If you sell when the market no longer represents “value”, when do you buy back?

One of my favorite quotable investors, Howard Marks, recently reminded us of the challenge in dealing with “two-decision stocks”: You sell because you think the price may fall (even though it may be something you’d like to hold for the long term), and then you have to figure out when to buy it back. He even recalled Charlie Munger complaining that “they’re really “three-decision stocks”: you sell it because you think the price is full, you have to figure out when to buy it back, and in the meantime you have to come up with something else to do with your money”.1

Is long-term value investing an oxymoron?

Given the difficulty and cost of buying and selling “the market”, I understand the temptation to take the long view and just “buy and hold” well-chosen securities. But, as a convinced value investor, I have long had the uncomfortable suspicion that there might exist an inherent contradiction between my (ideally) preferred long-term investment horizon and the value investing discipline in which I believe.

Regrettably, the “buy and hold” approach is no panacea. In the 1980s, having stumbled upon one of my papers, the “pope” of growth investing, Philip Fischer4, invited me to visit with him a company based in California. We spent the whole day there and met with executives and employees at many levels of the company, following the research approach Fischer advocated: Do extensive research, buy the best-managed company in a chosen field; and, pretty much whatever the purchase price, let future earnings carry the stock higher over the long term, since "the best time to sell a stock is almost never" (a phrase I believe Fischer invented).

There are two problems with this approach.

The first one, although anecdotic in the bigger perspective and probably an exception in Fischer’s highly successful record, is that the earnings of the company we visited that day never carried its stock much higher.

The other one is that Phil Fischer’s extensive kind of research unfortunately has become much more difficult to implement in today’s regulatory and compliance-driven environment. It relied on the fact that, by doing more extensive research, i.e. asking more and better questions, one could gain a legitimate advantage over other investors – especially in evaluating the quality and depth of a company’s management. But today’s regulations assume otherwise: that, if through your hard work you discover more information about a company than is broadly known, you must have benefited from illegal “inside” information.

As a result, companies broadcast earnings “guidance” for the next quarter or year, but otherwise limit the personnel authorized to speak to shareholders and analysts, and follow a closely written, attorney-controlled script in communicating with investors. The chances of gaining an advantage through extensive research, have been drastically reduced.

Unfortunately, value investing also has its problems.

A value investor recognizes that, over short and intermediate periods, crowd psychology drives stock prices somewhat independently of fundamental considerations. As a result, measures such as price-to-earnings ratios alert value investors to major buy and sell opportunities throughout stock market cycles. Value practitioners are supposed to buy a stock when its price falls below its intrinsic worth as a business but, logically, also to sell it when its price rises well above that intrinsic worth, since it then no longer represents “value”.

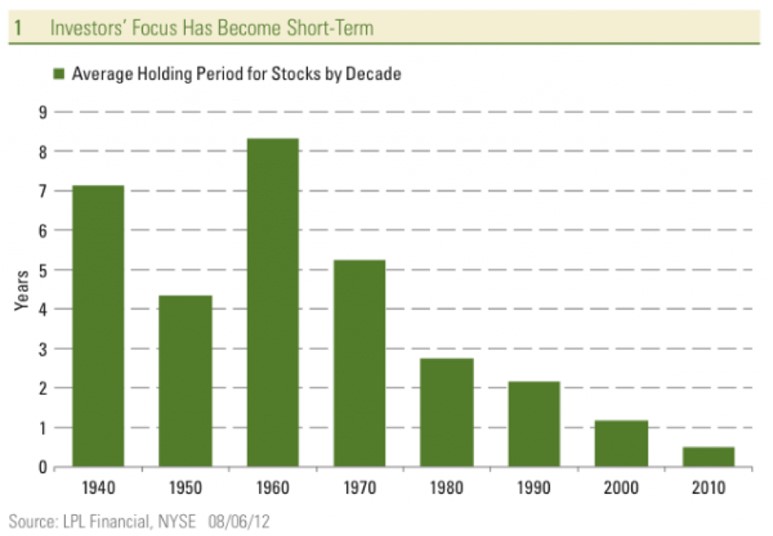

Buying and selling, however, have a cost. I do not refer only to brokerage commissions, which have shrunk to the point of becoming secondary in recent years. But, especially for large accounts, market realities mean that a buyer usually pays a bit more and a seller usually sells for a bit less than either expected. The more trading, the higher those “friction” costs. This penalty has grown in recent years as the pressure on institutions to compete over ever-shorter periods has intensified, causing them to buy and sell more frequently.

As holding periods declined in general, the short-term volatility of stocks increased, inciting even value investors to realize gains and losses more often than in the past – though obviously not nearly as often as today’s high-frequency traders. In the process, the difference between investing (long-term) and trading (short-term) has become somewhat blurry.

In a bull market, cash is not popular

Personally, I never believed that investing was about squeezing every last tiny fraction of return from my investments, so I never lost much sleep over what to do with the proceeds from stock sales. If one is into the relative performance game, which is akin to a sprint competition, this may be justified. But when the goal is to achieve large patrimonial gains over a lifetime, I believe that one’s energies are better spent on other choices, and holding cash is fine while you look for the next investment opportunities.

What, until then, had been only a logical intuition about the proper role of cash in investment portfolios was dramatically put into focus for me during the stock market crash of October 19, 1987.2

The Tocqueville Fund had been launched a few months earlier, in January 1987, by which time I already had become leery of what I viewed as a growing overvaluation of the U.S. stock market. With few compelling investable ideas, I kept in cash much of the money that had been trickling in from subscriptions. I felt particularly free to do so since, with no advertising, most of the initial investors were brokers of my firm, Tucker Anthony, and our traders, who were all familiar with my then cautious investment views.

Yet, as the market kept rising, these colleagues started calling to point out that their investments in the fund were only a portion of their total assets and that I should not treat the fund as I did my own portfolio or those of the families whose total patrimonies I was managing. I clearly remember one comment: “If we wanted to own a money-market fund, we would have bought one!”

I tried to argue, of course. In an early September 1987 report, I drew a parallel between the stock market situation then and that in the early 1960s.

The general idea was that the market indices were now showing signs of overvaluation (such as a 21-22 price/earnings ratio for the S&P 500). But the same had been true at the end of 1961, and the market had continued to advance for seven more years, through 1968, boosted by unusually strong growth of corporate profits. Price/earnings ratios had declined almost steadily from 1961 to 1968, but the shares of companies with strong earnings momentum had advanced anywhere from 50% to 80%.

I expected a similar pattern to characterize the coming few years, but with an important caveat: Twice, in the 1960s, the market had suffered sharp corrections, of 25% each in 1962 and 1966. Neither of these corrections, however, had been associated with an economic recession: rather, both had been short-lived, and had resulted from a temporary contraction of monetary liquidity in the preceding months. Still, those experiences justified holding some prudential cash reserves.

Indeed, the same could well happen now, I argued, especially in the shares of large, well-known companies, which had paradoxically become the most volatile (and thus vulnerable) sector of the stock market because of their growing exposure to the short-term whims of foreign investors and program traders. On the other hand, the shares of quality medium-sized companies should better resist a liquidity-driven market correction, because they were generally not owned by such investors and traders.

In the end, despite my early arguments in favor of cash, I yielded to public opinion and invested a much larger portion of the Tocqueville Fund portfolio into stocks. I rationalized that, since we would be largely invested in shares of medium-sized industrial companies which, after a number of lean years, were now experiencing accelerating earnings and offered excellent 3-4 year recovery and growth prospects, we should not worry about any market correction and concentrate instead on company fundamentals.

King for a day

I now quote excerpts from my November 13, 1987 report, only two months later:2

* Our benchmark accounts had done quite well since the beginning of the year, thanks to the growing realization on Wall Street that American industry, not only was not dead but, indeed, was in the midst of a major revival. For the first nine months of 1987, these accounts achieved a total return of close to 37%. The Tocqueville Fund, which did not yet exist at the beginning of the year, also outperformed the leading stock market indices from the end of March to the end of September (+14.7% vs. +12.0% for the S&P 500).

* From the end of September through the "Great Crash" on October 19, our stocks held up remarkably well. At the close, on that day, a share of The Tocqueville Fund was 22% below its September 30 level, while the Standard & Poor’s 500 had lost 30% over the same time span. I took this relative performance as a clear vindication of our views: we had done better than most on the way up, and had also held up better on the way down. With our portfolios still comfortably ahead for the year, I felt quite proud of myself and my team.

Then, the sky fell down... In the seven days that followed, while the S&P 500 actually recovered a few percentage points, the Fund's Net Asset Value per share dropped 17%!...

Looking back

The sharp drop of our investments in the week that followed the big crash can best be explained by a breakdown of normal market operations, following this historic collapse. The size of the decline on Monday October 19, and the unprecedented volume on which it took place shook up the confidence of even the coolest, longest-term investors. Some may have had to face margin calls, but a majority simply must have felt it prudent to raise some cash in their portfolios, especially in view of the widespread references to the Great Depression, both before and after the crash. If they looked in their portfolios for investments to sell which had not declined very much, they would naturally have turned to stocks such as the ones we held…

… As a result of all this, many of the stocks in our portfolios suffered sharp declines in the following few days, on practically no volume, which would seem to indicate that, while there unfortunately were no buyers around, there actually were very few sellers.

Note: I am using a combination of benchmark portfolios and the Tocqueville fund to describe what has happened to our investments in the last few weeks, because the Tocqueville Fund did not yet exist at the beginning of 1987, and we only calculate the performance of our benchmark portfolios quarterly. Since both contain very similar investments, however, it is reasonable to assume that they would have moved in parallel during the periods considered. Also, the performance figures quoted for the S&P 500 index since 9/30 do not include the reinvestment of dividends, but this would make very little difference over such short periods of time.

It should be pointed out that, despite the market’s paroxysmal volatility on enormous volume on Black Monday 1987 (the “tape” ran late into the early hours of the next morning), it is hardly noticeable on historical charts. Indeed, for the full year 1987, the Tocqueville sample account we referred to in past reports3 actually rose 4.5% and the S&P 500 with dividends reinvested returned 5.1%.

I draw three lessons from the 1987 episode:

• When markets collapse, precautionary cash reserves protect your portfolios only marginally. In my book, therefore, cash is mostly held, not for its protective powers but for its potential: as dry powder for future purchases. When we look at it this way and we are actively searching for buying opportunities (as we should be when prices go down), “idle cash” feels much less redundant than it might at first sight.

The real question then becomes: “Once you have built up cash reserves, when and how do you put them back to work? When do you re-enter the market?”

Investment philosophy vs. discipline

The fundamentals of a business do not normally change materially in a matters of quarters or even sometimes of a few years. It follows that the same is true of the worth of that business, except for variations in a few valuation metrics such as interest rates, which analysts use to discount the value of future earnings. Shorter-term fluctuations in stock prices, on the other hand, are mostly a measure of changing crowd sentiment toward the stock market or an individual company. The challenge for serious value investors is to reconcile two often contradictory disciplines:

• Value investing, which implies that you will take advantage of the excessive fluctuations in stock prices caused by the manic-depressive (bipolar) nature of markets.

Since stock markets are such psychological mechanisms, it is a good idea to identify potential investment targets with a contrarian approach (stock or sectors that are in great disfavor) and to then assess the potential rewards based on valuation analysis.

I believe that “character”, defined by common sense, patience, courage, and perhaps occasional stubbornness is more important to investment success than IQ, economic literacy or math skills. Deciding when and how to re-enter investment markets after having raised cash during periods of “irrational exuberance” requires these qualities.

For the past year or more, much of my caution towards major stock markets, has had to do with valuation. I recognize that valuation measures like P/E (price/earnings) ratios are of little use in forecasting cyclical stock market price movements. On the other hand, many studies, including by Nobel laureate Robert Shiller, show a close, inverse relationship between P/E ratios and stock market returns for the following 7-10 years: The higher today’s P/Es, the lower the likely future returns.

In spite of today’s high valuations, we are not in a position to forecast dramatic collapses in stock prices, but the potential for large, further gains after six years of recovery seems limited. In other words, the U.S. stock market as a whole offer unattractive risk/reward characteristics. And, I believe, so do most of the other large stock markets.

I have also argued that an unattractive combination of risks and potential rewards is not a good enough reason to stop looking for opportunities in individual countries, industries and companies. But there, too, the opportunities seem scarce.

A recent article in Oilprice.com5 points out how many hedge fund managers got whipsawed by the recent behavior of oil markets:

A young (er) but thoughtful colleague just sent me the following remarks about the current U.S. stock market:

I always agree with people who are smart enough to think like me…

François Sicart (In Paris)

March 30, 2016

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

1 “What Does the Market Know?” - Oaktree Capital Management, January 20, 2016

2 “Investment Strategies” – Tocqueville – November 13, 1987

3 For example: “Secular Lessons” – February 12, 2014

4 “Common Stocks and Uncommon Profits”, John Wiley & Sons, 1997 (First Ed. 1958)

5 Rakesh Upadhyay - - Oilprice.com -- March 29, 2016

6 Irrational Exuberance, Robert J. Shiller, Princeton University Pr