After a turbulent start, the first quarter ended on a calmer note. There were moments when the U.S. economy appeared to defy expectations, and there were moments when the outlook was not rosy. On net, forward momentum remains in place.

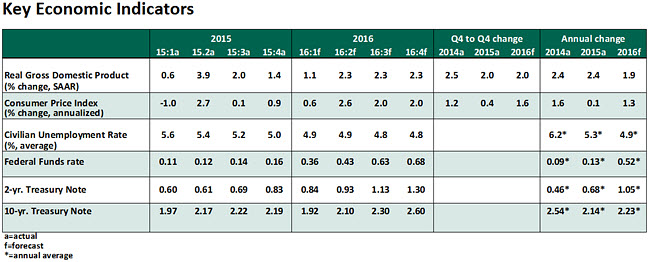

Concerns about the U.S. economy drifting into a recession appeared to have eased. Real gross domestic product (GDP) grew 1.4% in the fourth quarter. This puts economic growth for 2015 at 2.4%, matching the performance of 2014. The first quarter of 2016 is predicted to show a deceleration of business momentum, but prospects for the balance of the year remain favorable.

Key Elements of Forecast

- Consumer spending slowed in the first quarter after a nearly 2.8% increase in the second half of 2015. Although auto sales are holding at a high level (17.2 million units sold in the first quarter), they fell about 15% in the first quarter, which brought down the quarterly reading of consumer spending. Real disposable income has risen at an annual rate of 3.8% in the last three months, the best in the past 12 months. Employment conditions are favorable. These factors support expectations of a near-term pickup in consumption.

- Outlays on non-residential structures and equipment spending fell in the first quarter. The latter was partly led by the weakness in energy-related investment expenditures. Equipment spending is projected to present another quarter of disappointing performance. The good news is that new orders and production indexes of the Institute of Supply Management’s March survey suggests an expansion in activity. Oil prices are stabilizing, which should help to contain the weakness of the energy industry’s investment outlays.

- The housing sector appears poised for a modest pickup. The Mortgage Purchase Index advanced in the past month as mortgage rates declined. The Pending Home Sales Index, a leading indicator of sales of existing homes, moved up in February. On the supply side, housing starts rose in February after two consecutive monthly declines. On the demand side, sales of new and existing homes show small gains on a 3-month moving average basis. Home prices maintain a gradual upward trend. Residential construction outlays during January and February are solid.

- Inflation in the United States has moved to a different stage. Overall inflation, based on the personal consumption expenditure price index, is much higher than a few months ago. The year-to-year change in the core measure, which excludes food and energy, is closer to the Federal Reserve’s 2.0% target. Although Fed Chair Yellen is doubtful about the durability of recent gains in inflation, it is hard to see inflation readings move lower as the economy moves toward full employment.

- The economy continues to add jobs at a decent clip: about 209,000 jobs on average in the last three months. The increase in the unemployment rate to 5.0% in March was due to a rise in the participation rate, the fourth consecutive monthly gain. Both hiring and quit rates rose in February and confirmed the strength of the labor market.

- The 10-year U.S. Treasury note is trading a bit below 1.80% in the last five trading sessions, down roughly 45 basis points from the start of the year. It largely reflects weakness in global economic conditions and risk aversion more than domestic economic fundamentals. For perspective, the German 10-year government bond, now trading at slightly above 10 basis points, is one of the few alternative risk-free bonds. We expect modestly higher yields will prevail as global economic conditions stabilize in light of the supportive monetary policy actions other major central banks have put in place recently.

- The Fed holds the view that “global developments have increased the risk associated” with the outlook for the U.S. economy. Incoming economic data have not raised new red flags about global economic conditions since the Fed’s meeting in March. Market participants are monitoring international economic developments closely for early hints.

- The April Federal Open Market Committee (FOMC) is largely expected to end without any change in Fed policy. We think the data-dependent Fed will find enough evidence to support a higher policy rate by the June FOMC meeting.