Introduction

In 1817 David Ricardo wrote Principles of Political Economy and Taxation in which he outlined the theory of competitive advantage. He describes an England that excels at producing textiles and a Portugal that produces the best port wine in the world. He observes little trade between the two countries, suggesting that both countries are devoting resources to producing both clothes and wine. He wonders whether the welfare of both England and Portugal would be better off if each focused on what it was best at and engaged in trade. Given its geography, or factor endowment in the parlance of economics, Portugal had a natural advantage producing wine. Given its superior technology—harnessing the steam engine—England had a natural advantage producing textiles. He called these comparative advantages and suggested that a country should identify what it was most-best at and least- best at, and then divert resources away from the things they are least-best at and allocate more resources to what they are most-best at. So his prescription was for England to focus on the production of cloth and Portugal to focus on the production of wine. Then both countries should trade freely. The end result would be greater total output, productivity and income for both England and Portugal.

Over time, as countries identify their comparative advantages, they try to organize their economies around them to maximize economic growth. This endeavor to re-organize an economy in an attempt to maximize its comparative advantage leads to economic growth as resources are directed to the most productive use. Due to an abundance of cheap labor, China has had a comparative advantage producing manufactured goods and has spent the last 20 years restructuring its economy around manufacturing. This had positive spillover effects for most other emerging markets. China—and most other emerging markets—experienced a huge Ricardian growth surge over the last couple decades, best illustrated by the sustained increase in global trade.

But, Ricardian growth can hit limits, if for example, the comparative advantage of a country is exhausted. If China’s comparative advantage is principally low-cost labor and state directed finance, then as that low-cost labor and cheap credit is exhausted, the country’s comparative advantage slowly disappears. Given global linkages, this has negative consequences for other emerging and developed economies. How do we know where we are in the process of this Ricardian growth dynamic?

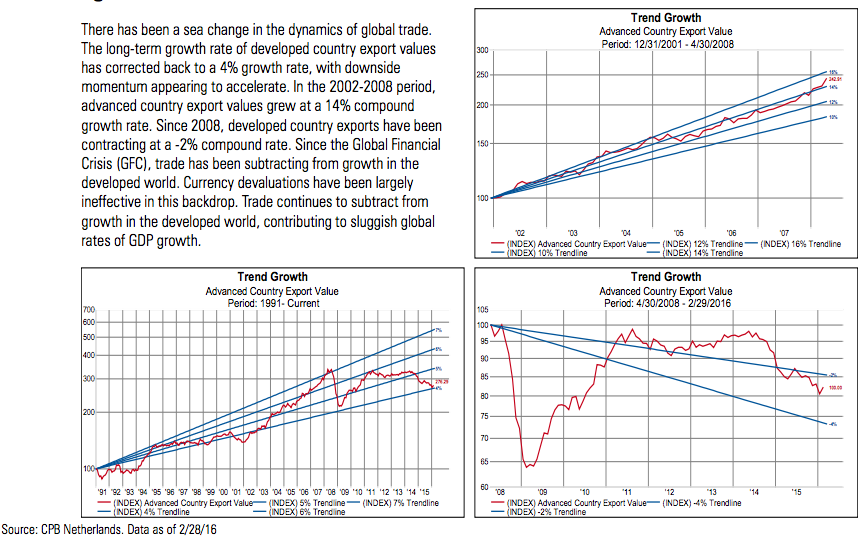

Observing global trade is one place to start. A deterioration in trade values and volumes would be great evidence to suggest Ricardian growth has run its course for this cycle. Unfortunately, recent trade statistics reveal a very clear sea change in the global trading environment. With commodity prices collapsing, export values around the world are deep in negative territory. Illustrating the demand deficiency, cheaper prices are not leading to increased volumes—representing a positive elasticity to demand. Rather, volumes are contracting also. Together, weak export values and volumes suggest the modern era of Ricardian growth may be over.

This quarter, we explore the hypothesis that the modern era of Ricardian growth has ended. We further explore what this means for asset allocation and which types of stocks in particular should do well in this Ricardian hangover.

The End of Ricardian Growth?

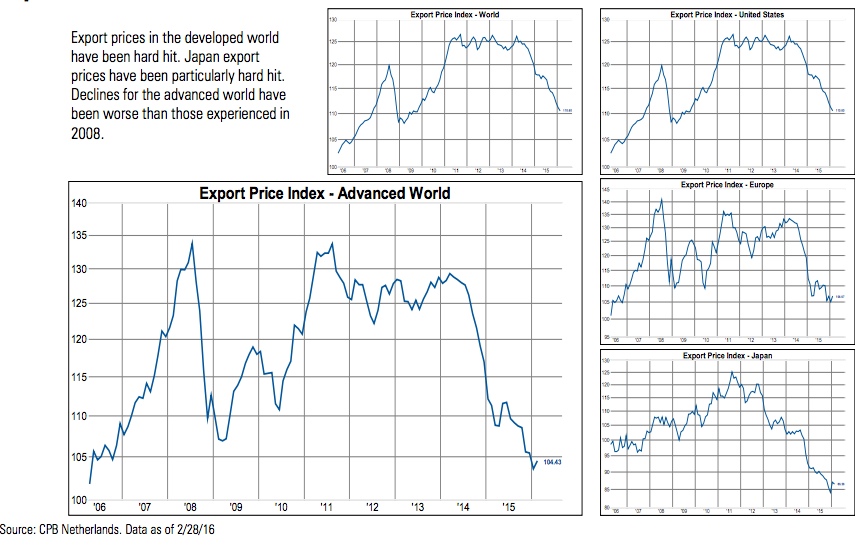

Export Prices Have Tumbled Around the World

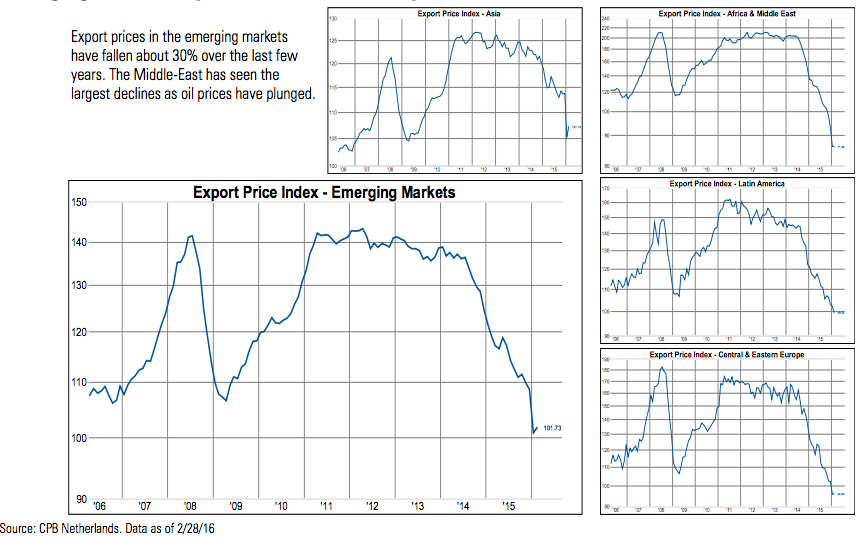

Emerging Market Export Prices Have Really Suffered

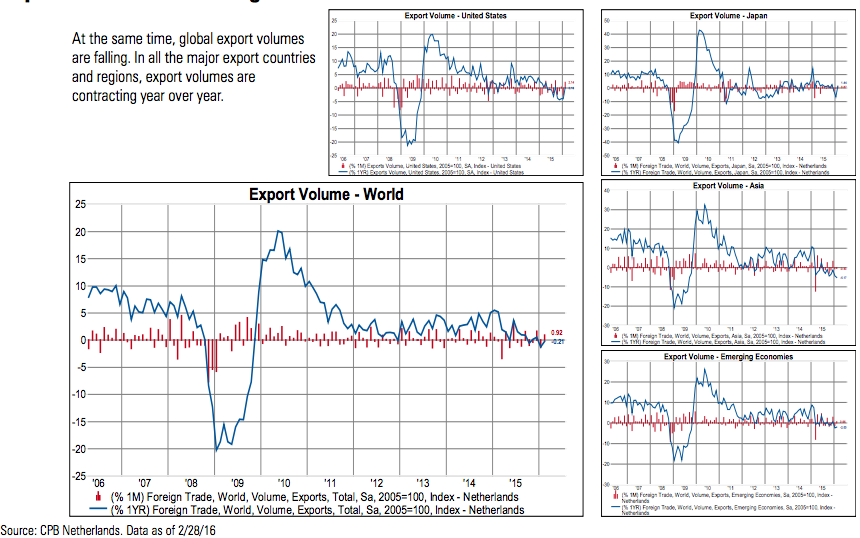

Export Volumes Are Falling Too

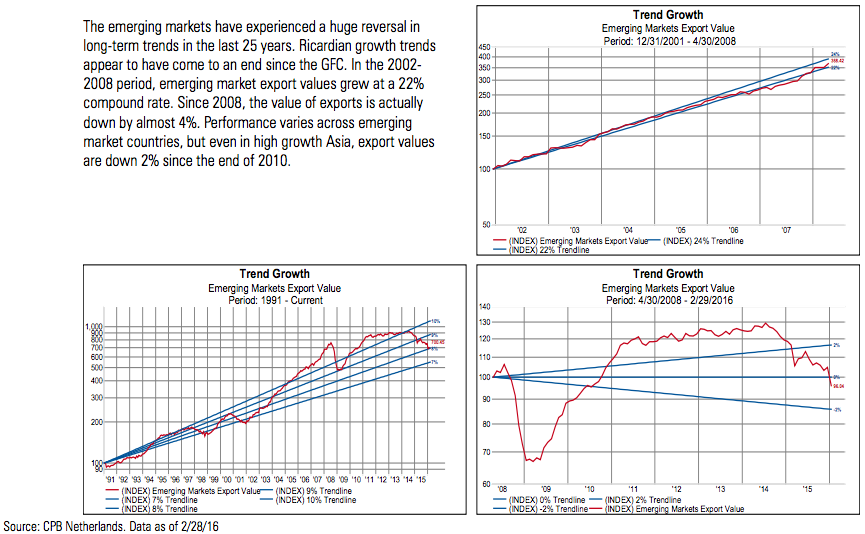

Sea Change in Global Trade

Ricardian Growth Hits the Wall

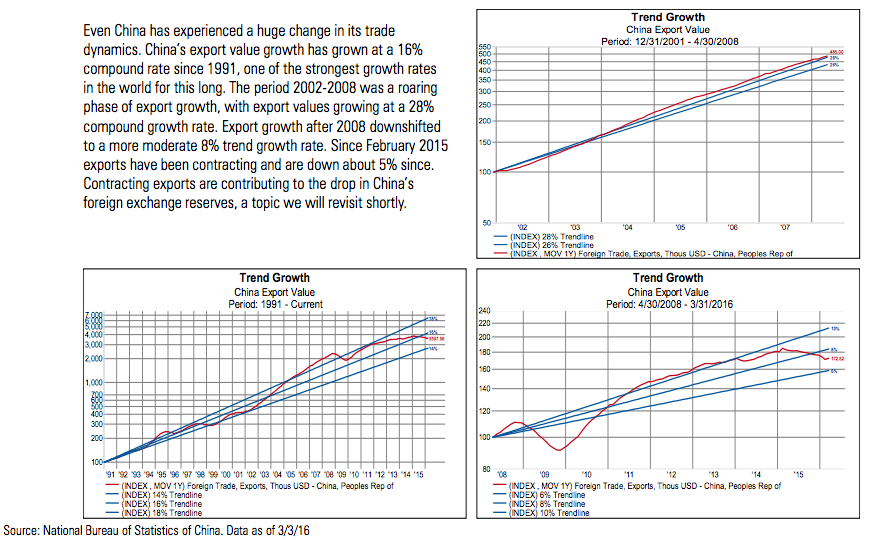

Trade Has Even Gone into Reverse in China

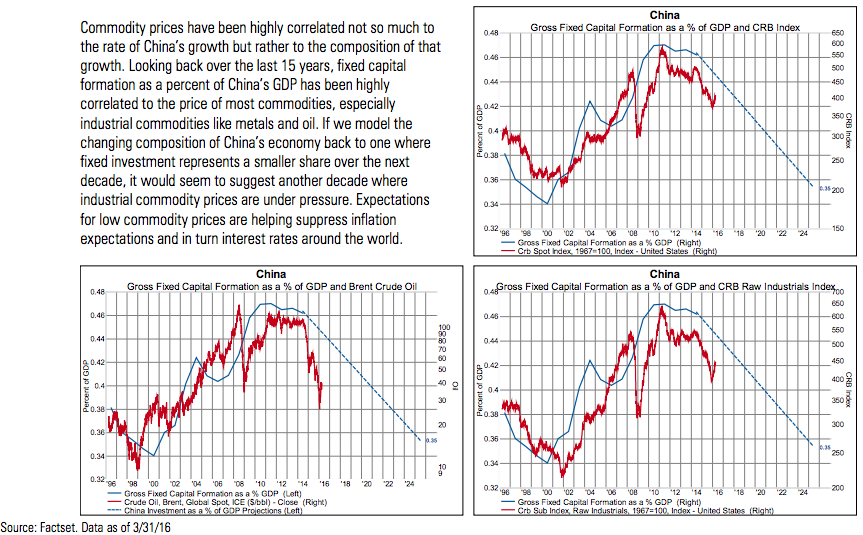

China’s Long-term Rebalancing Could Depress Commodities for Years

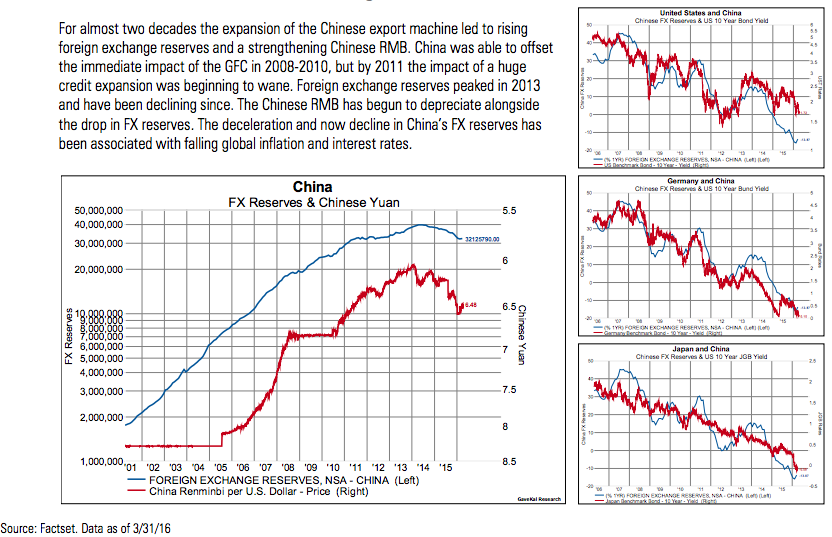

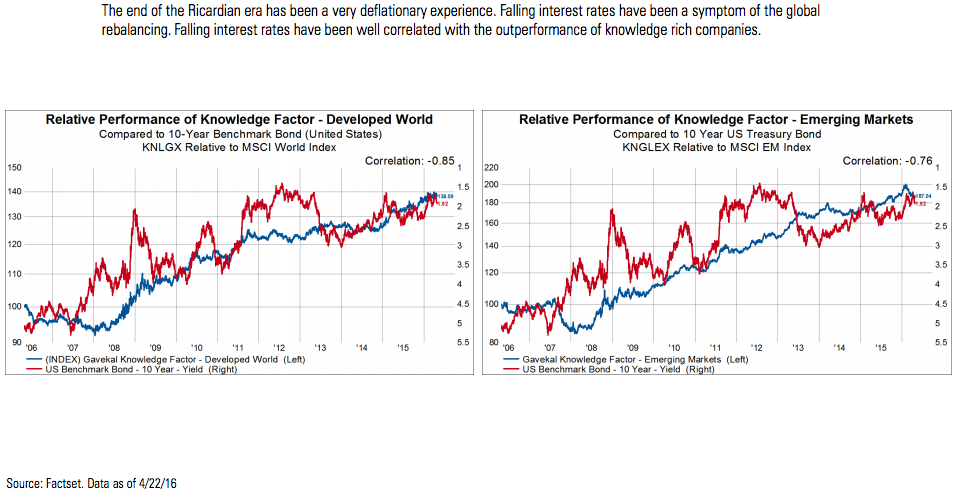

The End of Ricardian Growth is Driving Interest Rates Lower

Which Direction for the US Dollar?

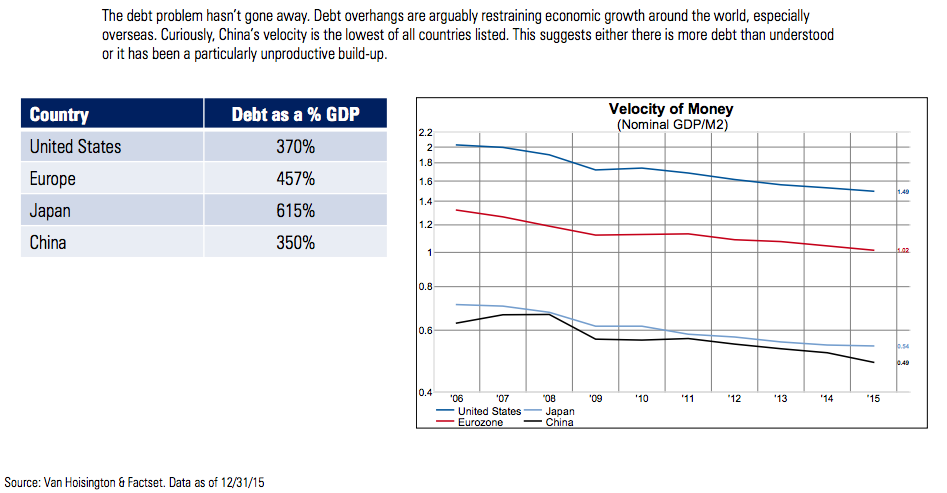

Global Debt Levels are Still Elevated While Money Velocity is Low

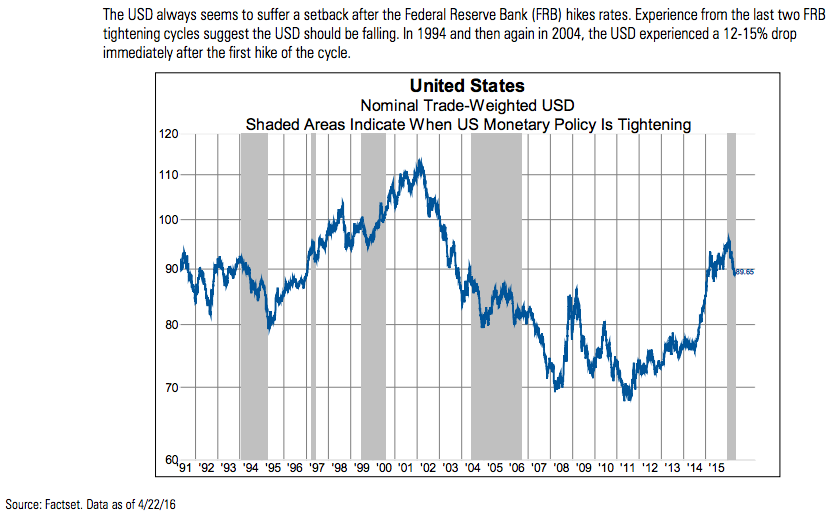

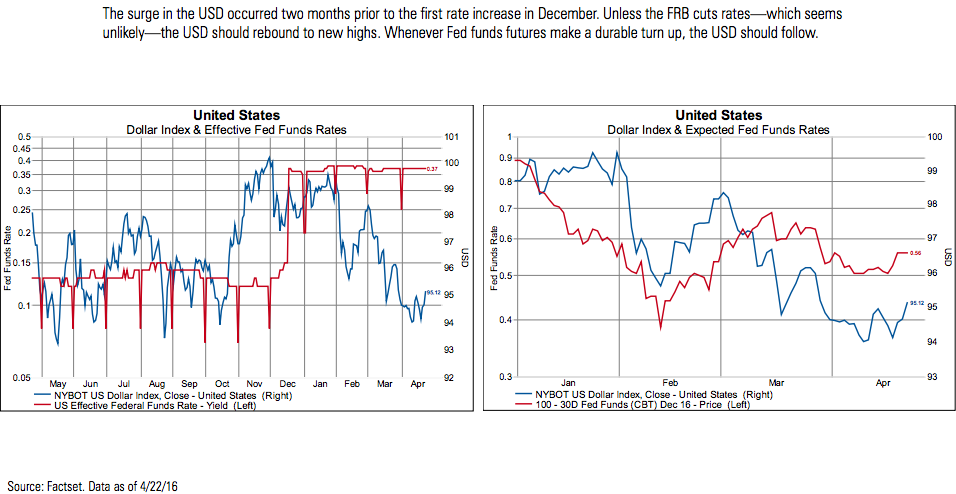

Is the US Dollar Correction Over?

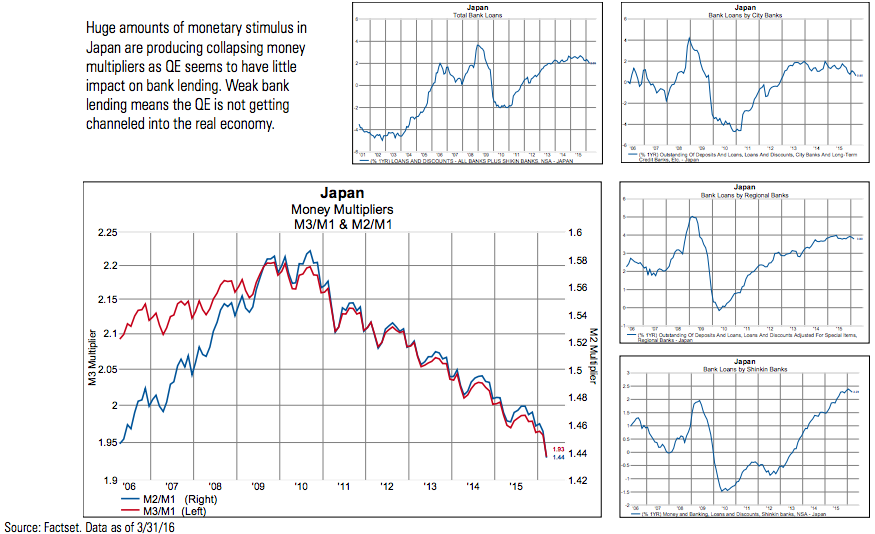

Credit Multipliers Continue to Plunge in Japan

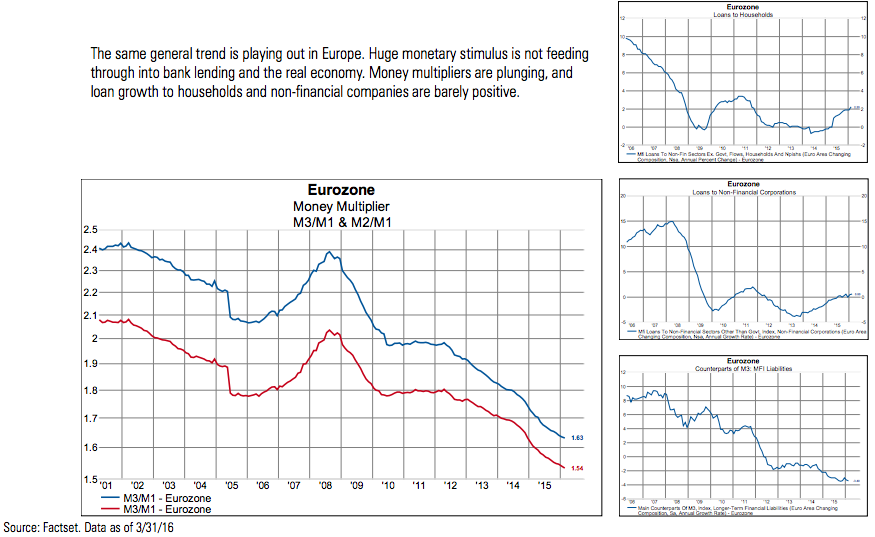

…and in Europe too, while Bank Loans Stagnate

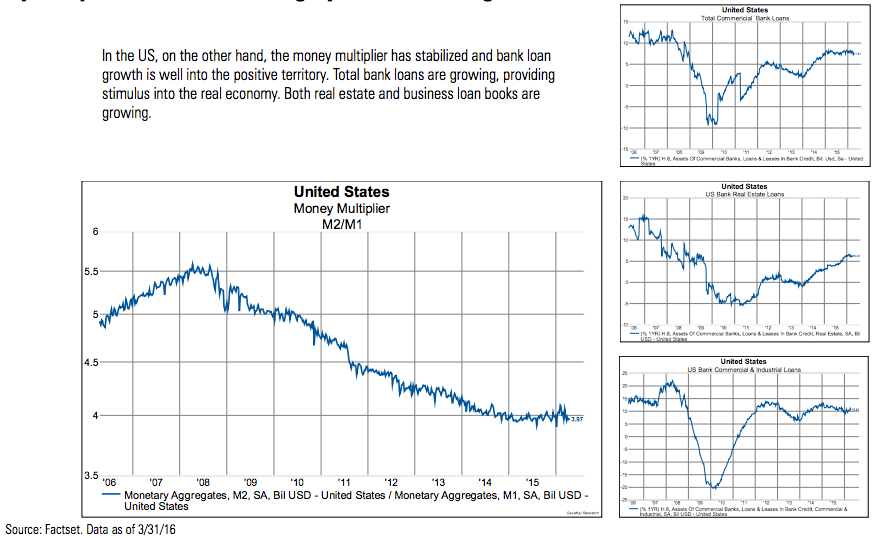

By Comparison the US Banking System is Creating Credit

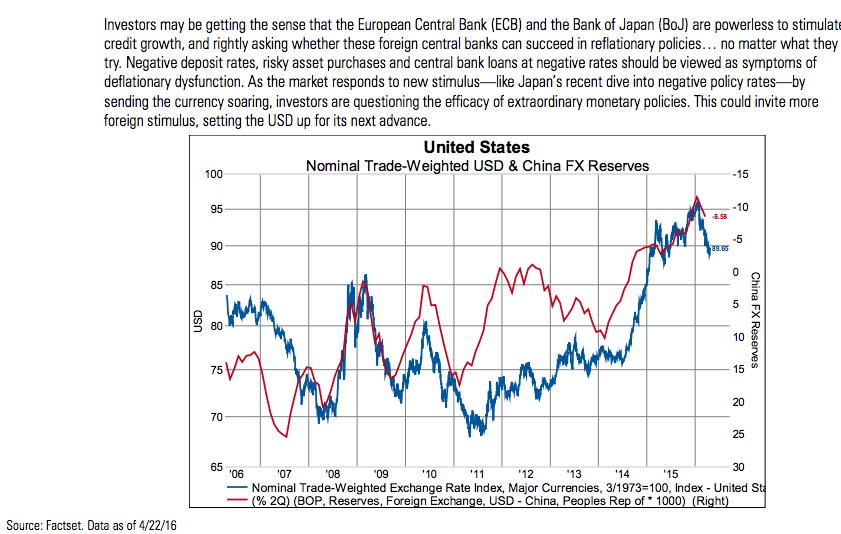

China’s Rebalancing is Overwhelming the ECB’s Bazookas and the BoJ’s Arrows

Rates Support a Stronger USD

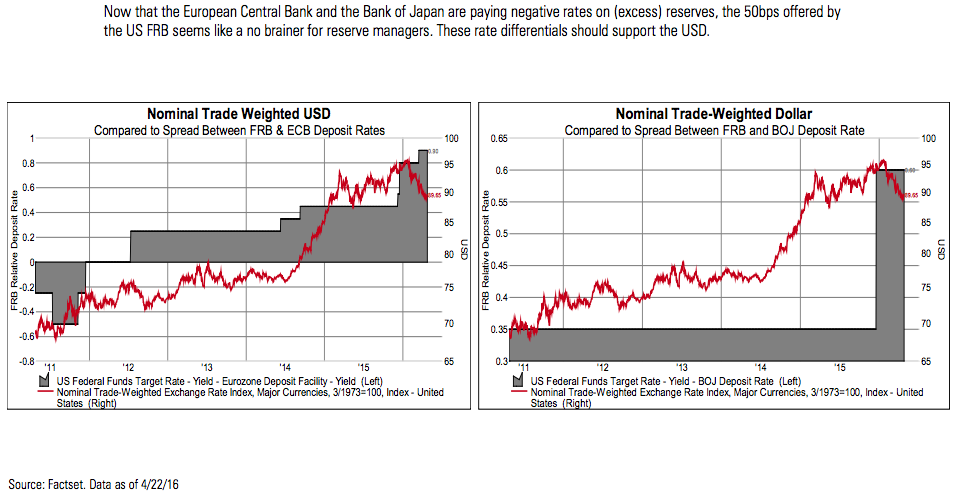

Relative Deposit Rates Favor the USD

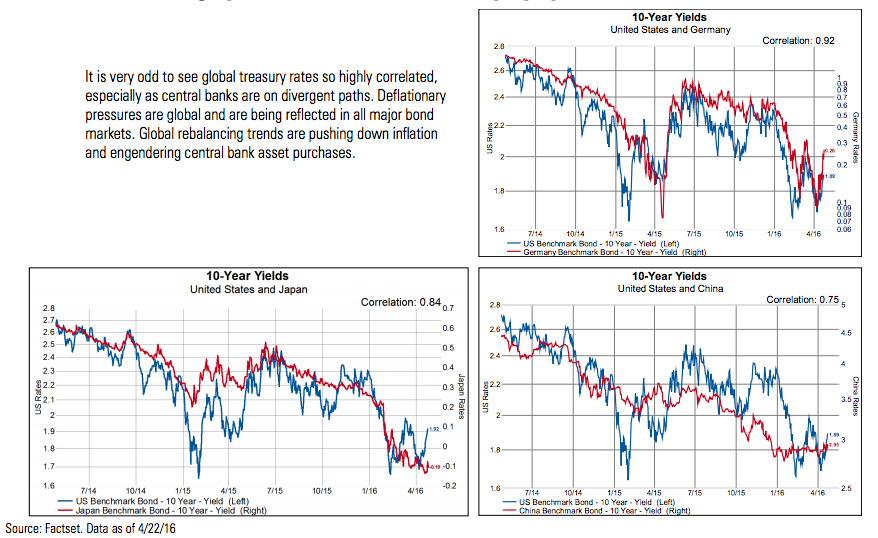

Global Bonds are Highly Correlated…a Deflationary Symptom?

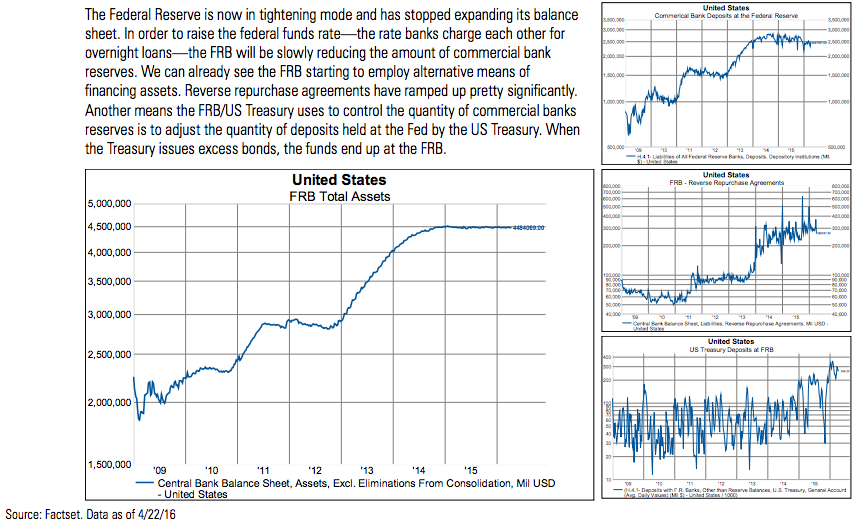

Normalization in US Monetary Policy?

Next Steps in US Monetary Policy

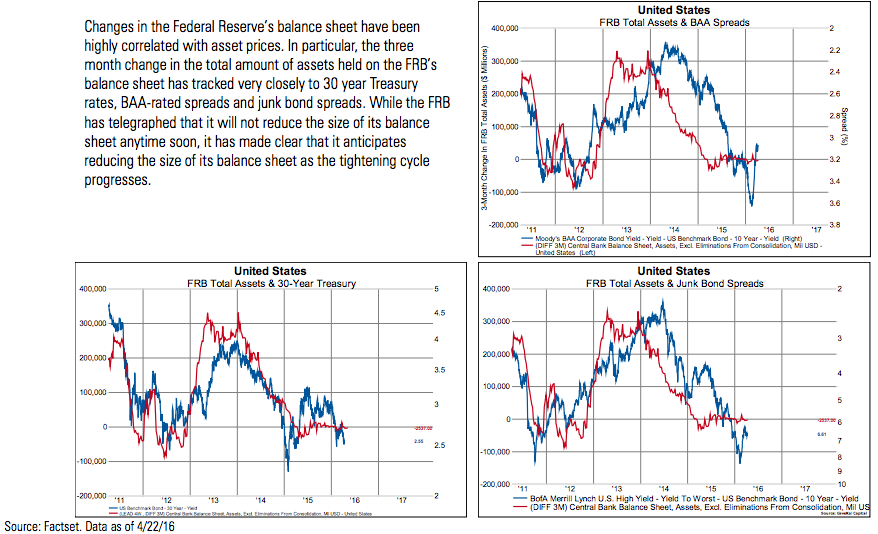

Federal Reserve’s Balance Sheet Will Contract in Time

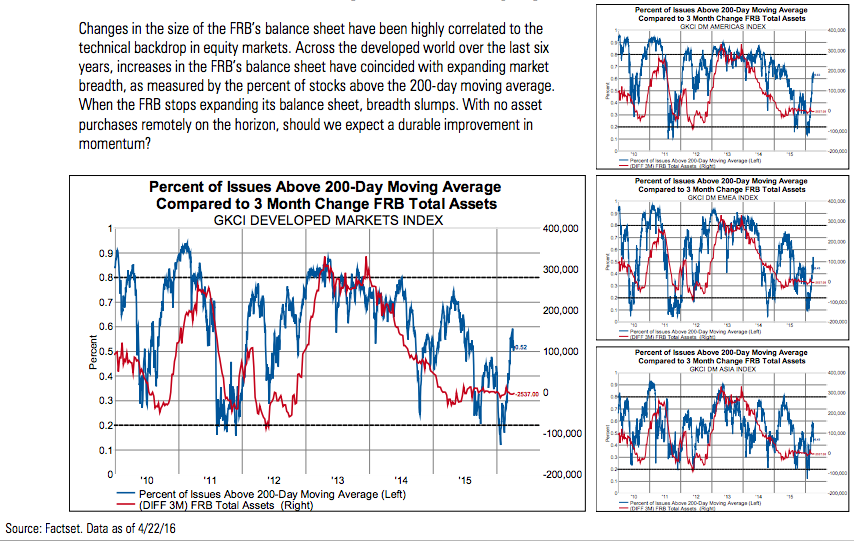

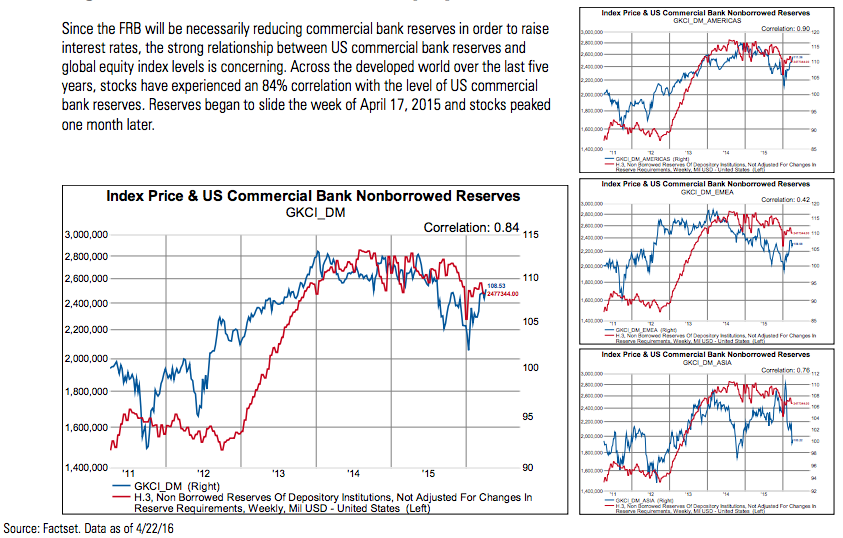

Fed’s Balance Sheet Has Been a Key Variable for Equity Markets

Shrinking Bank Reserves Pose a Risk to Equity Markets

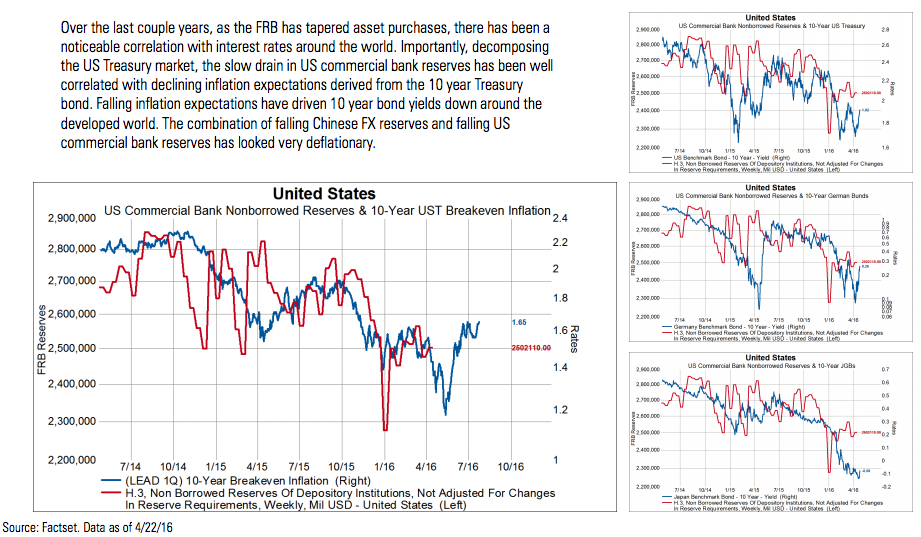

Draining Bank Reserves Has Been a Deflationary Exercise

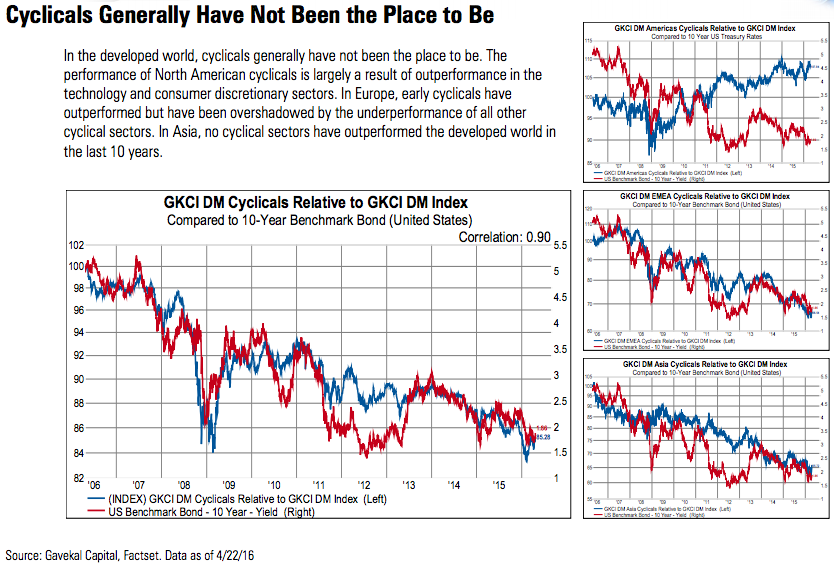

Asset Allocation in a Post Ricardian World

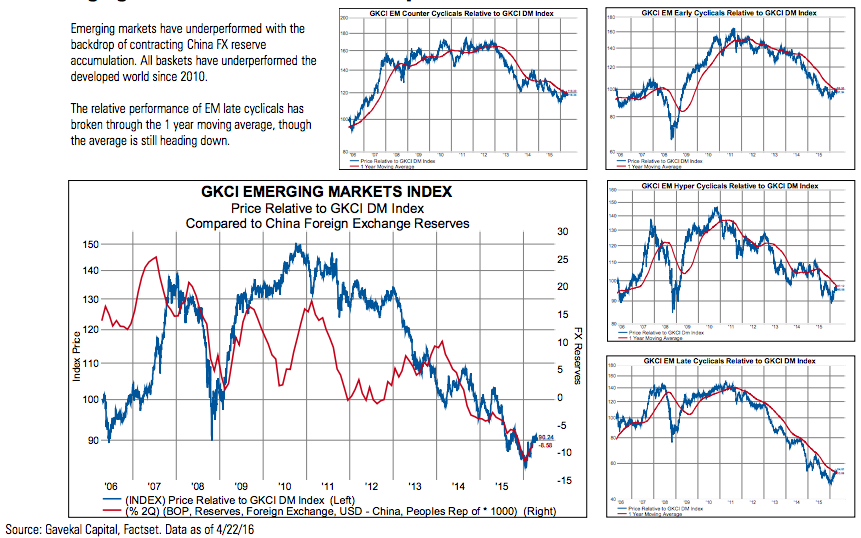

All Emerging Market Baskets Have Underperformed the Global Benchmark

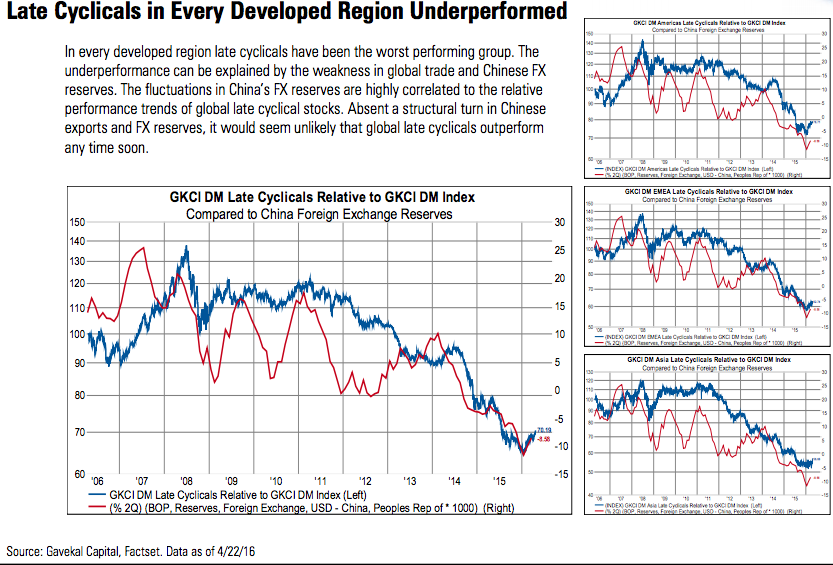

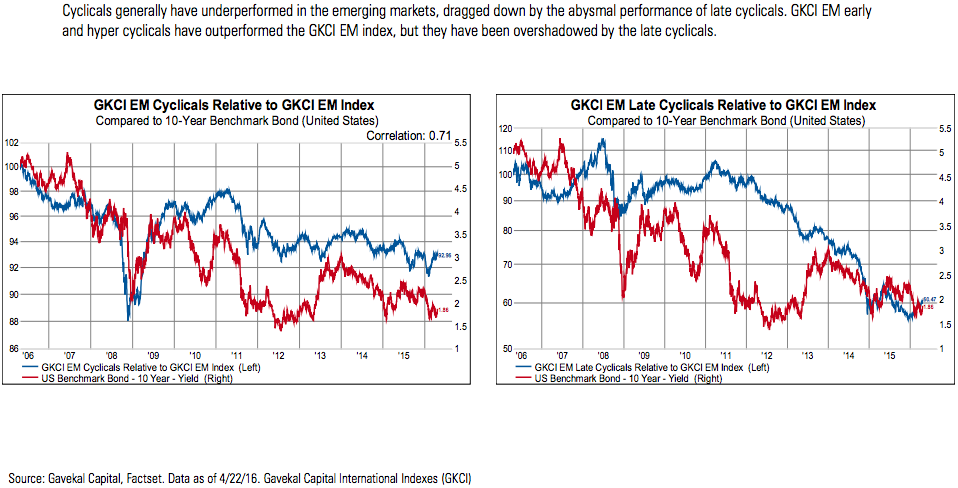

EM Late Cyclicals Have Been the Standout Underperformer

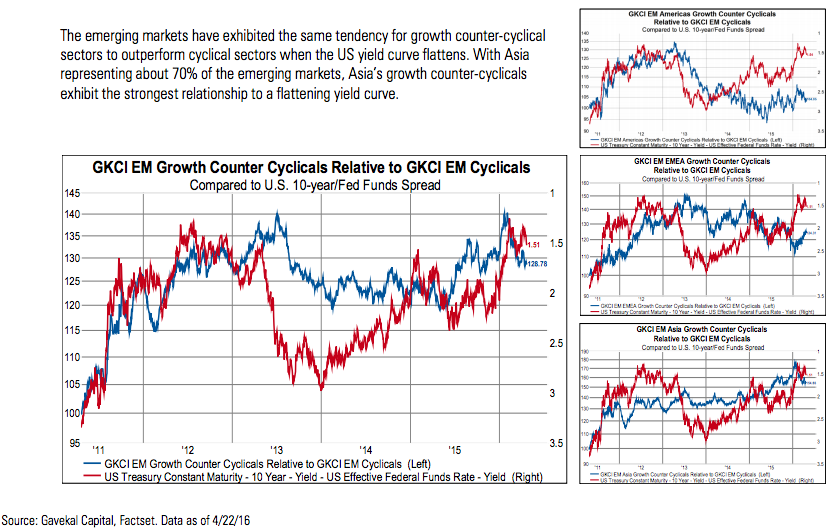

Same Strategy for the Emerging Markets

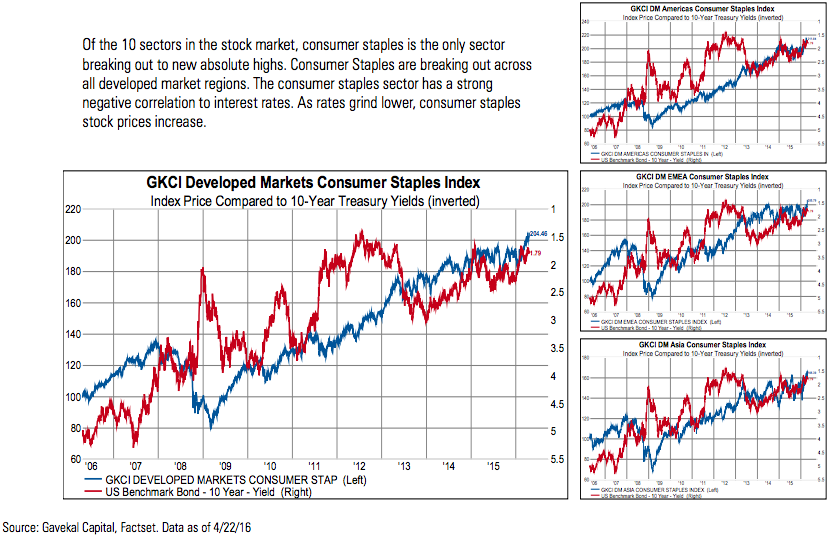

Consumer Staples is the Only Sector Breaking Out to New Highs

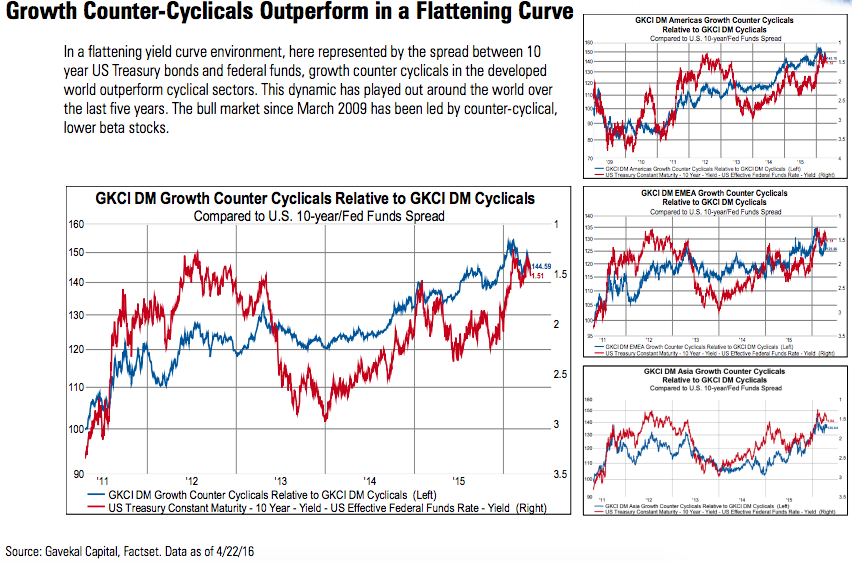

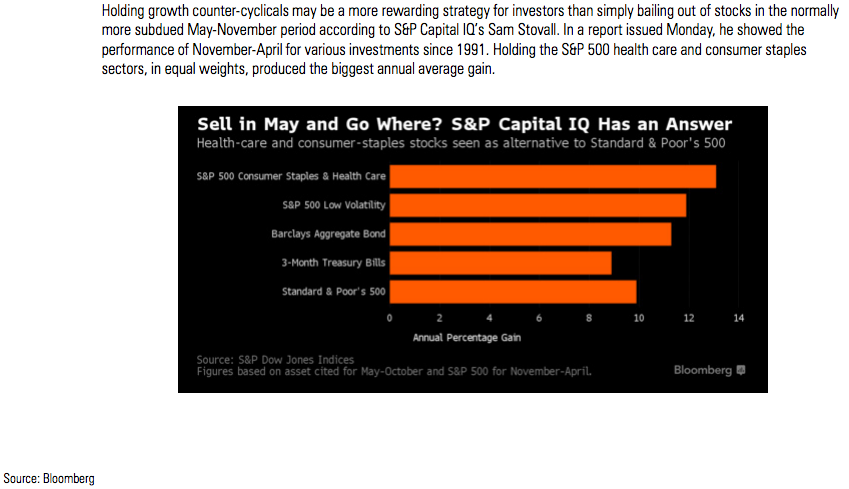

Sell in May and Go Away, or Go with Growth Counter-Cyclicals?

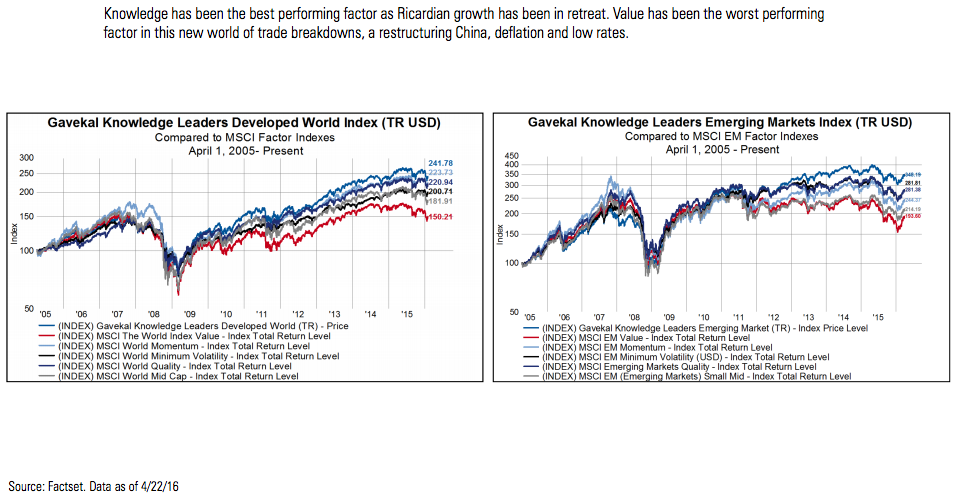

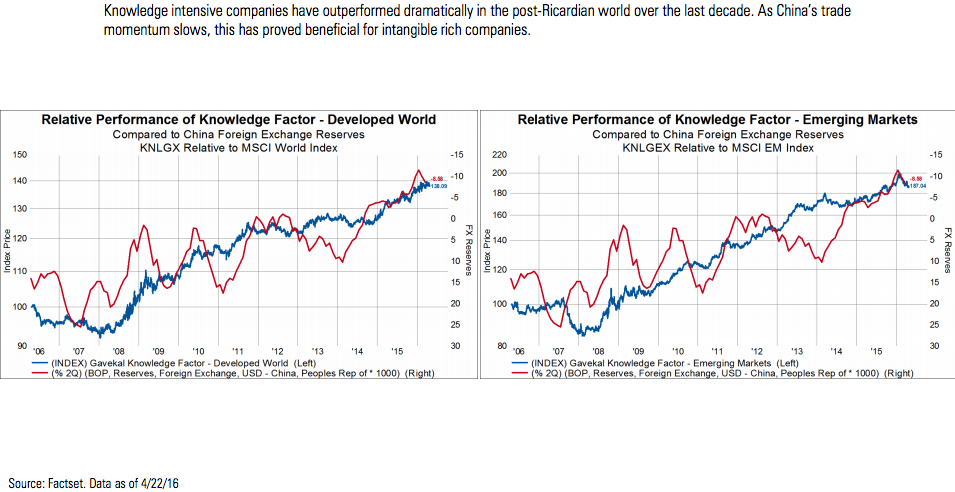

Knowledge Factor Outperforms When Ricardian Growth Ebbs

Knowledge Intensive Companies Overcome Trade Challenges

In a Deflationary World, Knowledge Intensive Companies Outperform

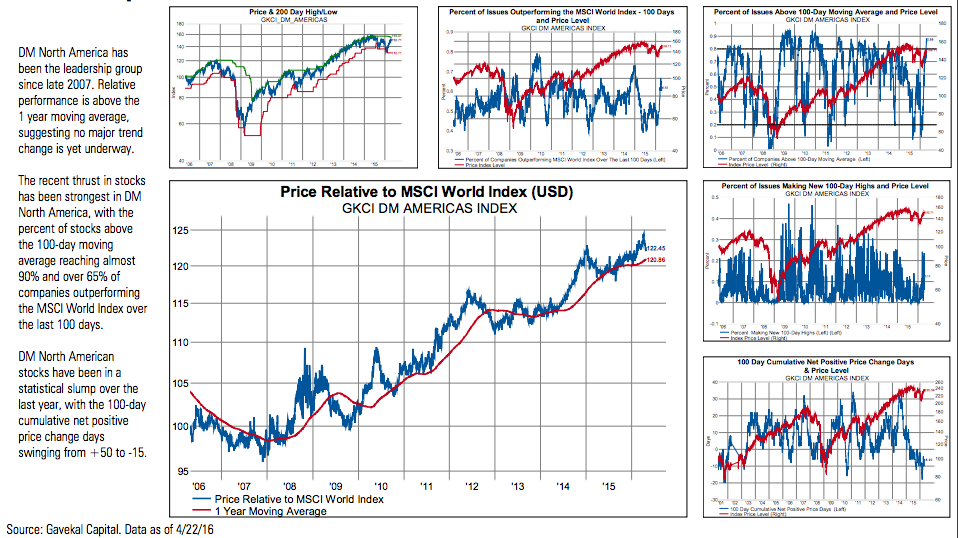

GKCI Developed World North America

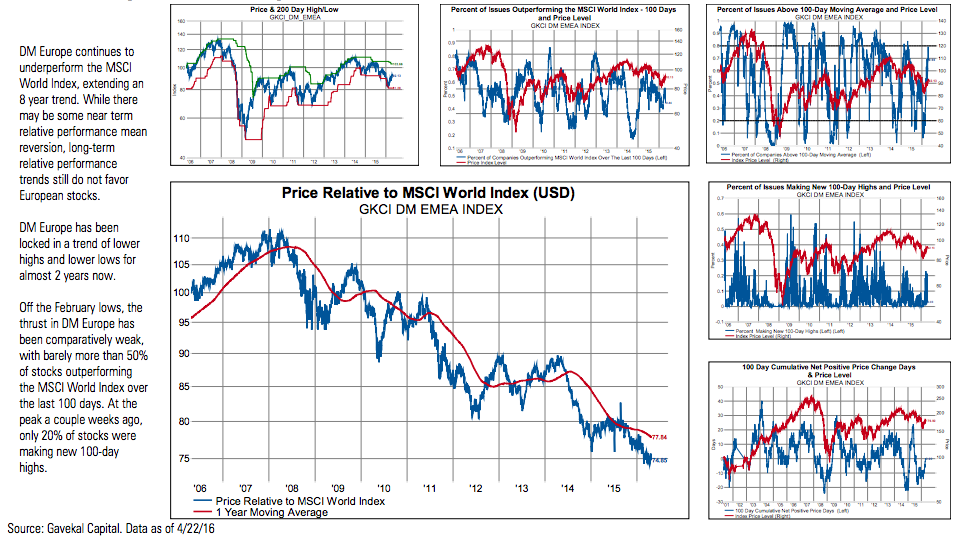

GKCI Developed World Europe/Mid-East

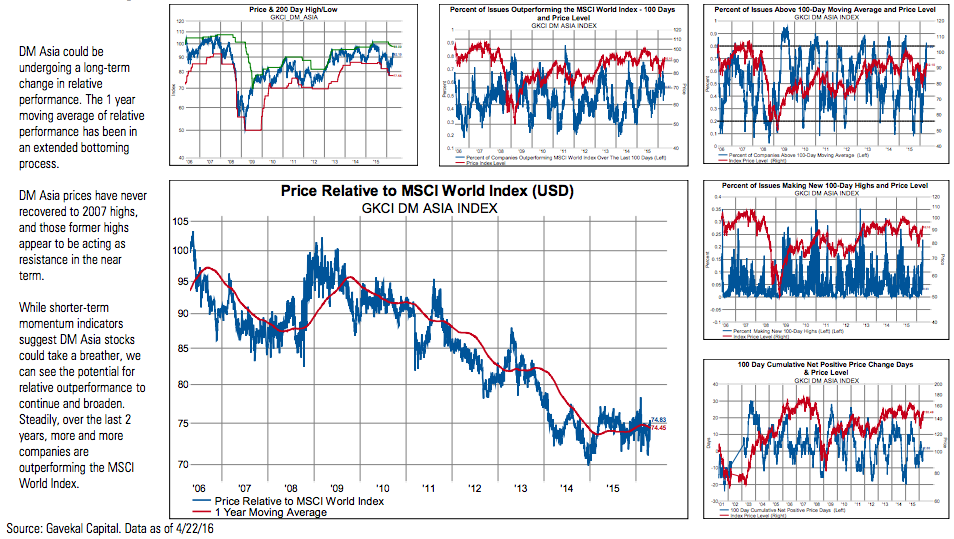

GKCI Developed World Asia

Disclosures

The Gavekal Knowledge Leaders Developed World Index is the property of Gavekal Capital, LLC, which has contracted with Solactive AG to calculate and maintain the index.

The Gavekal Capital International Indexes (GKCI) are the property Gavekal Capital, LLC. The publication of the Index by Gavekal Capital, LLC is not a recommendation for capital investment and does not contain any assurance or opinion of Gavekal Capital, LLC regarding a possible investment in a financial instrument based on this Index. For full information on the indexes, please visit the document “Terms and Conditions” available on www.gavekalcapital.com.

An investor cannot invest directly in an index.

The information contained herein is provided for informational purposes only and should not be regarded as an offer to sell or a solicitation of an offer to buy the securities or products mentioned. The strategies discussed in the presentation may not be suitable for all investors. Gavekal makes no representations that the contents are appropriate for use in all locations, or that the transactions, securities, products, instruments, or services discussed are available or appropriate for sale or use in all jurisdictions or countries, or by all investors or counterparties.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.