“What the wise man does in the beginning, the fool does at the end” – Warren Buffett

The media and most major stock market strategists have been talking lately about beginnings and endings. The S&P 500 Index just celebrated the seventh anniversary of it taking off from its bear market lows on March 10, 2009. We enjoy watching many experts who didn’t participate in the more than tripling of the S&P 500 Index over those seven years comment and make dire predictions about the future. When it comes to negative nabobs, there must be some pretty good money in being the “boy who cried wolf” or the “blind squirrel that finds an occasional nut.”

At seven years, we are in an old bull market from a historical standpoint. This long duration is causing investors to wonder if its run is coming to an end.

Coinciding with the stock market recovery from the financial meltdown, the U.S. economic recovery is approaching seven years without a recession (defined as two consecutive quarters of GDP contraction). The following is how the consensus is described in a recent Marketwatch.com piece by Victor Reklaitis titled “59% of fund managers see an economy in its final innings — highest percent since 2008:”1

“Fund managers increasingly think this stretch of global economic growth is in its final innings, according to a Bank of America Merrill Lynch survey.

BAML found that 59% of big managers surveyed think the current expansion is in a late-cycle phase. That means it’s potentially risking a stall and could be turning off investors from economically-sensitive, higher-growth stocks.”

A good example of the consensus of economists is this quote from the same Marketwatch.com piece:

“Michael Darda, chief economist and market strategist at MKM Partners, is among the U.S. investors who thinks it’s getting late in the game and a recession isn’t that far off.

‘Our working assumption continues to be that we are now in the late innings of both the market and economic cycle, and that investors should position in a defensive and diversified fashion,’ Darda wrote in a note this week.

Once again, this is a long time to go without excessive growth and boom conditions leading to an economic contraction.”

These contractions serve to cleanse the economic sins (over-borrowing, speculation, fraud) and remind everyone that business cycles are a fact of life in a democratic capitalistic system like ours. The irony of this long period without a recession is the anemic growth levels attained and the lack of excesses created.

Since so many are currently looking for beginnings and endings, we felt this would be a good time to reflect on what we do in our attempt to be wise at the beginning. We start by constantly scrutinizing the U.S. stock market, looking for excess enthusiasm (to flee it) and excess pessimism, which could open doors to us in the shares of companies which meet our eight criteria for stock selection. We keep a close watch on the 52-week lows list and read major investment media looking for what Michael Milken called “fallen angels.”

We then run these companies of interest through our eight criteria. We are looking to see if they have the qualitative characteristics and bargain price that we need to allow an initial investment and the potential for a long-duration holding period. We check to see if the insiders of these companies have been purchasing their stock in the open market, to understand if they like the price that we see to be attractive as well. When high quality companies are purchased with the belief that valuation matters dearly, it could be the gift that keeps giving long after the beginning.

While the U.S. stock market looked for these endings and beginnings, we did not find any new companies which were beaten down by the decline in stock prices from the summer of 2015 to the lows of February 11, 2016 and fit our eight criteria for common stock selection. We constantly searched among energy companies and large industrials that took a great deal of price abuse in the last nine months. We found none which met our qualitative criteria, especially in our balance sheet and free cash flow generation criteria. Many of our existing holdings became deeply out of favor and we will seek to emphasize the best bargains among our existing holdings, even if it means concentrating our investments more than the last couple of years.

Despite reliance on our stock selection and bottom–up discipline, we are very conscious of where others are investing and look to understand the beginnings and endings of booming confidence and humiliating declines. Therefore, we thought it would be helpful to give you our opinion on the most popular stock market topics surrounding the U.S. economic recovery and any possible extension of the bull market in U.S. stocks.

Beginning an Economic Recovery: Not Ending One

Here are some of the numerous reasons we believe that we are at the beginning of an economic recovery:

- U.S. households are the farthest inside their means in 36 years.

- Residential housing starts are coming out of a depression.

- Lowest mortgage rates in 50 years.

- Cheap commodity inputs/inexpensive energy prices.

- Massive number of Millennials and household formations that we believe are about to go off the charts.

- A home building and home remodeling boom coming over the next ten years.

These factors combine to lead us to believe that the U.S. economy will be much stronger in the next ten years than is expected. We believe Main Street will outperform Wall Street as the number of families increase and housing booms!

Beginning a Bond Market Rout

- Massive mortgage creation

- A booming economy

- A middle class revival in jobs and pay

Interest rates peaked in 1981, and as a result, many experts have been pummeled and ridiculed for predicting higher interest rates during the last three years. Since we don’t invest in bonds and don’t mind looking foolish at the beginning, we will go on record as saying that we believe quality long-term bond investors are at great risk. If 86 million people go from being afraid of buying a house to thinking it is a good idea, welcome to 1975 again. Current rents are the highest relative to mortgage payments as they have been in 50 years. In the long-run, the markets are a weighing machine

We find most bond bulls are using minuscule German Bund rates or negative Japanese bond rates as a reason to be bullish about ten-year Treasury Bonds at 1.9%. It sounds to us just like investors buying Microsoft and Cisco in 1999, because they looked cheap compared to most the dot-com tech bubble glamour stocks like AOL, Lucent and Geo-Cities.com. They did relatively well, because Microsoft only lost 50% of its market capitalization and Cisco only lost 80% of its value when the bubble broke. A hollow victory, to say it kindly.

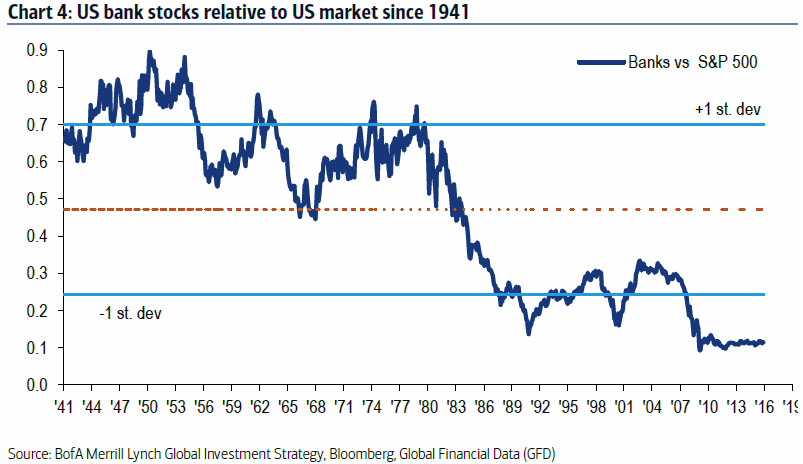

Beginning a Great Era in Bank stocks

Source: BofA Merrill Lynch Global Investment Strategy, Bloomberg, Global Financial Data (GFD). Data for the time period 1/1/1941 to 3/8/2016.

This chart speaks for itself. If valuation matters dearly and bond rates go up the next five years, we could be playing the song "Happy Days are Here Again," as it pertains to our bank stock holdings.

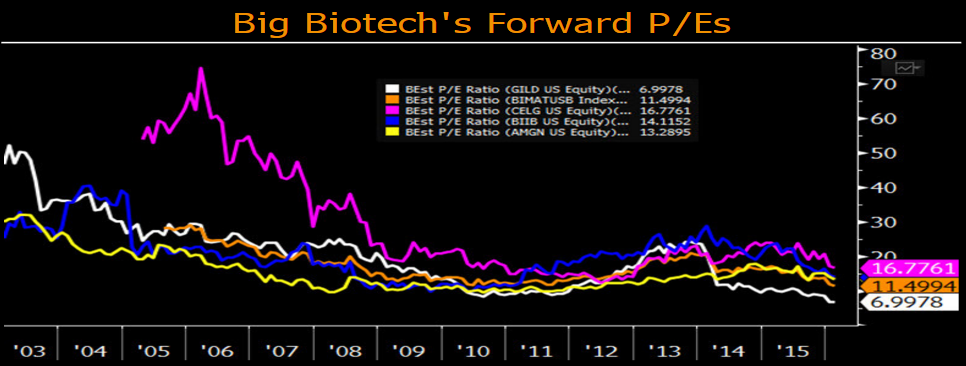

A new beginning in long-term bull market for Pharma/Biotech

Source: Bloomberg. Data for the time period 1/1/2016 to 2/8/2016.

For investors who like relative value trades, you will rarely see our nation’s most successful biotech companies this cheap relative to other stocks. Last time we checked, more people, and hundreds of untreatable diseases and chronic illnesses, are left to be vaccinated, treated or cured.

However, our bullishness on the U.S. economy is not matched by a bullishness for the U.S. stock market as represented by the S&P 500. The index is heavily weighted in revenue which comes from outside the U.S. and is unlikely to gain the most benefit from the beginnings we foresee. In fact, many of the most popular trends of the last five years seem to be ending. China’s economic miracle is now a questionable perpetuation of GDP growth. We believe commodities and emerging market nations which fed China’s miraculous infrastructure-led growth will struggle for years to find a better business model.

Technology as an end-all appears to be dying. If history is any guide, the over-pricing of FANG stocks in 2015 has laid the groundwork for stock price underperformance. Remember, valuation matters dearly in both directions. It is very hard for a successfully run and fast-growing company to overcome massive stock price over-valuation. For this reason, to quote my Shark Tank friends, when it comes to expensive technology companies, “I’m (we are) out!” Lastly, if the great bond bull market that began in 1981 ever dies, the idolization of it dies as well, leaving its worshipers to be orphaned and estranged. Stock market investors know this well and only need to look back to 2000-2002 or 2007-2009 as examples.

Our attempt to be wise at the beginning is centered on our practice of bottom-up stock picking discipline, based on our eight criteria. The voting machine of the stock market can be driven by the fools at the end. We want to be conscious of when it offers us high-quality companies at significant discounts. Thank you for your ongoing confidence and trust in our methodology.

1 http://www.marketwatch.com/story/economic-growth-is-in-the-late-innings-fund-managers-say-2016-03-16

Disclosure

The information contained in this letter represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

This Missive and others are available at www.smeadcap.com.

Follow us on Twitter @SmeadCap