One of the biggest questions equity investors are facing right now is whether to stay defensive or to turn up the cyclical heat on any pullback. We’ve been writing on this very topic for the last few weeks. Staying defensive is in essence a bet that counter-cyclical stocks will continue their leadership trend that has persisted for the last decade and especially since early 2011. It’s also a bet that long-term interest rates will stay grounded thanks to persistently low growth and inflation expectations. Taking a crack at cyclicals, on the other hand, is essentially expressing a view of rising growth and inflation expectations and the rise in long-term rates that would accompany that scenario. Such an expression is hardly for the faint of heart since betting on cyclical stock market leadership has been a disastrous tactic pretty much all the time since 2006 outside of the short-lived reversal in 2009.

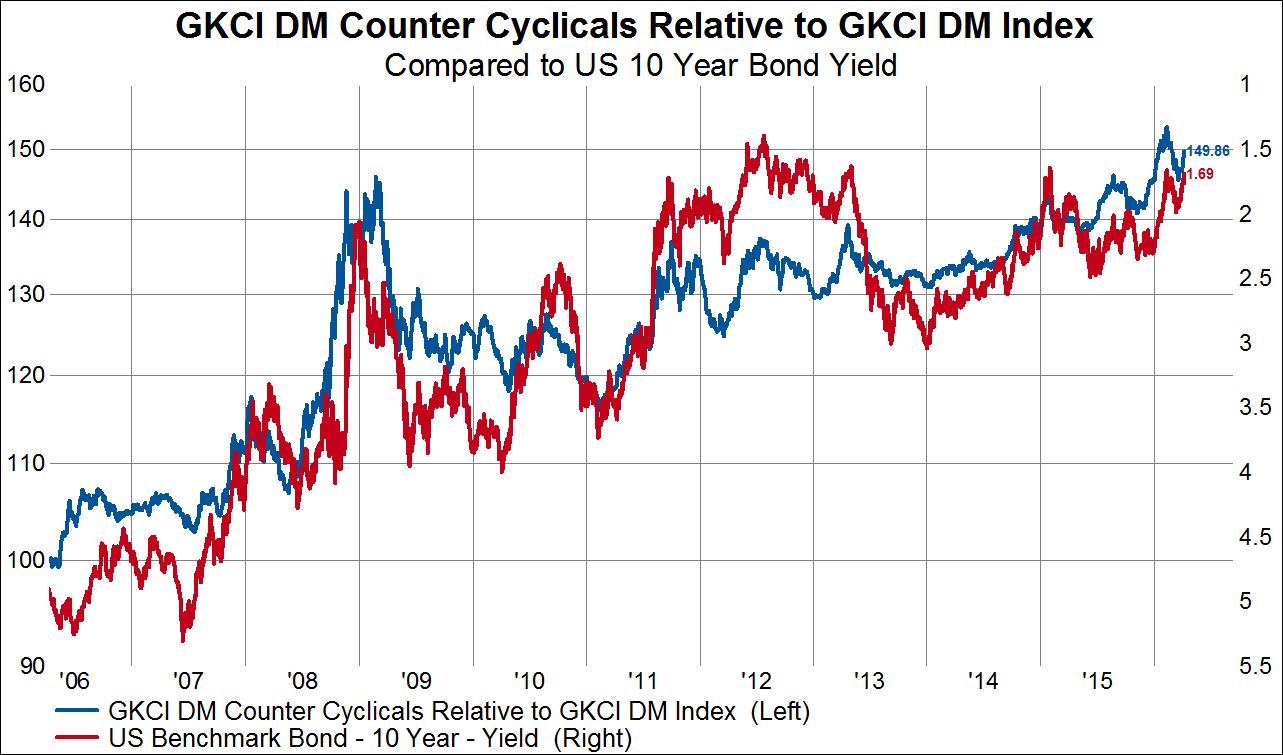

In the first chart below we show our GKCI DM Counter Cyclical Index relative to all DM stocks (blue line, left axis) and overlay the 10-year treasury bond yield (red line, right axis, inverted). When rates fall, counter cyclical stocks outperform the market.

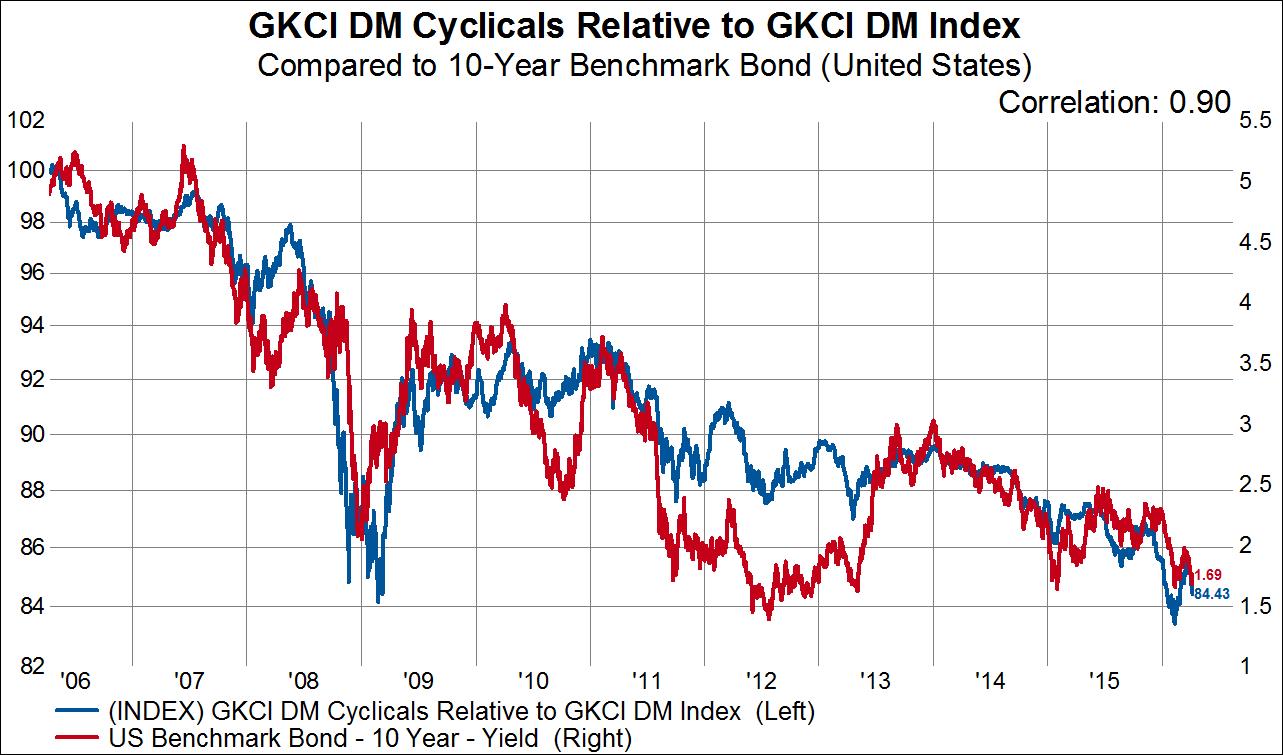

In the next chart we show our GKCI DM Cyclical Index relative to all DM stocks (blue line, left axis) and overlay the 10-year treasury bond yield (red line, right axis, inverted). When rates fall, cyclical stocks underperform the market.

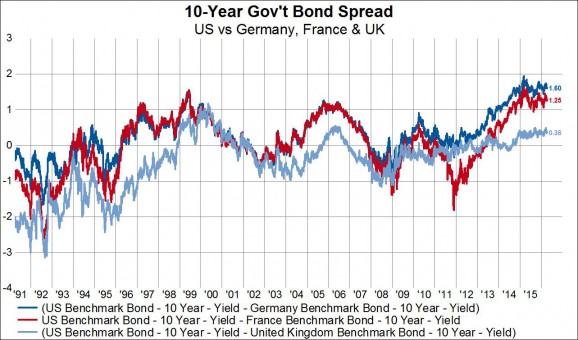

So the obvious important question to answer to help determine one’s equity positioning is what are long rates going to do? Our crystal ball is no shiner or more prescient than anyone else’s, but here’s some easily digestible food for thought. The global economy has been locked in a high debt, low growth environment for years and demographics are a headwind for most of the developed world and China. This environment alone argues for a lower “neutral” rate, as Fed Chair Janet Yellen would put it. But there is more. US 10-year rates are the highest among the G7 and higher than all developed market countries except Singapore, Australia and New Zealand, as the table below highlights. Furthermore, the spread between 10-year US Treasuries and Bunds, OATs and Gilts is near the highest level going all the way back to 1990. That is to say, there is plenty of room for flat to lower US Treasury yields and not a whole lot of impetus for higher yields. All this implies than the odds of continued counter-cyclical stock market leadership probably outweigh those of cyclical stock market leadership unless or until something dramatically changes with regard to growth or inflation expectations or demographic realities.