KEY TAKEAWAYS

- The recent surge in oil prices from the recent multiyear lows has raised concerns on the impacts for the U.S. consumer.

- Examining consumer spending activity in the past 18–24 months does not suggest an impending dramatic change, however, barring a return to oil prices of $100 per barrel.

The 75% run-up in oil prices from the multiyear lows hit in mid-February 2016 has raised concerns that the U.S consumer may run for the hills. However, a look at what consumers actually did over the past two years as oil prices fell more than 70% (from nearly $110 per barrel in mid-2014 to just above $25 in early 2016) can help us better understand what consumers may do now that energy prices could be on the way back up.

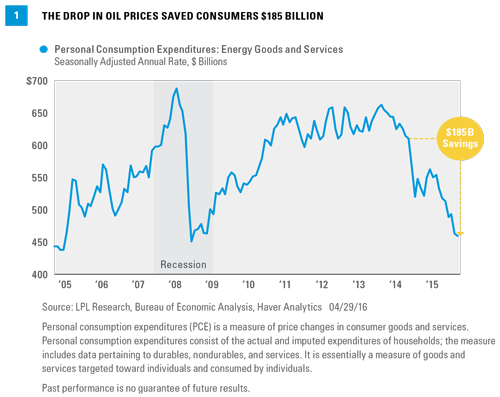

The U.S. consumer, which accounts for more than two-thirds of U.S. economic activity, spent an annualized $459 billion on gasoline and other consumer energy products (home heating oil, natural gas, etc.) in March 2016, $185 billion (or 29%) less than they spent in June 2014[Figure 1]—aided by the 47% drop in gasoline prices between June 2014 and March 2016. What did consumers do with all the money they saved? The conventional wisdom was that consumers would pocket the savings at the pump and head to the mall, on vacation, or perhaps to the nearest new car dealer. Consumers did go out and spend some money on nonessential items; but they also took on some more debt, and even saved a little, as measures of consumer sentiment soared. Sound familiar? This kind of activity is similar to the behavior in the early stages of recovery following the Great Recession, suggesting that consumers may still be reeling from the recession and its aftermath, and perhaps also believed that the drop in energy prices was only temporary.

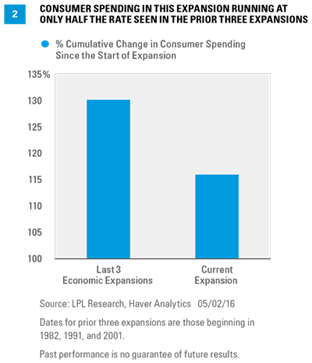

The big drop is gasoline prices did not, as some expected, provide a big lift to the overall economy or the consumer sector, which continues to struggle in this recovery, nor did it change the overall tepid pace of consumer spending. In fact, since the end of the Great Recession 27 quarters ago (the second quarter of 2009), consumer spending has only increased by a cumulative 16%, well under the 30% gain in the first 27 quarters of the last three economic recoveries, which are the most comparable to today’s recovery [Figure 2].

Supports and Constraints

Roughly six months after oil prices peaked in June 2014, our expectation was that although the drop in gasoline prices would be a plus for spending, other factors would likely have a much bigger impact on the consumer, given that gasoline accounted for only 4% of personal spending.

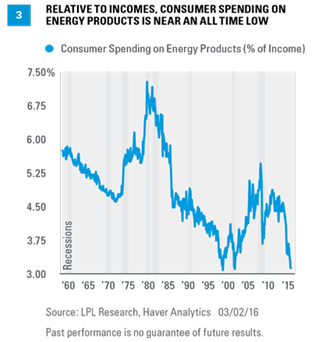

The good news is that the better tone to the labor market, the sharp rise in household net worth, and a return to prerecession levels of confidence have all acted as supports for the consumer. In addition, the precipitous drop in consumer energy prices over the past 18–24 months has left the share of consumer incomes dedicated to purchases of energy at 3%, matching the all-time lows hit in the late 1990s and early 2000s, providing even more cushion for consumers in the coming quarters if energy prices were to suddenly spike higher [Figure 3].

However, wages and disposable income have a far bigger impact on consumer spending than any of the positives listed above. Although growth in both has been improving, it remains stubbornly weak, and thus a key constraint on spending. Some of the sluggishness in wages can be traced back to the dramatic drop in energy production that led to widespread job cuts in the typically high-paying petroleum industry.

In general, although the big drop in consumer energy prices was a plus for consumers, at just under 4% of overall consumer spending (around $459 billion), the category just isn’t large enough to move the needle on overall consumer spending, which is currently running at over $12.5 trillion. But will consumers respond to higher energy prices by spending less on other items?

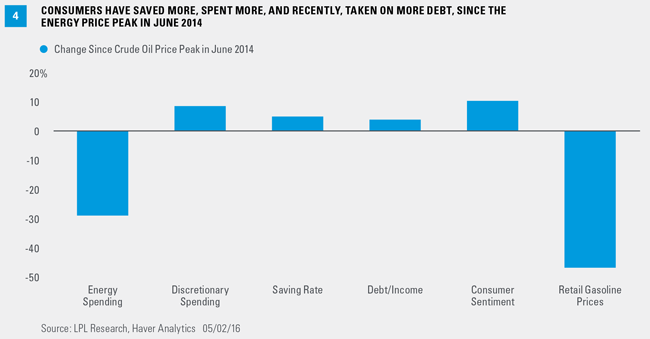

Figure 4 details the percent change in several key consumer categories since oil prices peaked in June 2014:

· Consumer spending on energy

· Consumer spending on discretionary items

· Consumer savings rate

· Consumer debt-to-income ratio

· Consumer sentiment

· Retail gasoline prices

Largely Consistent Behavior

The big drops in energy spending (29%) and gasoline prices (47% drop) stand out and dominate Figure 4, warranting a closer look at what happened to consumer sentiment, discretionary consumer spending, the saving rate, and consumer debt levels. The drop in energy prices has coincided with a sharp rise in consumer sentiment, which is hovering near a 12-year high. While falling energy prices likely played a part here, other factors (better labor and housing markets, etc.) also contributed to the rise in consumer sentiment. Consumer spending on discretionary items like cars, movies, televisions, and vacations increased by nearly 9% from June 2014 through March 2016, but not by as much as the 10% rise in consumer sentiment.

Consumers also increased their saving rate modestly, perhaps sensing that the drop in energy prices was only temporary. The rise in the saving rate is a comforting sign for the health and durability of the economic recovery, providing the consumer with some additional “dry powder” in the later stages of the expansion that could help cushion against future shocks to consumer spending. One potentially negative consequence for consumers (over the longer term), however, is that the drop in energy prices has coincided with a noticeable run-up in the debt-to-income ratio, as measured by consumer credit outstanding to disposable income. To be fair, other widely followed measures of debt-to-income ratios have shown only a very modest uptick, but if sustained, this is perhaps an unforeseen consequence of the big drop in oil prices.

In many respects, aside from taking on more debt, consumers really did nothing different in the past 18–24 months than they did in the early stages of the recovery from the Great Recession, when they also both spent and saved more than they had during the Great Recession. Looking ahead, barring a return to near $100 per barrel oil prices, we continue to see consumer spending running at around two-thirds of its normal pace, supporting gross domestic product (GDP) growth between 2.5% and 3.0% for the remainder of 2016.*

*Our forecast for GDP growth of between 2.5–3% is based on the historical mid-cycle growth rate of the last 50 years. Economic growth is affected by changes to inputs such as: business and consumer spending, housing, net exports, capital investments, and government spending.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.