- Investors' appetite for risk assets has been renewed.

- The global economy remains sluggish.

- Much wariness still surrounds the possibility of a Brexit.

- Uncertainty remains about the outcome of the contentious U.S. presidential elections.

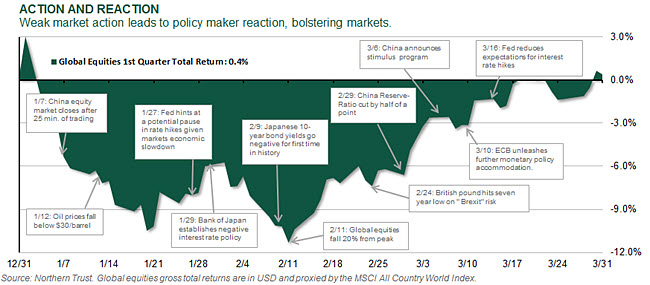

The renewed appetite for risk assets continued during the last month, maintaining the strong rally after global equities registered a 20% decline from their highs on February 11. After triggering risk aversion in January, the news out of China is beginning to show some positive effects from their multi-pronged policy approach. The markets have also been supported by more realistic utterances from the Federal Reserve. Not only has the full committee reduced their expectations closer to the market, Fed Chair Janet Yellen has gained some ground in convincing investors that she's in control of policy making at the Fed. The risk of populist politics providing a market surprise could surface first in Britain, where the June 23 vote about retaining European Union (EU) membership looks increasingly too close to call. In the United States, the party conventions will be held in the second half of July, after which we should be better able to handicap election risk.

The global economy continues to grow at a sluggish pace, with countries struggling to generate acceptable growth while still combating disinflation concerns. It appears that many analysts became too cautious over growth earlier this year, as economic reports across most regions (save Japan) have been better than expected. The U.S. industrial economy is struggling, while consumer spending is more solid. Europe's growth outlook is being overshadowed by concerns over the Brexit risk, while Japan has registered negative growth for two consecutive quarters. Chinese stimulus efforts are starting to bear fruit, as infrastructure spending is accelerating and power consumption grew at the fastest rate since June 2014.

Even though we don't see much upside risk to economic growth in the developed world during the next year, we do see some reduced downside risk in China. While inaction by politicians in developed nations has forced central bankers to carry the burden, China has been able to unleash both monetary and fiscal policy. The focus will increasingly turn to political action in the developed world over the next year as Japan struggles to accelerate growth and inflation, Europe faces stresses on its union, and the United States faces a contentious presidential election.

U.S. EQUITY

- Despite negative revisions, U.S. equities are now up year-to-date.

- Further market appreciation to be driven by earnings and dividends.

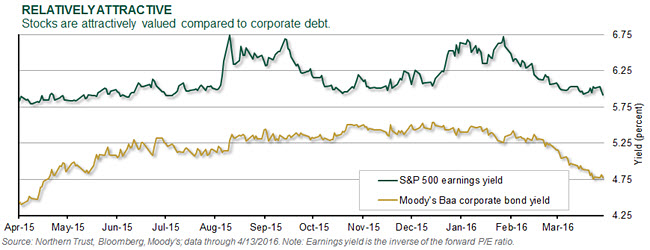

After rallying more than 13% from February lows, U.S. equities are now in positive territory year-to-date. Earnings per share (EPS) estimates for 2016 continue to slide, now representing less than 2% growth this year, leading the P/E on the S&P 500 to expand to 17.5x. This level is close to the forward P/E multiple highs seen in early 2015. While seemingly expensive, the earnings yield on the S&P 500 relative to other risk assets, such as Baa corporate bond yields, should prove supportive of the current multiple. We're more conservative than consensus in our earnings expectations for 2017 at 7% growth, so we expect out-year negative revisions to continue. Growth should accelerate as we move through 2016 and into 2017, but with little upside in valuation, we expect the majority of performance to come from earnings growth and dividends.

EUROPEAN EQUITY

- The ECB unleashes new measures to combat deflation and spur growth.

- Equity markets hold steady while the euro strengthens.

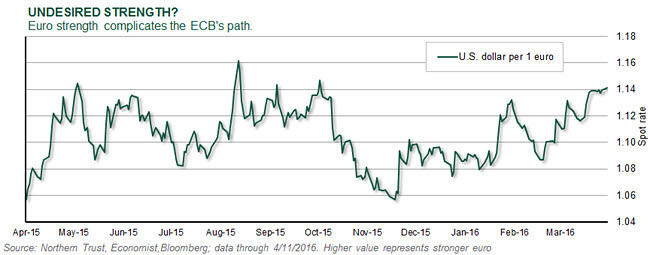

The European Central Bank (ECB) launched a new round of measures in mid-March designed to stimulate inflation and economic growth. Key components included: lowering the overnight cash deposit rates on excess bank reserves from -.3% to -.4%; increasing the ECB's monthly bond purchase program from €60 billion to €80 billion (with investment-grade corporate [non-bank] bonds now eligible for purchase); and implementing a new refinancing scheme intended to incentivize banks to increase their lending. Despite these measures, European equity markets have held flat (though this is arguably a win) and the euro, after a brief decline immediately following the ECB's announcement, strengthened when ECB President Mario Draghi dismissed the potential for further rate cuts. We expect continued consternation over the potential of Brexit to weigh on European equities until the referendum vote on June 23.

ASIA-PACIFIC EQUITY

- Continued yen strengthening is pressuring Japan's equity market.

- BOJ's late-April meeting could yield new measures.

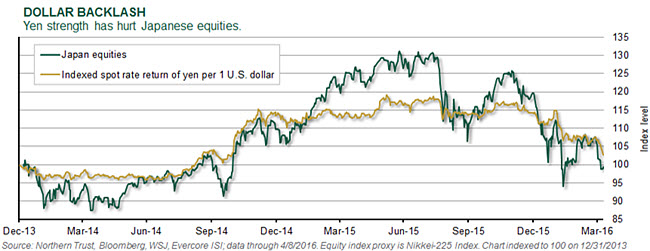

Despite a potpourri of ideal ingredients for currency depreciation (such as negative interest rates), a surprise strengthening of the yen has occurred. This can be attributed to a dovish Fed, tame inflation expectations within Japan, an ECB that also implemented negative rates and continued global macro uncertainty (with the yen still perceived as a safe haven). The yen has gained 14% since last summer's lows and is now at levels last seen prior to the Bank of Japan's (BOJ's) massive quantitative easing expansion in late 2014. Although negative rates have spurred bank lending and housing starts, yen strength ultimately undermines Japan's export-driven economy — which in turn could pressure consumer confidence/spending. In the face of this yen strength, the Nikkei has declined 5.5% since the end of March and 16% year-to-date.

EMERGING-MARKET EQUITY

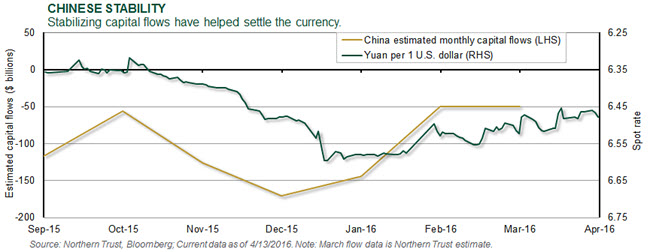

- Near-term risks around China have receded.

- Longer-term economic challenges remain.

Concerns over the state of China's economic and financial affairs were a significant contributor to market weakness earlier this year. Policymakers have responded with easier monetary policy and infrastructure spending, which is starting to show up in the economic data. They have also succeeded, so far, in significantly slowing the outbound flow of capital, resulting in relative stability for the renminbi. As we believe these developments have reduced the downside risk around emerging-market assets, we moved our recommended tactical asset allocation from underweight to market weight. Longer term, China still faces challenges around credit quality and the need to develop a stronger service and value-added manufacturing economy. During the next year, however, we expect reduced downside risks along with a more stable U.S. dollar to lead to improved performance of emerging-market equities.

REAL ASSETS

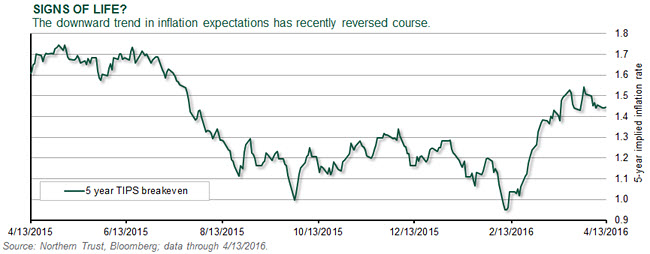

- Market indicators on expected inflation have caught investors' attention.

- The recent uptick in inflation expectations isn't expected to persist.

With oil prices finding a near-term bottom and anecdotal signs of gathering wage pressures, some investors are beginning to think the last five years of disinflationary trends is drawing toward a close. These fundamental factors, combined with renewed dovishness on behalf of central banks, have pushed inflation expectations up meaningfully (see accompanying chart). But upticks in inflation expectations of similar magnitude to that just witnessed have occurred five times over the past five years. Each time this has occurred, inflation expectations have subsequently rolled over. Given expectations for continued slow economic growth and rising job market participation rates, we believe inflation will still take time to ignite. Turning to asset allocation, our inflation outlook doesn't endorse a tactical emphasis on inflation-sensitive asset classes at this time.

U.S. HIGH YIELD

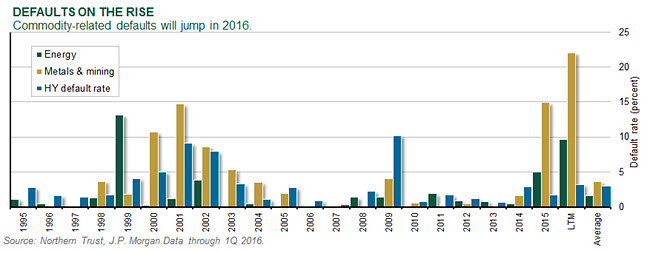

- The high yield default rate is expected to increase in 2016.

- Easily identified sectors will drive the increased high yield default rate.

The high yield default rate is expected to increase in 2016 after several years at a low rate. Although an increase in defaults isn't positive, the increase will be driven by the obvious commodity sectors. Moody's estimates a 4.7% default rate in 12 months, a 1% jump from the current 3.7% default rate. For context, the long-term default rate for high yield is 4.5%. The accompanying chart shows the default rate of the energy and metals and mining sectors alongside the overall default rate. The dramatic increase in defaults in these commodity sectors is driving the increase in the overall rate, but fundamentals in the broader high yield market are far more stable. Managing exposure to the commodity sectors can avoid default losses and improve portfolio outcomes.

U.S. FIXED INCOME

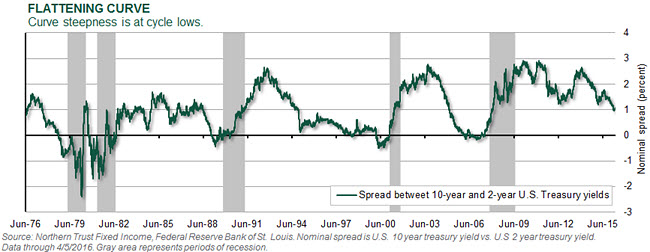

- The U.S. Treasury 2- and 10-year spread is at its lowest since 2008.

- We believe U.S. Treasury spreads reflect expectations of slow growth and low inflation continuing.

Investors look to the spread between U.S. Treasury notes with maturities of two and 10 years as one market-based indicator of future growth and inflation. In the past, when this indicator has flashed negative — that is, when the yield on the two-year note is larger than that on the 10-year note — it's been a predictor of a future recession, albeit with approximately a one-year lead time. Even though the spread currently remains positive, it's at its narrowest since the last U.S. recession in 2008-2009 and bears watching. We continue to believe that the U.S. economy will experience modest growth and low inflation, continuing the trend seen throughout this economic expansion. We expect rates to stay range bound in this environment during the next year.

EUROPEAN FIXED INCOME

- Risks of "Brexit" are increasing.

- The markets appear to be testing the resolve of the ECB.

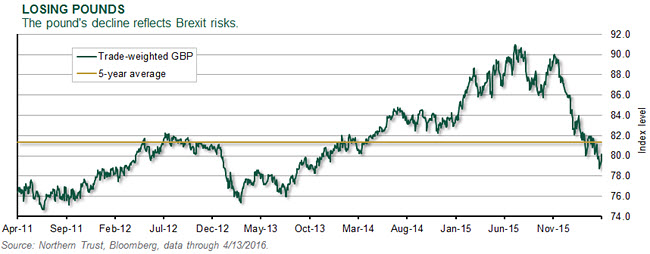

The markets have pushed U.K. interest rate hike expectations into 2018, and the pound is at a multi-year low, all of which may be attributable to the upcoming U.K. referendum on EU membership. Early opinion polls appear divided, but markets possibly reflect a greater risk of a "leave" vote, paying little attention to the reasonable economic backdrop. The effects of the referendum vote could be more apparent in second-quarter data as activity inertia kicks in, but markets could sharply reverse course if the United Kingdom votes to stay. Despite the unleashing of a range of measures from the ECB, euro-area sovereign spreads versus German bunds have moved wider since. Investors will become increasingly concerned about this, while the ECB appears reticent to enact further interest rate cuts.

ASIA-PACIFIC FIXED INCOME

- Yen appreciation puts the BOJ under pressure.

- The Reserve Bank of India cuts interest rates in response to lower growth and inflation.

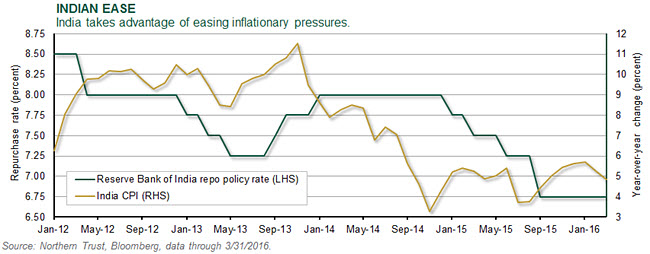

Since the introduction of negative interest rates in January, the yen has appreciated almost 10% against the dollar. This is no doubt worrying for the BOJ, as an exchange rate of 103 is being touted as a key breakeven level for domestic exporters. The BOJ has willingly intervened in the past and has indicated a willingness to do whatever is necessary, but markets are beginning to put fiscal policy back under the spotlight as monetary policy efficacy comes into question. The Reserve Bank of India announced a 25 basis point cut at its April meeting taking the repurchase rate to 6.5%. While lower oil prices should be positive as a net importer, government oil subsidies appear to be masking these benefits, placing increased responsibility firmly on the central bank.

CONCLUSION

The most important conclusions from this month's asset allocation discussions surrounded reduced downside risk from China and increased confidence that the Federal Reserve better understands the challenges it faces in normalizing interest rates. As Chinese policy moves look to be stabilizing its growth outlook, and capital flows out of the country have slowed, the risks of a material disappointment over the next year have been reduced. As such, we recommended an increased 3% investment in emerging-market equities — raising our previous underweight position to a neutral stance. We funded this increase through a decrease in U.S. equities — where our substantial overweight position is being trimmed. U.S. shares have materially outperformed during the last several years and are trading at higher valuations than its peers — supporting a moderate reduction in the overweight.

During the last two months, we have removed U.S. dollar strength and a Chinese hard landing from our risk case scenarios. We're currently focused on the potential of a negative surprise coming from the British EU referendum, the U.S. presidential election or from major central bankers. The outlook for the June 23 British referendum has narrowed, but the recent support for the "stay" vote from the Labour Party unites the two major parties. Late July will likely provide clarity around the U.S. presidential election, where the uncertainty is greatest on the Republican side. If Donald Trump is unable to secure a majority of delegates heading into the convention, a candidate other than him could become the nominee. The party is likely focusing beyond the presidential race toward retaining control of Congress.

Our concern about negative developments on the monetary policy front diminished some over the last month, as Fed Chair Yellen articulated a strong and dovish outlook. The Fed had previously communicated an expectation of four rate hikes during 2016, which the market was never close to believing. The Fed's new expectation of just two hikes is still higher than the market, but the discrepancy is more manageable. Fed Fund futures are pricing only a 50% probability of a single hike this year, and those probabilities will need to rise for the Fed to smoothly raise rates. Improving economic growth, along with steady risk markets, are likely required for this scenario to play out. This positive set of developments, along with clarity on the political front, could set the stage for better equity markets later this year.

© Northern Trust