Fed Watching For Dummies: Credit Spreads Are Driving Monetary Policy

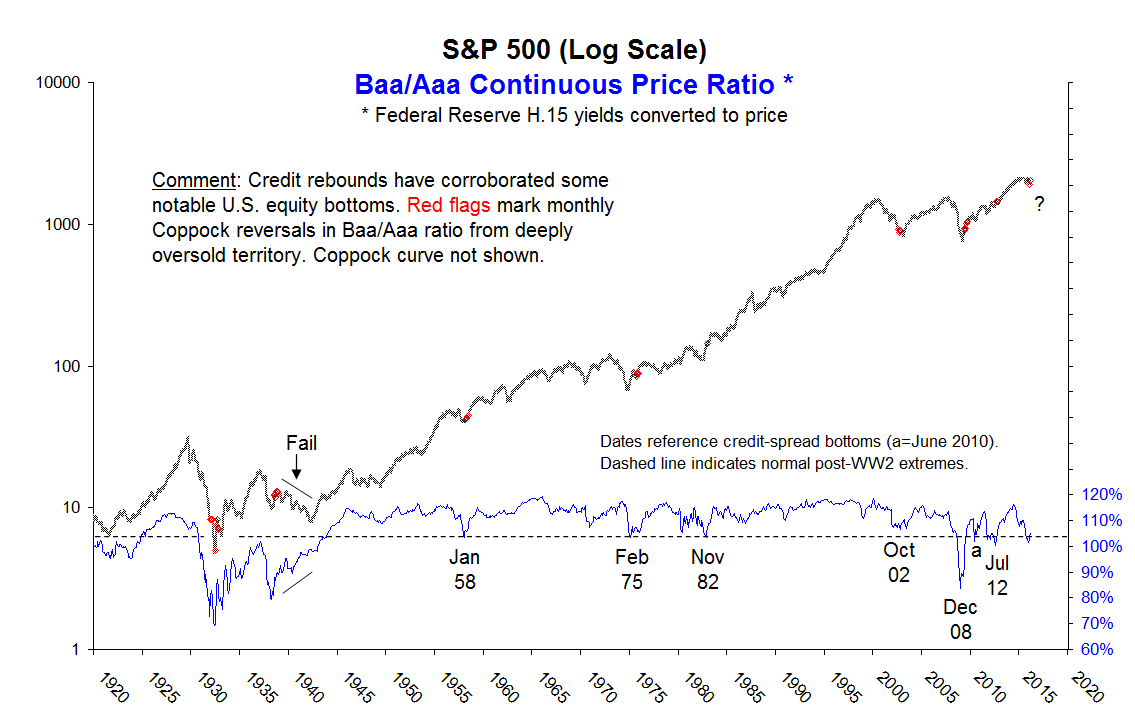

On March 29th, Janet Yellen outlined three factors warranting a new, dovish bias: energy prices, currency dislocations, and global equity turmoil. While all of this makes perfect sense, we think the real driver of FOMC policy is corporate credit. In recent months, the price ratio of Baa-to-Aaa U.S. bonds has deteriorated to levels not seen since June 2010 and July 2012. (See chart below.) Those cases were followed by QE2 and QE3, announced in November 2010 and September 2012, respectively.

The Fed would obviously like to avoid credit-market conditions akin to 2008-2009, when spreads widened to levels not seen since the 1930s. Janet Yellen certainly cares about energy prices and currency fluctuations, but their effect on corporate credit is where the rubber meets the road. The Federal Reserve Bank is, after all, a banker’s bank… at the heart of the credit system.

So there is nothing unusual about last week’s “shocker.” Expect new rounds of monetary accommodation whenever credit spreads test their post-crash extremes.