First Quarter Market Commentary

In mid-January we felt compelled to send out a blast-email to our clients based on the volume of calls and concerns related to the bouts of volatility which roiled stock markets the first few weeks of the year. We certainly empathize with our clients’ very real concerns. Our empathy stems from the fact that in today’s hyper-connected world with media outlets “screaming” headlines to attract eyeballs, it is nearly impossible to separate fact from narrative.

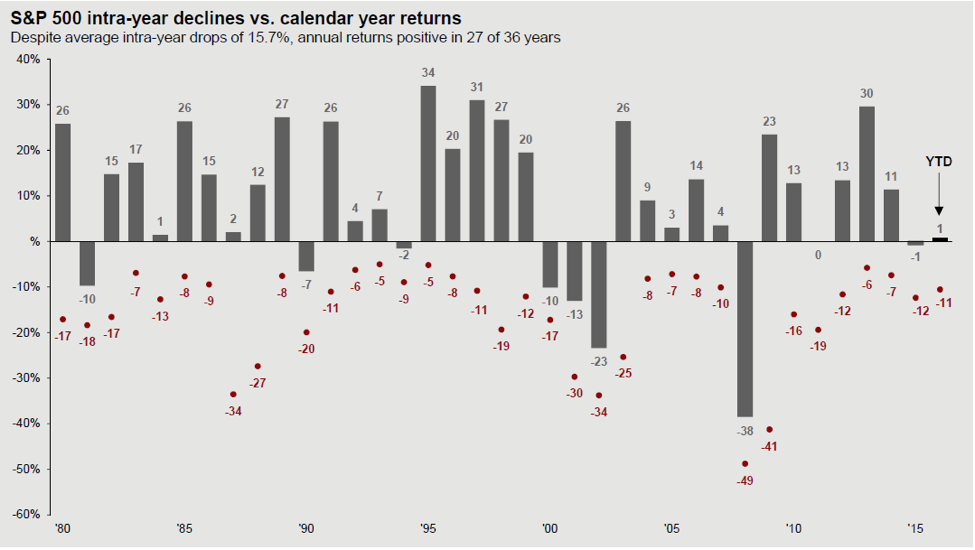

The point of our mid-January blast e-mail was simply to remind our readers that 10% market corrections are well within the historical norm and are not anomalies. Nor do they portend recessions. We have included the updated graphic we sent out in January below, which includes our most recent dip. This chart spans nearly 36 years. Note that there have been four economic recessions over this period.

The recently released Bureau of Economic Analysis US Gross Domestic Product estimate shows that the economy expanded at 0.50% in the first quarter this year. Keeping in mind that this is a preliminary estimate which will be revised approximately two months hence, we have already perused several declarations of a stalling economy in various financial media outlets. Oh how memories are short! Initial estimates of Q1 GDP last year were of a contraction of 0.70% (later revised to a contraction of 0.20%). In 2014, the advanced estimate for Q1 was 0.1%--though this estimate was later revised down. In all, US GDP has averaged just over 2.10% for the last four years. We see no evidence that this year will depart much from the trend line. GDP is a backward-looking mechanism, with a poor record of forecasting market returns.

There is both good and bad news in the most recent data. We feel we have spent a lot of time in recent months battling negative media headlines to focus on the underlying fundamentals. Lest we appear to be “cheerleading” equities, we will start out by pointing to some areas of concern. First, business investment (business spending) logged its worst quarter since the economic expansion began in 2009. Much of this decrease in spending can be traced directly to the malaise in the oil markets as capital spending on structures (shafts and wells) and equipment has ground to a halt. This spending (largely financed) has represented a large portion of capex for the previous seven years or so. Secondly, demand from overseas and a strong US dollar through much of 2015 has also taken its toll on corporate profitability, which also affects corporate spending. The Dollar has actually relaxed against the Yen and the Euro so far this year, but as we pointed out a year ago—it can take time for currency effects to make their way into corporate income statements. Last year’s Dollar rally has clearly hit earnings thus far into Q1 releases.

We expect to see the price of oil begin to stabilize later this year—a process which may include revisiting recent lows. Since oil production in the US has been significantly curtailed (and with many of the numerous smaller producers in, or entering into bankruptcy) the important task of working off the excess inventory begins. We will eventually return to price equilibrium in a year or two (our guess, $50-$60 per barrel). In general, while corporate spending is an important component to GDP, it pales in size to spending by consumers—and is a more volatile and often transient component versus consumer spending.

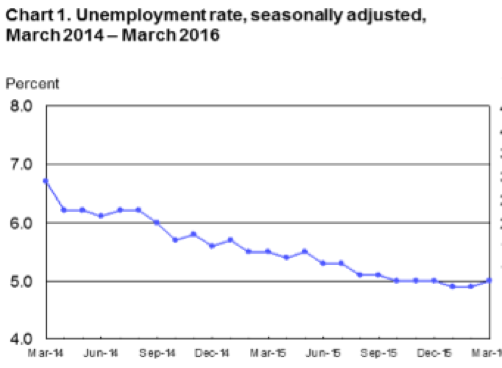

Now for the good news. A funny thing happened on the way to recession last quarter…the US economy created 628,000 net new jobs according to the Bureau of Labor Statistics. That’s a roughly 10% increase over the 570,000 jobs gained for the same period a year ago. As we have mentioned in these pages before, it is consumer consumption which bears the greatest impact on GDP, so we think it crucial for jittery investors to understand that as flawed as the unemployment rate calculations are, this measure of job growth continues to move in the right direction! The unemployment rate in the US stands at 5.0% as of the end of March, having ticked up slightly from the 4.9% level in January and February. Interestingly, the uptick is cited by the BLS as a result of more people looking for jobs (the labor participation rate has concurrently risen slightly as chronically unemployed people reenter the work force by looking for work). Of course being employed is generally a condition of being a full contributing unit of economic output as a consumer.

In mid-March we spoke with a client who relayed anecdotal evidence of an economic slowdown through his conversations with his patients discussing their reluctance to spend due to their perception of economic uncertainly. He was contemplating stepping back from the markets in-part due to this “evidence”. We are glad he didn’t—not least due to the markets’ returns since that conversation. To us, however, this smacks of the “narrative” that has at times accompanied the recovery from the depths of the 2008 financial recession and seems to tempt investors to abandon their investment strategies when even normal bouts of volatility arise.

For evidence of consumer health and spending, consider the returns of the Dow Jones US Consumer Services Index (populated with companies like Amazon, Disney and Home Depot) of the Dow Jones US Consumer Goods Index (i.e. Proctor & Gamble, Nike, Ford). Both indexes have outperformed the S&P 500 over the last 1 and 3 years and widely outpaced the broader NYSE Composite Index. With equities being a leading economic indicator of growth, we surmise that consumers have been active throughout the recent quarters and the jobs numbers give us reason to remain optimistic. Our larger point is simply to beware of the prevailing short-term narratives that accompany bouts of market volatility—and focus on the facts that matter.

Non-US:

As further evidence of how the “narrative” can infect our investment strategies rather than inform them, recall the panic surrounding the Chinese economy from about August through this January. The worst-case scenarios had China in a melt-down, bringing the rest of the world with it (including the US) into a new global recession. Year-to-date, the MSCI Emerging Markets Index is up 5.71% through the end of April! This index’s largest country exposure is to China (23.37%), with close neighbors South Korea and Taiwan rounding out the top three (at 15.37% and 11.62% of the index, respectively). We are neither suddenly bullish on China, nor emerging markets per se, but we do believe in mean-reversion. We remind investors that the slowing of China’s economy to a long-run sustainable equilibrium is both old-news and a necessary condition of their continued progress to economic development.

Data released late last month by Eurostat showed the eurozone’s GDP rose by 0.6% versus the fourth quarter 2015 and by 1.6% versus the first quarter of 2015. European markets reacted to negative global growth developments last year even more than US markets—but it appears that Eurozone growth is picking up while the US shows the slightest signs of slowing. The recapitalization of European banks along with the ongoing monetary stimulus should continue to support this trend.

“Throw The Bums Out”

The correlation between market returns and election outcomes are a common topic during election years. We have been asked for our forecast of the market’s reaction several times in the past months. We admit to being a very interested political observer—in fact we would even have described ourselves as passionate not long ago! Perhaps age or experience has dampened our enthusiasm. More likely, it’s the current crop of presidential candidates which has us scratching our head. In some ways—the 2015-2016 election season has been surreal (and remains so). Our clients span the political spectrum and feedback seems to indicate that both parties seem to have outdone themselves in turning off mainstream American voters. Our only prediction is a low-turnout election.

“Democracy is the theory that the common people know what they want,

And deserve to get it good and hard”

-HL Mencken

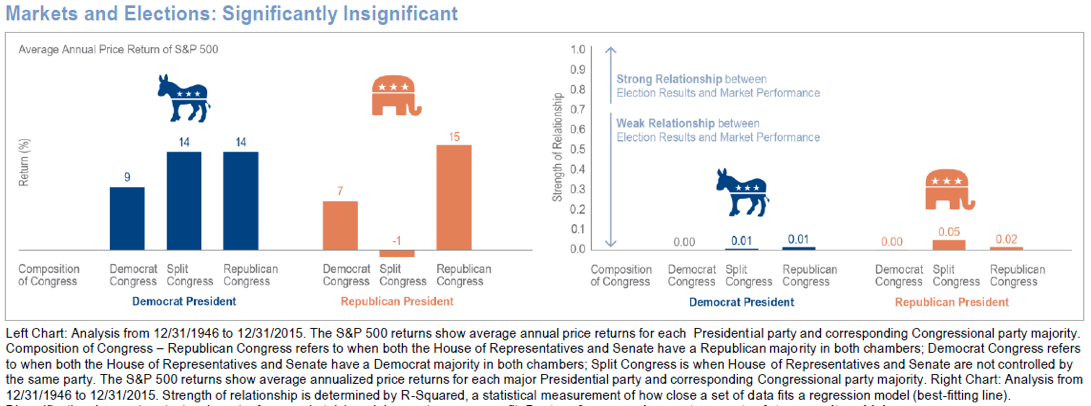

A lesson we have re-taught ourselves repeatedly over the past decades is that while policy is important, few presidents get to enact their political promises unmolested by the co-equal branches of government. Correlations between the party-in-power (whichever it may be) and market outcomes are spurious at best. Indeed, this relates to our earlier comments about being distracted by “narrative”. We chuckle at the promises of certain celebrities threatening to move to Canada if (fill in the name) gets elected. Truthfully there are some we really wish will follow through. Unfortunately—abandoning an investment strategy is much easier to do than fleeing your US citizenship. We strongly urge our clients to apply a large discount to theories of what will happen to the markets or the economy if the election turns out in a particular way. Goldman Sachs has done extensive quantitative research on the topic of political composition of the US government and US equity market returns. Their conclusion: “[w]hile data may appear to suggest a strong relationship between party composition and market returns, closer analysis reveals a failure to meet the basic standards of statistical significance in both sample size and strength of relationship. As always, be cautious of political averages”.

The source of market volatility over the last 8 months has been the confluence of slowing global growth, rising rates here in the US, turmoil in China and the commodities markets. We DO NOT attribute market volatility to today’s bizarre election gyrations. We expect commodities and China to eventually stabilize, and we expect more Fed rate hikes ahead. In short, because the source of volatility will remain with us for some time, so will the volatility. Staying focused on the relevant economic facts should keep investors invested during this period to experience positive, if temporarily muted portfolio returns.

In mid-January we felt compelled to send out a blast-email to our clients based on the volume of calls and concerns related to the bouts of volatility which roiled stock markets the first few weeks of the year. We certainly empathize with our clients’ very real concerns. Our empathy stems from the fact that in today’s hyper-connected world with media outlets “screaming” headlines to attract eyeballs, it is nearly impossible to separate fact from narrative.

The views are those of CCR Wealth Management LLC and should not be construed as specific investment advice. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and, when sold or redeemed, you may receive more or less than originally invested. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Investors cannot directly invest in indices. Past performance does not guarantee future results. Securities and Advisory Services offered through Cetera Advisors LLC. Registered Broker/Dealer, Member FINRA/SIPC.

Cetera Advisors LLC and CCR Wealth Management LLC are not affiliated companies.