Their shares fell 33%. Chipotle faced the challenge of e-coli and norovirus breakouts last year at its restaurants with a number of its customers falling sick across the country in a short span of time. The problem has been traced to lax food safety controls. Their shares plunged 47 %.

HiddenLevers conducted a Twitter poll on Zenefits culpability. 67% of respondents thought the ethics problem of Zenefits is more like the Volkswagen scandal. 33% compared Zenefits’ problems to Chipotle.

Even well-run companies make mistakes. Startups are particularly vulnerable to them. They do not have in place the mature processes and systems needed to effectively, efficiently and ethically support their drive to catch the rainbow.

And now, in 2016, we may begin to see unicorns implode due to their depleted cash reserves, ho-hum revenue growth, and no more investors holding a safety net.