Long term readers are familiar with our ownership of Berkshire Hathaway (BRK) shares, as well as our undying respect for Warren Buffett and Charlie Munger. They have few peers among the best stock pickers and capital allocators in U.S. history, as measured by the returns on Berkshire Hathaway over the last 51 years. On April 30, 2016, faithful shareholders gathered as Mr. Buffett and Mr. Munger shared copious and wise advice at the 2016 Berkshire Hathaway Annual Shareholders Meeting. Ironically, almost every topic was connected to hyperactivity. We attended the meeting, and came away with some thoughts that are somewhat contrarian, including some of his views we found disappointing.

- Hyperactivity in Investment Management

During the meeting, Buffett explained in detail how expenses are the enemy of your investment portfolio. He used the eight-year results of a bet he made where he pitted a low-cost S&P 500 Index against a multi-layered list of top hedge funds. It showed that the high expense levels overwhelmed the aggregate investment selections of the hedge fund managers after including their annual fee of 2% and then taking 20% of the profits. The deficit they achieved was greatly impacted by the results of the hidden cost of trading in the individual hedge funds, something that long-term readers know we have argued are as damaging to most money managers as annual fees.

- Hyperactivity in Mergers and Acquisitions

Munger called Valeant Pharmaceutical's business model a "sewer." He and Buffett had warned that using borrowed money to acquire healthcare companies hyperactively and then stripping their research and development budgets was a “short-term momentum favorite and a long-term loser.” Munger described the severe price increases as "immoral." Buffett added fuel to the conversation by calling them "chain letter" companies.

We think of it more as "bigger fool theory." You need a bigger fool to come after you to perpetuate the excitement. Valeant ran out of buyout candidates to continue their pyramid scheme. In the past, Buffett has explained chain letter companies and other manias as being like Cinderella, saying, "At midnight, it all turns to pumpkins and mice." Many high price-to-earnings favorites look like "chain letter" stocks to us when so much of the wealth that gets created is in stock price appreciation and appears disconnected from the profits of the business.

One blogger of the meeting said this: “Warren Buffett couldn't care less about those who have struck it rich in the frenzy of IPO activity in recent years.” Staying true to his oft-cited advice for the average investor seeking long-term growth, Buffett gave the verbal equivalent of an eye roll to anyone who tries to game the market.

Buffett stated that the unusually large position that the Sequoia Fund took in Valeant was a mistake and says that the business model of Valeant was enormously flawed. Both Buffett and Munger shared that from their long experience in business, they can spot patterns that frequently lead to bad outcomes, and Valeant displayed those patterns and trends. We would argue that those investors who seek a high margin of safety must avoid all of these kinds of investments, even the ones which have worked so far like Tesla and Amazon.

- Hyperactivity in Hail Storms and Car Accidents

Buffett explained that poor underwriting results in the first quarter came from hyperactive hailstorms and dramatically higher than usual auto collision numbers nationwide. He also explained how hyperactive competition in reinsurance caused him to sell Munich RE and Swiss RE. He went on to show how enormously the overall Berkshire insurance business has grown in the last fifteen years and how erratic it has been from year to year. To us it looks like a good example of where one may feel compelled to move hyperactively in and out of Berkshire Hathaway only to miss out on the real wealth creation.

- Hyperactivity in Stock Buy Backs

A question came up concerning stock buy backs on Berkshire Hathaway shares. The company has stated it is willing to buy back shares at 1.2 times book value or lower. Munger reminded everyone that hyperactive stock buyback programs, unrelated to price considerations, are unhelpful to shareholders. Buffett only favors buys below intrinsic value, which are theoretically useful to shareholders.

- Hyperactivity in Chasing Yield

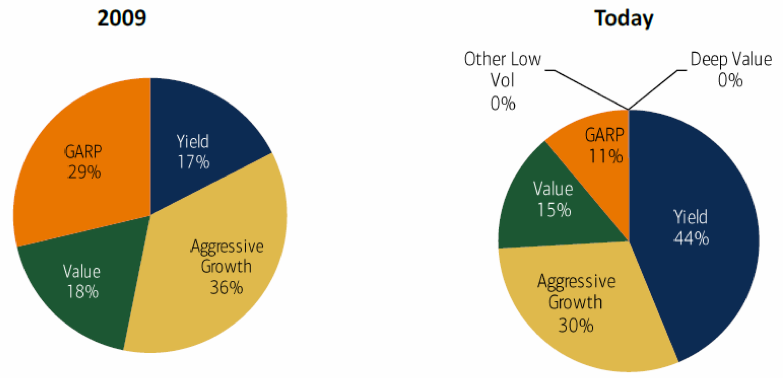

Buffett explained how difficult the packaged food business is getting. According to ValueWalk, “The most interesting part of the answer was not specifically about how 3G operates, but Buffett’s quip that the volume trends in the package goods industry are not looking particularly strong.”1 To us, this says something about confidence being placed in a wide variety of staple companies in the S&P 500. The chart below tells the story:

Source: Merrill Lynch report March 30, 2016; What Investor’s Want

We believe there has been hyperactivity among investors chasing dividend stocks and paying high price-to-earnings multiples among staple, industrial, energy and other companies to get at those dividends.

- Hyperactive Affection for Hyperactive Revenue Growth

While Buffett and Munger warned investors about being envious of winning IPO investors and other tech darlings, investments Munger called "lottery" winners, they venerated Amazon and heaped praise on their CEO, Jeff Bezos. Buffett described a reverence for Amazon, despite the negative effects that has had on anyone in retailing. He also complimented what he called "pull" marketing, as practiced via Amazon Prime memberships. We don't disagree with Buffett and Munger that Amazon has been amazing in its revenue growth, market share and $109 billion of annual sales, but we are shocked that they made no mention of the price-to-earnings ratio of Amazon and the fact that they have been one of Munger's lottery winners.

We remember Buffett and Munger telling us in shareholder letters and at prior annual meetings about what makes a business great. They said, "A great company CEO goes to a mirror and says, “Mirror, mirror on the wall, should I raise my prices this fall?” The mirror replies, “Why wait?" Amazon seems to only cut prices and the cost of delivery to gain market share and requires investors to believe in a sales growth story tied to a rising stock price.

Even the annual fees from Amazon Prime get burned up in the cost of delivery. Amazon is happy to report that Prime members buy way more stuff on way more occasions than they did before becoming a member. As Buffett extolled, it gets you huge market share and makes life miserable for anyone who competes with them. In our case, Nordstrom and eBay have been negatively impacted by the momentum Bezos has created. Our concern is that respect for manager genius is closely tied to stock price increases, not profits. Apple and Tim Cook were much more respected a year ago at $140 per share than they were at $93 on May 2, 2016. In years past, even Buffett and Munger were excited about the CEO at BYD, a Berkshire holding that makes electric car engines in China. They were noticeably silent on that subject this year.

- Hyperactive Faith in CEOs

Buffett and Munger described that they had people come hyperactively to sell them on investing in Valeant based on the genius of their CEO, Michael Pearson. He was adored by many highly thought of value investors and was a rock star when Valeant's stock rose to over $200 per share in 2015. Let it be said, that we at Smead Capital Management want to avoid ascribing higher and higher intelligence to CEOs based on stock price performance. If anything, “Pride goeth before a fall.”

- Hyperactive Populist Politicians

Buffett seems to be afraid to confront hyperactive populist politicians on their ridiculous regulatory witch hunt with banks like Bank of America and Wells Fargo. The Berkshire boys kind of mumbled something to the affect that these banks don't have as good of a business as they used to. Did he and Munger mention what it would mean if the politicians found a new whipping boy? Or did they explain what normalized economic growth and higher interest rates would do to bank earnings? The answer was no.

- Lack of Hyperactivity in Existing Holdings

Buffett and Munger also seem very hesitant to sing the praises of portfolio holdings like IBM, American Express, Bank of America and Coca-Cola. All he said was, "these businesses aren't as great as they used to be." If Buffett doesn't believe in these companies, we believe he should sell them to someone who does and redeploy the capital elsewhere. If he believes that time will be the friend of these former stalwarts, he should point out what it will look like when finicky investors could chase them higher if and when they produce better results in the future. We think he believes they will be good investments and think he should cheerlead those like he does Geico, Mid-American Energy and the other private holdings.

Warm Regards,

William Smead

1 Source: ValueWalk, http://www.valuewalk.com/2016/05/berkshire-hathaway-2016-annual-meeting-recap/2/

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

©2016 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com.

Follow us on Twitter @SmeadCap