India’s Central Bank cuts key policy rate by 25bps

What were the market expectations? – 25 basis point rate cut

In its last monetary policy review in Feb 2016, just before the union budget, the Reserve Bank of India (RBI) while keeping the policy rate unchanged had stated that it is looking for clarity on the plans for fiscal consolidation, gauge progress on structural reforms and the inflation trend for easing of policy rates. Since then, almost all the conditions for monetary easing had been fulfilled. The central government stuck to the fiscal consolidation roadmap it had announced last year by keeping the fiscal deficit at 3.5% for FY17, while the Inflation undershot RBI expectations again, with the Mar’16 print likely to be closer to 5%, against RBI projections that are closer to 5.5%. Growth scenario remained rather muted, as witnessed by sluggish industrial growth.

In this background the market was expecting a minimum of 25 bps rate cut. Besides, the system had been grappling with huge liquidity deficit situation, caused both by structural as well as to a certain extent caused by seasonal factor. These tight conditions were being considered to be an impediment for effective monetary transmission. In view of this, the market was also expecting policy measures from RBI on addressing the liquidity deficit problem as well.

What the RBI has delivered?

In line with the market expectations, RBI in its first bi-monthly policy, announced the following monetary and liquidity measures.

- 1) Reduction in policy repo rate under the liquidity adjustment facility (LAF) by 25 basis points from 6.75% to 6.5%.

- 2) Narrow the policy rate corridor from +/-100 bps to +/- 50 bps, by reducing the MSF rate by 75 bps to 7% and increasing the reverse repo rate by 25 bps to 6%.

- 3) Reduce the minimum daily maintenance of the cash reserve ratio (CRR) from 95% of the requirement to 90 per cent, while keeping the CRR unchanged at 4.0 per cent of net demand and time liabilities (NDTL);

- 4) Maintain liquidity deficit in the system at neutral level, from the existing one per cent of NDTL to a position closer to neutrality.

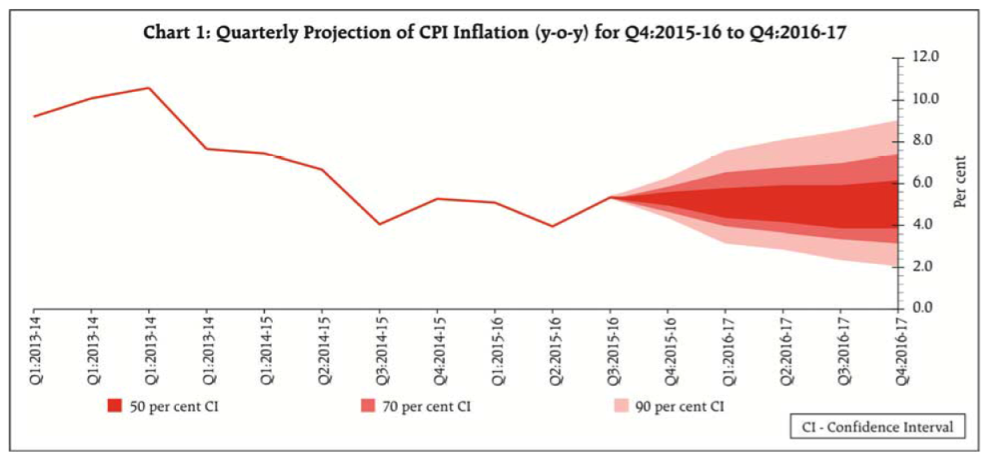

RBI on Inflation – Average around 5%

RBI has kept the inflation target for FY17 unchanged. It expects the inflation to decelerate modestly and remain around 5% during the year with small inter-quarter variations. While it highlighted on uncertainties surrounding this inflation path emanating from recent unseasonal rains, the likely spatial and temporal distribution of monsoon, the low reservoir levels by historical averages, and the strength of the recent upturn in commodity prices, especially oil, it pointed out that there are certain offsetting downside pressures as well stemming from tepid demand in the global economy, Government’s effective supply side measures keeping a check on food prices, and the Central Government’s commendable commitment to fiscal consolidation.

|

Source: RBI |

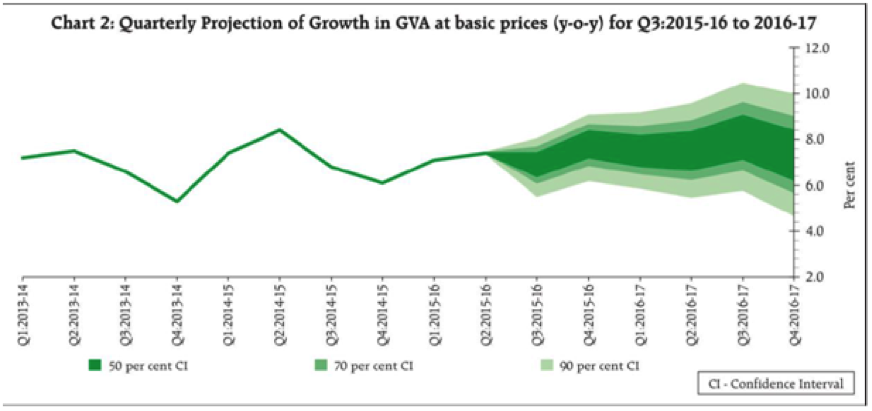

RBI on GDP Growth

RBI retained its GDP growth projection for F717 at 7.6%, assuming a normal monsoon, the likely boost to consumption demand from the implementation of the 7th Pay Commission recommendations and OROP, and continuing monetary policy accommodation. However, it also highlighted that the persisting corporate sector stress and risk aversion in the banking system, and the weaker global growth and trade outlook could impart a downside to growth outcomes going forward.

|

Source: RBI |

Clarity on FCNR (B) deposits

In September 2013, RBI opened up the FCNR window to attract foreign deposits to stem the Rupee’s fall at that time. The minimum lock-in for these deposits which were SLR exempt, was kept at 3 years. Now these deposits are coming up for maturity starting September 2016. In one of our previous note, we had highlighted the lack of clarity around how the RBI will tie up the forex required for this ~$26-30bn lumpy maturity. In this monetary policy statement the RBI clarified that these repayments and swaps are fully covered under its forward purchases program. Moreover, RBI will monitor developments closely to contain any unanticipated market volatility associated with the repayment.

Forward guidance

After the cumulative easing to the extent of 150 bps beginning Jan-215, RBI continues to maintain an accommodative stance, taking comfort from the improving macro-economic situation. While maintaining an accommodative stance going forward, RBI stated that it will continue to watch the financial developments in the months ahead with a view to responding with further policy action as space opens up.

Our View

We believe that with the latest cut RBI is nearing the end of its policy easing cycle. It may be noted that, Reserve Bank of India had earlier underlined inflation-adjusted interest rate of about 1.0-1.5% - as appropriate for the current phase of Indian economy. Based on the one-year Treasury bill rate and one-year inflation expectation of 5%, the real interest rate as on now stands in the range of 1.5-1.75%, thus there still exists a small window of opportunity for further monetary easing by a maximum of 25 bps.. However, a cut beyond 25bps, will only lower the real rate below RBI’s comfort range, given the upside risks to inflation pointed out by RBI.

The RBI measures to bring the system liquidity to neutral along with the narrowing of the corridor to 50 bps and CRR maintenance at 90 percent will allow overnight rates to remain very close to the repo rate or even drift marginally lower. This will ensure that the easy policy stance percolates to the real economy and materially lowers financing costs.

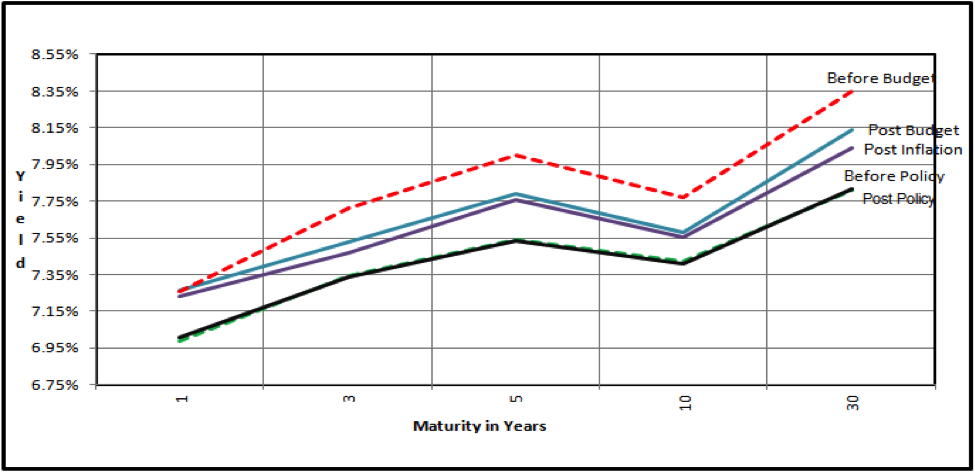

Bond Market Reaction

The reaction of the bond market has been quite muted, as the market had already rallied by 15-20 bps in the run up to the policy announcement in the expectation of 25 bps rate cut. In fact the bond yields have softened quite substantially in the last month (by 40-45bps) post the budget announcement and retail inflation for the month of February, 2016.

|

Source: RBI |

Going forward, we expect that the 10 year benchmark yield to trade in a broad range of 7.25-7.5%. We also believe that the various measures to address the liquidity situation will narrow the corridor on the overnight rates, leading to further steepening of the yield curve

Disclaimer: The views expressed are of Tata Asset Management Ltd. and are in no way trying to predict the markets or to time them. The views expressed are for information purpose only and do not construe to be any investment, legal or taxation advice. Any action taken by you on the basis of the information contained herein is your responsibility alone and Tata Asset Management will not be liable in any manner for the consequences of such action taken by you. Please consult your Financial/Investment Adviser before investing. The views expressed may not reflect in the scheme portfolios of Tata Mutual Fund.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully before investing.