First Quarter 2016 Economic & Capital Market Summary

If you are following the presidential election process, you might conclude that the U.S. economy is in crisis and that we are nearing the brink of catastrophe. On both sides of the isle, Democratic and Republic candidates have built messages to the voters that the economy is in decline and that they have solutions to fix it. Yet, the Federal Reserve, which is our loudest voice right now on the outlook for the health of the economy is saying that everything is okay. What should we believe?

Well, for starters – nothing has really changed. We are in the same spot we have been in for the past three years. Domestic economic growth is bumping along around 1.5% and we are seeing evidence of a sharp slowdown in the first quarter of 2016. At the same time, we estimate that the rate of inflation is running near 1.5% with the potential to increase through the year as oil prices begin to rise. This mediocre economic activity is supported by an increase in nonfinancial debt and aggressive monetary policies of the Federal Reserve. These aggressive monetary policies have the effect of inflating asset prices which has, in turn, distorted the price of risk of publicly traded securities in the capital market. We believe that the effectiveness of these aggressive monetary policies is nearing an end and our economy is exposed to the downside in the absence of structural reforms. These structural problems include distortions in the labor market, the lack of business formation which is suppressing job creation and dismal private credit expansion.

During the Financial Crisis, the U.S. government accumulated significant amounts of debt in order to pay its bills including its commitments to pay social security as well as to support entitlement programs such as Medicare and Medicaid. In addition, levels of debt increased in other areas of the economy including public and private pension plans, student loans, and auto loans. This phenomenon was repeated in other developed countries including Japan, Great Britain and much of Europe which has led to huge growth in global debt. The growth in global debt which has been used to support consumption and easy monetary policies ultimately suppresses economic growth in the long run.

A real improvement in domestic economic growth rests on two key issues: job growth and private credit expansion. The economy is producing on average over 200,000 jobs per month and we have experienced six consecutive years of job creation. This would normally lead to an increase in pressure on wages which, in turn, would lead to an increase in consumption. Yet, wage growth is stuck near 2.3%. American businesses would rather buyback stock or increase dividends to shareholders, than increase employment headcount.

The slowdown in global growth is a concern for investors as well as the Federal Reserve. As the Fed postures to increase U.S. interest rates, the central banks of other developed countries including Sweden, Germany, Denmark, Switzerland, Japan and the European Central Bank are pushing interest rates into negative territory. We view the push into negative interest rates by developed countries as deflationary and a dangerous policy tool. We believe that negative interest rate policies will not work in the long run and will penalize savers and hurt the banking and insurance sectors. We also believe that it is a policy tool that our Federal Reserve is prepared to use if necessary.

Negative interest rates are forcing the cost of equity capital higher in Europe and ultimately hurting equity returns. Yet, there are two other issues which concern us with respect to Europe: the inability for Greece to be an economic contributor to the European Union and the vote in June for Great Britain to leave the European Union. In our view, there is a possibility that both countries leave the EU which will likely cause a spike in volatility as capital flows and counterparty requirements become more uncertain.

Financial assets have weathered the collapse in oil prices; however, the ride was treacherous. Many investors limited to publicly traded stocks and bonds were left licking their wounds at the end of the first quarter. We are beginning to see signs of a deterioration in the credit cycle which may foreshadow the next wave of market volatility.

The Economy

We believe that the fuel for the economic recovery is the capital that is provided to support business investment. Supported by low interest rates and easy monetary policies, without a doubt, there is adequate fuel for the recovery to continue. One only needs to look at the $2.5 trillion of excess reserves on the Federal Reserve’s balance sheet to realize that if the banks want to lend, there is sufficient dry powder to do it.

Yet, if there is adequate fuel to stoke the economic engine, the question then becomes: is the engine working efficiently? Our answer is that if this is an eight cylinder engine powering a speed boat across the water, we are only running on five cylinders. That’s enough to get down the road, but not enough to meet the potential speed for which the engine was built. But, the hull of the boat has holes in it which are slowing us down as well. Examples of these holes in the boat include: the $1.2 trillion student loan problem, the imbalances in the current tax code, the growing income disparity, and the lack of lending to small businesses. As a result, we can keep pouring more and more gasoline into the engine, but, at the end of the day it isn’t going to help us move across the water any faster.

According to the Bureau of Economic Analysis, the US economy grew at a rate of 1.4% in the fourth quarter of 2015. We expect growth to inch in around 0.5% in the first quarter of 2016. We are seven years into a recovery, which is now the fourth longest on record. The domestic economy is over $19 trillion and roughly 70% is represented by the consumer sector. In our view, consumers remain cautious which is underscored by the recent -0.1% decline in consumer spending posted for February and downward revision to -0.4% for January. While these figures may be skewed by the decline in gasoline prices and auto sales, they cast a shadow on the consumer heading into the second quarter.

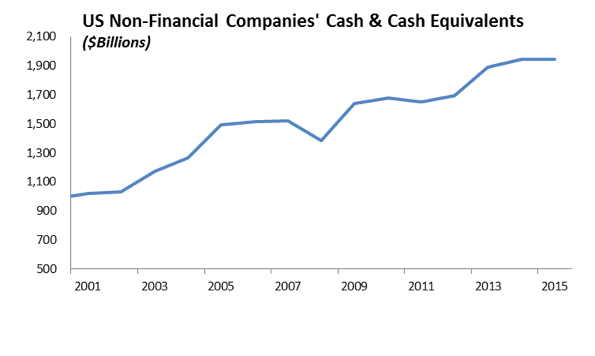

Within the domestic economy, the corporate sector is not meeting its potential. The ISM survey increased to 54.5 in February in a sign of health; however, the strong dollar is making domestic exports more expensive putting additional pressure on manufacturers. American corporations are throwing off huge profits and cash flows, yet capital investment is relatively low. Since the financial crisis, corporate management has preferred financial engineering, including hoarding cash and buying back shares, rather than investing capital in their business. Ultimately, the increase in corporate debt to support stock repurchases does not support economic growth, increased employment, higher wages or improved productivity. Over the long term, this form of increased debt will have a weakening effect on the economy.

Finally, global weakness in demand has acted like a brake on the U.S. economy. The result is the trade deficit continues to be a drag on the domestic economy. According to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau, the U.S. trade deficit increased 2.6% in February to $47 billion, its highest level since August 2015. With the sharp decline in oil prices, petroleum imports in February hit their lowest level since 2002. The average price of imported crude oil was $27.48 a barrel in February, the lowest since December 2003.

Monetary Policy + Fiscal Policy

Central banks exist to assist economies with the flow of money which in turn supports economic activity. This is important because if the flow of money is too great or distorted, it causes imbalances in the economy which could ultimately lead to recessions, financial crisis, or high rates of inflation. Interesting, at least to us, is that monetary policies that worked 15 years ago don’t work today. Monetary regimes change over time and generally last for periods of around 30 years. We have moved from a monetary regime that was focused on a target level of interest rates, the Fed Funds Rate, to a monetary regime focused on quantitative easing and asset purchases to manipulate the level of interest rates. The Federal Reserve will use its $4.5 trillion balance sheet to affect monetary policy and continue to grow it if necessary. This is our new monetary regime and we expect we are here for a while.

The Federal Reserve spent most of last year “talking up” an increase in short term interest rates which they pulled off in December. Immediately following the 25 basis point increase in short term interest rates, China’s capital markets imploded, the price of oil collapsed and the IMF began pressuring the Fed to back off its march toward high interest rates for fear that it would counter act the simulative policies of other developed countries. So far the Federal Reserve has not signaled a move higher and we do not expect that they will make a move toward higher until later this year, if at all.

What Does the Election Mean to my Investment Strategy?

If you are a U.S. citizen, you are guaranteed certain liberties and freedoms as part of our democratic society. One of those liberties is the right to vote. Yet, how do we vote for candidates that don’t represent the best interests of the American people or our form of capitalism? And, if you voted republican in the primary, does your vote even matter if the GOP convention is contested? With social media, huge sums of money backing candidates, and little accountability on what the candidates represent in speeches and debates, our presidential election process has become theater for global entertainment. It appears that candidates will say anything to get elected by misrepresenting the facts, contradicting themselves or even outright lying (check out www.factcheck.org ). Ultimately, the American voter is being forced to vote for candidates that are controversial within each of their own parties. As entertaining as our election process is, the entire primary process is failing American voters.

We believe that we are in a season of change for our democracy. It is not a failure of our form of government; but, rather a recognition that our democracy is evolving. And, it needs to evolve to meet the needs of its people. Even our position as a global leader is evolving. Our foreign policy, which was largely formed in the 1950’s after World War II, appears out of date and ill-suited against terrorist threats such as ISIS. In addition, we have ballooned our debt level to maintain spending on entitlement programs and not a single presidential candidate has offered up a solution to this problem.

Historically, presidential elections have had little impact on the capital markets. We would not advocate making dramatic changes to investment or spending strategies based on the election. However, if either Trump or Sanders is elected president, we would expect volatility will increase and equity valuations to decline initially based on their current views.

Investment Strategy

The S&P 500 returned 1.35% and the Barclays U.S. Aggregate bond index was up 3.03% in the 1st quarter. However, for both fixed income and equity investors, the first quarter returns do not tell the story of the journey through the markets. As volatility spiked toward the end of 2015, equity prices plummeted right at the start of the new year. Confusion in China’s central bank policies as China growth slowed, a near free fall in oil prices, and increased volatility in global capital markets provided a toxic combination of events which pushed equity prices down and interest rates lower. Compounding the market turbulence was Federal Reserve rhetoric that seemed to hold to further tightening through 2016. The result was the S&P 500 declined sharply by 10% on February 11, prices in high yield declined and credit spreads gapped wider as bonds in the energy and minerals and mining sectors declined sharply by mid-February. Yet, by the end of the quarter, prices in both equities and fixed income had rebounded. The sharp rally in domestic stocks underscores our belief that the current use of derivatives and general illiquidity within the overall capital markets make for treacherous investing.

The sheer amount of money supporting the equity markets through ETFs, Index Funds, retirement plans, and pension funds, equity valuations will remain elevated. As a result, expected returns from current levels will be limited and below historic averages.

At its peak, the S&P 500 lost over -13% and crude oil fell to a low of 26.05 in the first half of the quarter. Through the quarter, markets were highly correlated to price swings in oil with fears around bankruptcies in the energy sector. The worst performing sectors in the S&P 500 were financials and healthcare, which had over 5% declines for the quarter. Utilities and telecommunications were the best performing sectors, as investors flocked to high dividend “safety” stocks during a period of heightened volatility. The MSCI EAFE fell over 15% at its lows, ending the quarter with a -3.01% return.

We are sanguine on stocks in the banking sector given the low level of interest rates and decline in net interest margins. We are still in the camp that the large banks will ultimately voluntarily reduce their businesses given the higher required capital levels. Also, we expect the regulatory costs facing the industry will continue through 2016.

At our core, we believe that security valuation does matter. With respect to domestic equities, we are buyers on weakness and more risk averse at elevated market valuations given the inefficiencies in the current market structure. Volatility will be range bound and we expect there will periods where volatility will spike. In the past, these periods have proven to be very short.

Ultimately, we see domestics stocks as range bound with fair value near 2050 for the S&P 500. However, markets often move is strange and irrational ways. With the strong recovery in domestic stock prices, we are inclined to take profits. Corporate earnings will be challenged again this quarter and we expect earnings on the S&P 500 to decline by over -7.1%. With operating margins near peak levels, and lack of top line growth, equity markets have very little catalysts for growth. We are currently overweight domestic large cap equities relative to small cap stocks. We see the lack of credit expansion to small and mid-sized businesses as an ongoing restriction to both revenue and earnings growth.

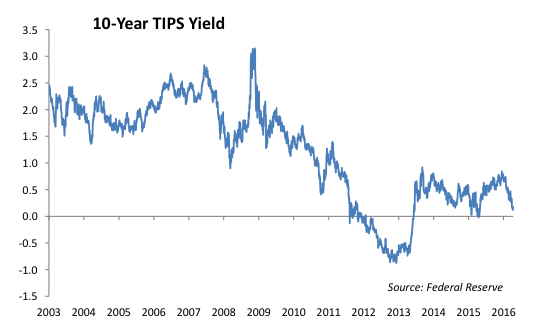

Given the low levels of domestic economic activity and inflation, we expect interest rates will remain low. The yield on the 10 year Treasury Inflation Protection security has moved near 0% as inflation expectations have declined with the fallout in commodities prices.

The Federal Reserve will continue to talk out of both sides of their mouth in an effort to manage the capital markets expectations for the next incremental move higher. But, we don’t expect any moves from the Fed until later this year. Corporate spreads should tightened in both investment grade and high yield sectors as the fixed income markets digest the massive balance sheet restructurings facing the energy sector.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2016 Winthrop Capital Management