This title was my favorite takeaway from a conference I attended in Cincinnati recently. I don’t know who to credit it to, but the cynical formula is quickly being absorbed into the investment world’s body of insider jokes.

Smart beta products are only as smart as the investor who uses them. They are tools. I once saw one of Ernest Hemingway’s Royal Quiet Deluxe typewriters, and it was beautiful, but it was important because Hemingway knew what to do with it. Today, many smart beta products are presented without instruction manuals – some marketers don’t think they need one – and it is possible investors will pay the price.

I want to remind our readers that before they were called “smart beta”, dumb beta strategies in the right hands saved American retirees hundreds of millions of dollars in the 1990s and 2000s. Even more surprising, the geniuses weren’t the Wall Street investment banks, but public servants who learned the issues and made sensible decisions. Michael Lewis would have a difficult time making this into a book.

The first and enduring success story came as many of America’s largest pension funds began to use the MSCI Europe, Australasia and Far East (EAFE) Index funds for their first investments in stocks outside of the United States. This was a turning point for global investing as the offshoring of retirement assets accelerated quickly following the fall of the Berlin Wall in November 1989. The awful trap laid then was that buying the EAFE Index in 1990 involved sending a significant portion of investments into what was recognized (correctly, in hindsight) as an equity market bubble in Japan. It took a lot for teams of public fund investment officers to fight the growing tide of skeptics who claimed that plain capitalization weighting was naturally the best approach in increasingly efficient markets. Those that did saved pension funds huge sums of money as a result over the next decade as the Japanese equity and real estate bubble burst.

Leading pension fund investors adopted what came to be known as “Japan-Lite” mandates, which came in several different forms. Instead of blindly loading up on what ultimately became over 60% of the MSCI EAFE Index in the beginning of the 1990s – a multiple decade peak in the exposure – these Japan-Lite investments capped the Japan weight typically in the range of 25%-35%. Not enough people appreciated what that act of common sense investing did to spare pension assets – as Japan experienced the lost decades of growth that followed.

The thoughtful use of smart beta approaches produced similar success stories during the Tech bubble of the late 1990s. The Russell 2000 Growth Index (small cap US equity) became dominated by Internet darlings, nearing 60% weighting in technology stocks in 2000 (compared to 21% at 12/31/15). Capping exposure to the tech sector mitigated serious damage during the tech bust from 2000 to 2003. Fewer funds acted on the concentrations in banks in most equity indexes that grew during the housing bubble of 2006-2007, but that was again an opportunity for smart beta to instill a value discipline during speculative periods. Today you will find ETFs that invest in emerging markets that have the term “capped” in their name – this is a smart beta version of the normal capitalization weighting that adjust for large concentrations of single names or sectors within developing markets. Incidentally, most of those concentrations were in commodity-oriented companies and industries, making the smart beta tool very useful over the past several years.

We have been using a smart beta concept called “revenue weighting” in the management of a portion of LMCG Global MultiCap (GMC) strategy for over 5 years. We believe this concept will continue to be one of the best tools for generating returns in the next 10 years as it has been for the past 30. Like the “Japan-Lite” approaches in the late 1980s, revenue weighting does something simple and smart; it ensures a degree of valuation discipline. If you take all the companies you buy in an index and add up the value – not of their stock price – but of the sum of their revenues – you have an objective starting point for investing based upon an important fundamental - company revenue. Japan’s capitalization weight grew to over 2 times its revenue weight at its peak. Today, it is a fraction of its revenue weight. The strategy has worked well for us these past 5 years, primarily because it involved buying more of countries which were oversold (Europe of late) and less of others.

Today, the revenue weighting approach is giving us a new and potentially important insight. How does our own US equity market look in terms of value relative to markets around the world? The period between 2007 and 2015 captures the beginning of the financial crisis to present day. We know now that this past 8 years, the S&P 500 Index has outperformed the non-US indices handily. But is it because our economy is so much better or that investors are paying a big premium for the stability of the United States?

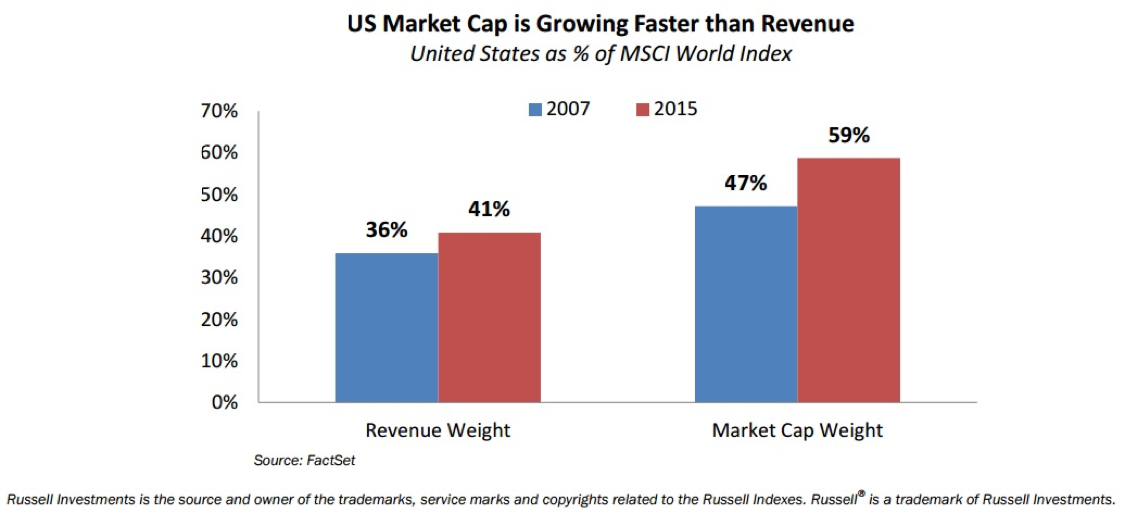

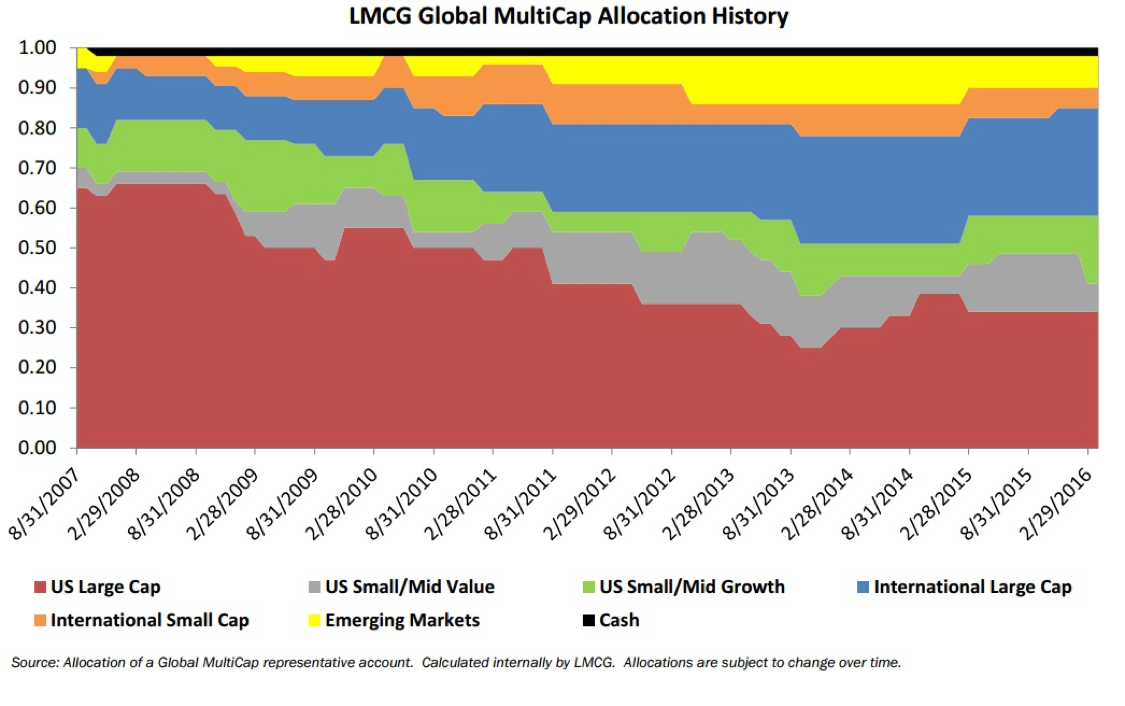

We believe it is the latter. The chart above demonstrates that from 2007 to 2015, US revenue weight as a percentage of the total MSCI World Index has grown by 5%, from 36% to 41%. However, the weighting on a market cap basis has grown by a whopping 12%. So the answer is from this measurement that, yes, US companies were able to grow their revenues faster than the rest of the world, and investors are paying much more for their revenues as a result. This is one of the reasons we have moved the weighting of US companies down over the past 5 years to current levels in Global MultiCap (see graph below), and why we say that a conservative, long term investor will not be putting money back into the US market, but will be searching for better value elsewhere. The allocation decision is critical in terms of our potential to add value verses the MSCI ACWI IMI Index – and ultimately the S&P 500 Index. Evaluating revenue weights compared to market cap weights is an important component that we believe allows us to allocate our clients’ capital to more attractive areas of the market. You should be skeptical about marketing claims of smart beta, but smart investors can use these strategies for both important insight and, hopefully, real profit.

The opinions herein are those of LMCG portfolio management, are made as of the date of this material, and are subject to change without notice. There is no guarantee the views and opinions expressed in this communication will come to pass. It is for discussion purposes only, since the availability and effectiveness of any strategy depends on each client’s facts and circumstances. The information in this commentary was obtained from sources believed to be accurate, but we do not guarantee that it is accurate or complete. It is provided for informational purposes only and was not issued in connection with any proposed offering of securities.

Copyright © 2016 by LMCG Investments, LLC. All rights reserved