Emerging Markets Update: Is Now the Time for Emerging Markets?

Although many financial pundits make their predictions for future stock returns based on past results, such an approach is dangerous in our view because it doesn’t consider valuations and can lead to missed opportunities as investors chase performance in the most-speculative areas of the markets. Moreover, while it’s true that positive or negative price momentum can persist for a while, momentum alone isn’t usually a good indicator of longer-term investment results.

In the case of emerging markets, we believe the uninspiring returns over the past five years may be contra-indicators of what lies ahead. In addition to many flat and down stock prices — which indicate an overall lack of froth and speculation — selectively chosen emerging-market companies offer growth potential, reasonable valuations, attractive dividend payouts, and the chance to benefit from stabilizing commodity prices and from strengthening currencies. We also think the role of innovation in emerging markets has been woefully underappreciated.

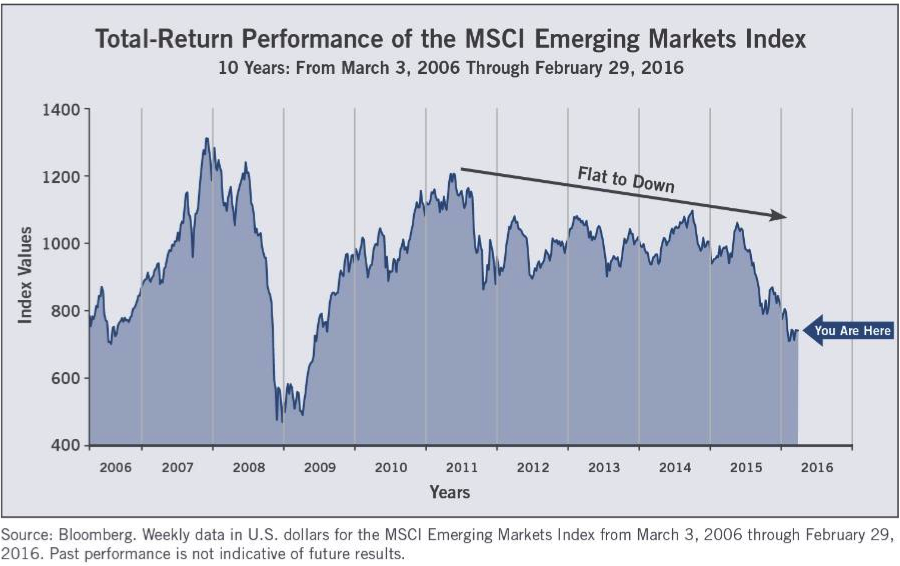

Emerging Markets: You Are Here

The chart below indicates the dollar-denominated total-return performance of the MSCI Emerging Markets Index over the last 10 years. As we can see, the Index is currently well below where it was five years ago — and also significantly below its 2007 peak prior to the Global Financial Crisis (GFC).

Now let’s look at the dollar-denominated total-return performance of the MSCI World Index (an index of developed markets) over the last 10 years, as presented in the chart below. In this case, the Index has made substantial progress since five years ago — despite significant volatility during the past several months.

Another way to look at this information is to plot the ratio of the MSCI Emerging Markets Index divided by the MSCI World Index (with both indices calculated on a total-return basis). This ratio over the past 10 years is shown in the chart below.

Here we see that the ratio is currently close to its lowest level in the entire 10 years, and that developed markets have dramatically outperformed since 2010. If we believe most trends eventually reverse course, we may be close to a period of outperformance for emerging markets. Looking at how the ratio has fluctuated over time, it’s evident that such a period of outperformance culminated in late 2010 after having begun in 2008 at a level even higher than today’s level.

A Tale of Two Market Types

So, if many emerging-market companies have for quite some time appeared reasonably valued — or even undervalued — what has accounted for their stock-price declines? We believe there are several reasons that have to do with the two main types of emerging markets.

The first market type includes major commodity-exporting countries such as Brazil, Colombia, Russia and Malaysia. The second market type includes manufacturing and service-oriented countries such as China, India, Mexico, South Korea and Taiwan.

The trend of falling oil prices over the past two years was viewed as a modestly net-positive factor for developed markets because it took some pressure off corporate and consumer budgets — despite real hardships in the energy sector. But for emerging markets, this trend was viewed very negatively because some of the most-prominent emerging-market countries are major exporters of oil and other commodities.

Exacerbating the damage to emerging markets overall was the slowdown of economic growth in China. Investors feared that this slowdown would lead to even less demand for petroleum and metals. In addition, there was concern that China might materially devalue the yuan in an effort to boost the country’s exports of manufactured goods and thereby lift its economy. Such a devaluation, it was feared, could then lead to devaluations in other currencies as nations around the world would seek to maintain their manufacturing-export competitiveness versus China.

Weak prices for commodities also put additional downward pressure on the currencies of commodity-exporting countries such as Brazil and South Africa. At the same time, talk of potential interest-rate increases by the U.S. Federal Reserve (Fed) — along with decent economic performance in the United States — caused the U.S. dollar to rise to its highest level in about 15 years. For those with their investments denominated in dollars, this meant that emerging-market holdings performed even worse.

Capital Outflows From Emerging-Market Economies

Despite the significant differences among emerging markets, many investors tend to view these countries as belonging to one category. That view — combined with the proliferation of index-based investing and redemptions from sovereign wealth funds — caused broad capital outflows from emerging-market economies in the last two years, as shown in the chart below.

Capital flows represent purchases and sales of financial assets such as stocks, corporate bonds and government bonds. Negative net capital flows (outflows) meant that money was leaving emerging markets in aggregate. And we believe index-based funds, which buy and sell emerging markets as one basket, caused investors to be less discriminating among attractive and unattractive countries and businesses. In other words, we think the baby was thrown out with the bathwater.

Fortunately, this indiscriminate selling means that valuations have become particularly appealing in certain segments of emerging markets. As a result, we believe now is the time to take an active (non-index) approach in an effort to narrow the universe and find what we think are some of the best stocks that were previously sold off as part of the passive emerging-market basket trade.

Growth Potential, Reasonable Valuations and Dividend Yields in Emerging Markets

So far, we’ve addressed why emerging-market stock prices are well below their highs of recent years. And before we discuss the catalysts that may cause prices to move sustainably higher, we should describe the reasons why we believe certain emerging-market businesses are currently so attractive.

The first reason is growth potential. Although not all emerging markets are experiencing strong economic growth, several emerging-market countries — such as India, Indonesia and the Philippines — have gross domestic product (GDP) growth rates that exceed 5%. In addition, countries like Mexico, South Korea and Thailand have GDP growth rates that are more modest but are still close to the level in the U.S. and above the levels generally seen in Europe.

It’s true that strong GDP growth alone doesn’t necessarily correlate with rising stock prices. But when we combine meaningful GDP expansion with decent sales and earnings growth at the company level, we have higher expectations for performance in the stock market — particularly among companies that are serving domestic (home-country) consumer demands.

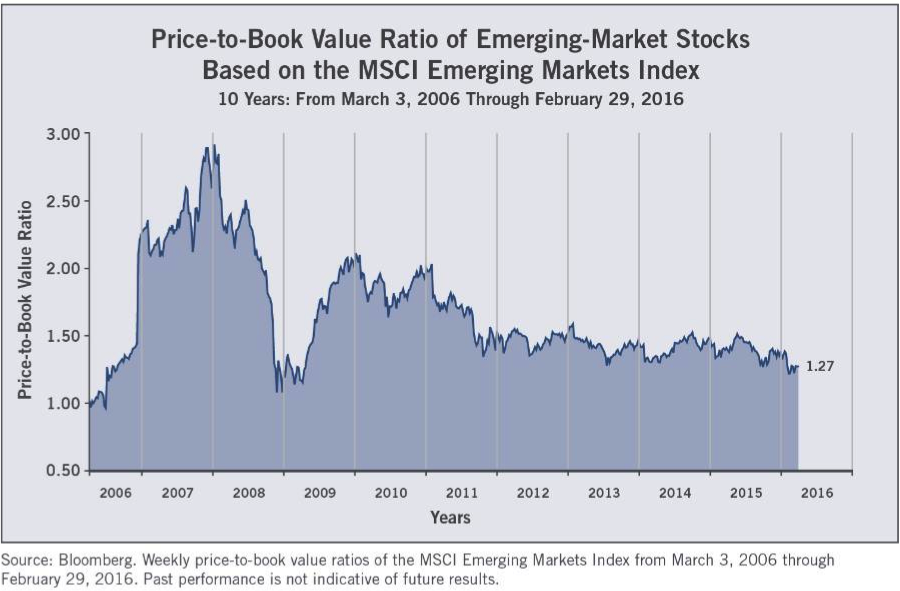

The second reason has to do with the company-valuation levels we’re finding among emerging markets. Whether we look at price to book value, price to cash flow, price to earnings or cyclically adjusted price to earnings, some of the world’s least-expensive companies are in emerging markets. For example, emerging-market stocks on average are trading at a ratio of about 1.3 times book value, which — as shown in the chart below — is close to the bargain levels reached in 2008 during the GFC. And when we combine the attractive valuations with the better growth rates we’re seeing, we get particularly optimistic about our investments in emerging markets.

The third reason is that many emerging-market businesses have a propensity to pay dividends. This is particularly appealing in an environment where interest rates are close to zero or are actually negative in many developed-market countries. Even the U.S. Fed refused to take negative interest rates off the table as a future tool of monetary policy. Moreover, dividends have historically accounted for a large portion of long-term stock returns. And we think dividends will become increasingly important in the continued low-interest-rate, disinflationary environment we see going forward.

Commodities Versus Manufactured Goods and Services: The Real Story for Emerging Markets

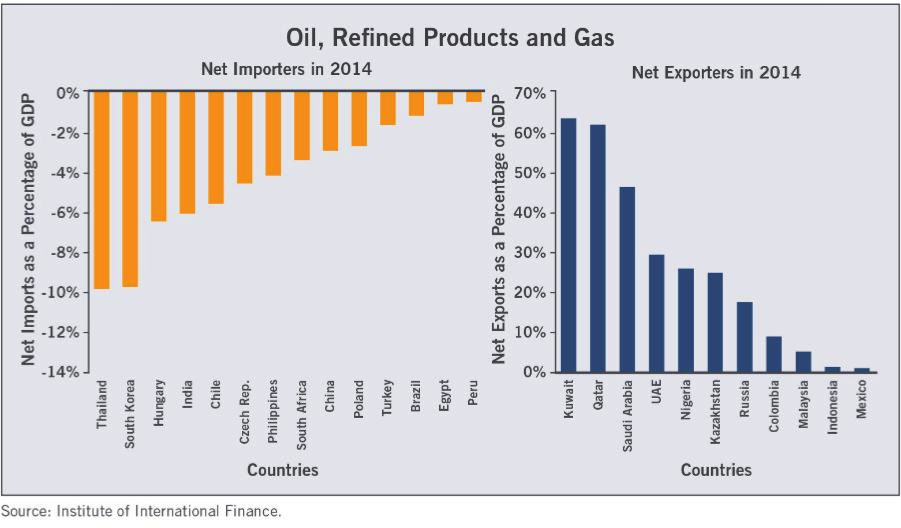

There’s no doubt that declines in the prices of oil and other commodities have had negative impact on emerging markets, many of which are major exporters of commodities. But the bigger picture is that even among net exporters of oil, refined products and gas, several emerging-market countries depend on these commodities for less than 20% of GDP.

Moreover, there are many emerging markets that actually benefit from lower commodity prices because these countries are net importers of oil, refined products and gas. Net importers and net exporters of oil, refined products and gas are shown in the chart below.

Even among major oil exporters, the effects of the energy situation may be counterintuitive. Take Indonesia, for example. Although Indonesia is a major oil exporter and a member of the Organization of Petroleum Exporting Countries (OPEC), growing internal demand for energy has also made Indonesia a large importer of petroleum.

Cheaper oil has allowed Indonesia’s president, Joko Widodo, to abolish the national fuel subsidy, which had accounted for approximately 15% of the state budget and drained about $19.6 billion from government coffers in 2014. Having used the windfall in 2015 to shore up the country’s public finances, in 2016 Indonesia is looking to spend the extra money on infrastructure projects designed to help the economy perform closer to its true potential. We believe these developments, along with a strengthening currency, declining fiscal deficits and improved capital flows into the country, bode well for Indonesia’s economy and consumers. Similarly, India is using a portion of its windfall from lower energy prices to improve its infrastructure.

Broadly speaking, lower commodity prices should benefit the following types of emerging-market businesses: high- and low-tech manufacturers, textile producers, pharmaceutical firms, companies addressing the market for outsourced operations, and providers of consumer products and services. All of these businesses use energy and/or other natural resources. So lower commodity prices, all other things being equal, reduce operating costs and raise profits. For domestic consumer-oriented companies, lower energy prices should also translate into more spending money in people’s pockets.

On related matters, the disinflationary forces described in this paper are improving current-account positions in many emerging-market countries and are taking some pressure off the countries’ central banks, which are now less inclined to raise interest rates. These conditions should allow emerging-market bond yields to continue falling, which is positive for businesses and investors alike.

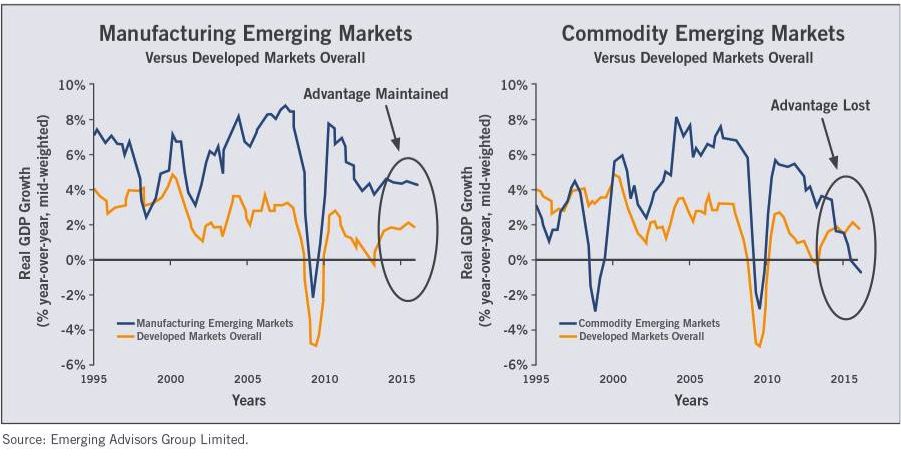

The chart on the left below indicates how manufacturing-oriented countries in the emerging-market universe have maintained their overall GDP growth advantage versus developed markets. And the chart on the right indicates how commodity-oriented countries in the emerging-market universe have lost their advantage — actually falling below the overall GDP growth in developed markets.

In these charts, manufacturing-oriented emerging markets are defined as economies where final manufacturing products account for more than 50% of exports by revenue. And commodity-oriented emerging markets are defined as economies where the majority of exports are primary resources, fuel and resource-based processing.

A final point about commodities is that demand has softened — but for many commodities, demand hasn’t fallen off a cliff. For example, notwithstanding the headlines, China’s GDP growth is still above 5% annually and Chinese imports of crude oil actually rose in 2014 and 2015 from year-earlier levels — as did China’s share of world imports. Consequently, even if they don’t increase much, we think major commodity prices will begin to stabilize around current levels. This should calm investors’ fears somewhat and create a better environment for stock prices.

Despite Its Problems, China Is Still an Economic Powerhouse

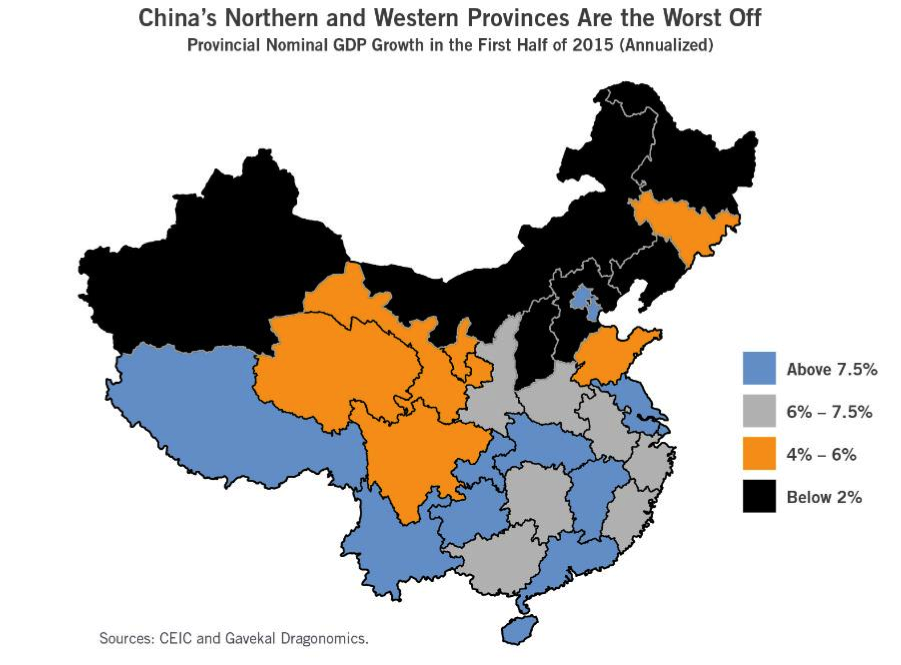

As mentioned, China’s overall GDP growth is still above 5% and the country’s consumption of oil hasn’t declined. But economic growth is uneven throughout China’s provinces — with the northern and western areas faring the worst, as indicated in the illustration below.

China’s other problems include the following: 1) high corporate and government debt incurred for the country’s massive overbuilding of its infrastructure and manufacturing capacity, 2) the likely devaluation of the Chinese yuan after years of being pegged to the U.S. dollar, 3) continued attempts by individuals and businesses to move capital out of the country, and 4) excessive stock valuations — particularly on the mainland exchanges.

Having said all of this, we think China is capable of addressing its problems and will not cause much additional contagion in the emerging markets that are home to high-quality manufacturers and service providers. Already we are seeing signs that China is shifting from an infrastructure-led economy to a more consumer-led economy. This shift could be helped by the fact that the Chinese people have low debt levels and are strong savers with an overall household savings rate of about 30%. As a result, the people have the ammunition to start spending. By the same token, such a shift toward consumption could help alleviate debt at the corporate and government levels.

Regarding the Chinese yuan, we think a further devaluation could be significant — perhaps 10% to 15% — but not so large as to cause panic in other emerging markets. Remember, if the U.S. dollar also declines meaningfully, this will alleviate some of the downward pressure on the yuan. And if the yuan is under less pressure, the desire to move capital out of the country will also lessen.

Regarding excessive stock valuations in China, we believe there are only two ways to fix that problem: The first is for stock prices to come down. The second is for stock prices to stagnate while the companies eventually grow into their valuations. Either way, we think the best approach for Wasatch is to underweight our investments in mainland Chinese stocks. And when we do want to selectively add exposure to China, we believe the best way will be through stocks traded in Hong Kong, where valuations generally have been more reasonable.

But won’t the malaise in Chinese stocks infect most other emerging-market equities? We don’t think so. Just like global markets decoupled from Japan’s troubles in the late 1980s and throughout the 1990s, we think emerging markets have begun to decouple from China.

It’s true that China is the second-largest economy in the world and has been a powerful engine for economic growth around the globe. It’s also true that the initial phase of the Chinese slowdown has been a painful adjustment period. But aside from some of the large commodity-exporting countries, China isn’t a major trading partner with most other emerging markets.

This means that the best emerging-market investments may have narrowed to the less commodity-oriented markets and the countries with relative political stability — countries such as India, Mexico, the Philippines, South Korea, Taiwan and Thailand. Despite this narrowing of the opportunity set, we believe we still have plenty of room to find great companies given the vastness of the markets. In Mexico, for example, the economy appears to be holding up well and many of the country’s manufacturers are benefiting from U.S. demand as they take market share from Chinese competitors.

Innovation in Emerging Markets

The pace of innovation in emerging markets is another reason to be optimistic regarding certain businesses in these countries. But can investors make money from the innovation taking place? The short answer is “yes.”

Emerging-market companies are typically less well-researched and therefore more reasonably priced than their developed-market peers. Once these companies have clearly demonstrated their success, however, they’re likely to be rewarded with considerable public and private valuations. Investors can profit from these valuations, especially as liquidity continues to improve in emerging-market stock transactions.

While Joseph Schumpeter — who popularized the concept of “creative destruction” — regarded innovation as a defining feature of capitalism, we believe innovation has more to do with people’s desire to improve their lives. What may be surprising to some investors is that innovation is prevalent around the world in developed markets, in emerging markets — and even in frontier markets, which are considered the least advanced of all. Moreover, contrary to the popular belief that innovation is best encouraged by “government just getting out of the way,” governments often play important roles in setting priorities and working in partnership with new entrepreneurs and established players.

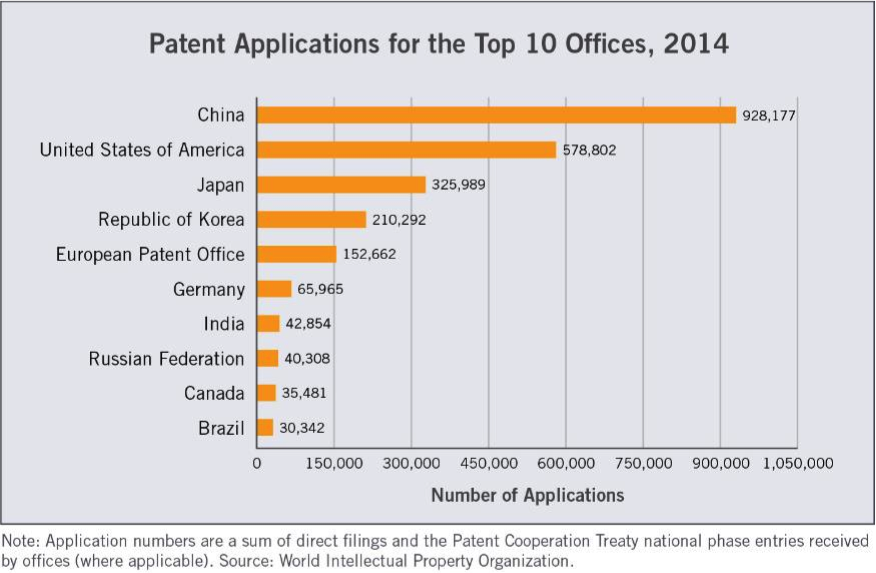

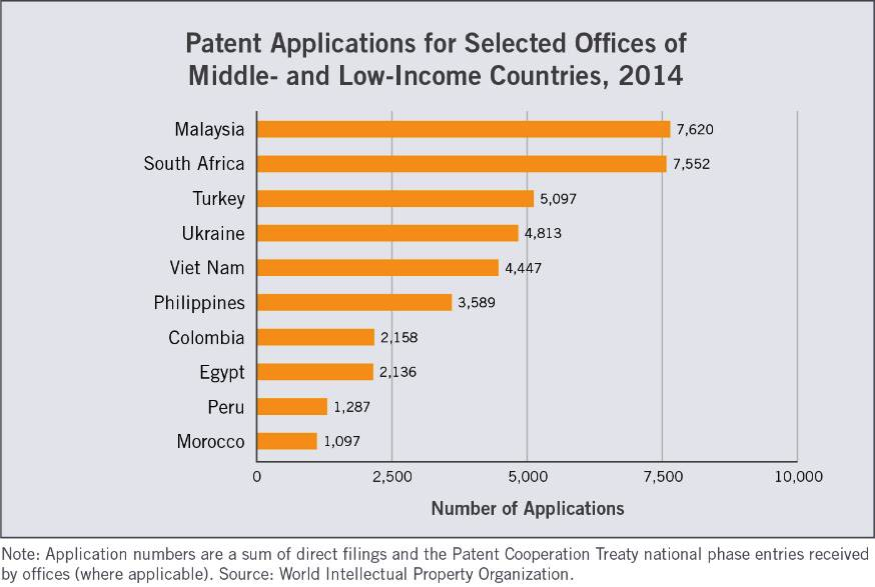

The number of patent applications is one gauge of innovation. By that measure, the charts below indicate where innovation is really occurring. Here we see that the type of government doesn’t appear to be the driving force.

Among the top 10 offices for patent applications, five are in emerging markets. In fact, China is #1, well ahead of the United States and Japan. Perhaps even more surprising is the diversity of countries in which innovators are applying for patents and the total number of patent applications by offices in emerging and frontier markets.

When we think about innovation, Silicon Valley and the greater San Francisco Bay Area often come to mind. But some of today’s social-media, SaaS (software-as-a-service), cloud-computing and other high-tech companies were actually started as much as half a world away. What’s more, innovation goes well beyond these tech industries.

In addition to Internet-based companies, innovation occurs in services that affect the quality of our lives — in health sciences, for example. Another fertile ground for innovation is in the revolution of a business process, whereby a company uses existing technology in new ways to leapfrog competitors.

Within the emerging and frontier universe, several countries are especially rich in natural resources as we’ve described. In addition, most emerging and frontier markets have young and growing populations with consumers increasingly moving into the middle class. As a result, many investors in these markets tend to focus mostly on oil and other commodity exporters, and on makers of basic consumer staples. But there are so many other investment opportunities.

The growing middle classes in emerging and frontier markets are also being served by more-innovative companies. Investors can participate in the growth of these companies, many of which are publicly traded on local stock exchanges — and some of which are even listed on major exchanges around the world.

Currencies and Purchasing-Power Parity

Now that we’ve described the reasons why certain emerging-market businesses are currently so attractive, we can discuss the catalysts that may cause stock prices (denominated in U.S. dollars) to move sustainably higher. In this regard, we think an analysis of currency movements and purchasing-power parity indicates that most emerging-market currencies have seriously overshot in their weakness against the U.S. dollar. A reversal of this trend would be very positive for emerging-market investors. Moreover, we believe such a reversal of the five-year trend may have already started or may be close at hand.

Many factors, including strong geopolitical forces and higher interest rates in the U.S., have led to the dollar being excessively valued relative to other currencies — especially emerging-market currencies. If emerging-market currencies reverse course and strengthen against the U.S. dollar, initially the changes could be very sharp until a new trend is established. Looking at the Trade-Weighted U.S. Dollar (Broad) Index in the chart below (where in January 1997 the Index equaled 100), we can see that the level on February 29, 2016 of around 124 for the greenback is at the upper end of the range since 1996, with the highest level having been at about 130 in 2002. The dollar has now surpassed the levels it held during the depths of the GFC in late 2008 and early 2009.

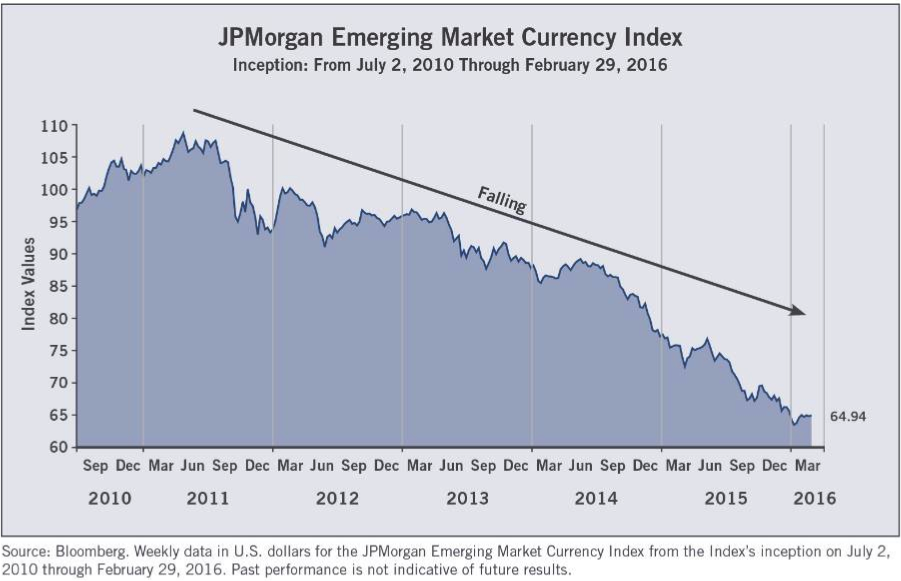

If we look at the JPMorgan Emerging Market Currency Index in the chart below, we can see that a basket of emerging-market currencies started falling against the U.S. dollar in 2011 — for a total decline of about 40%. So the bear market in emerging-market currencies had remained in force for approximately five years.

With global growth slowing and geopolitical risks rising, the attraction of the greenback as a safe-haven currency went up in the last several years. More recently, that safe-haven position was enhanced by the U.S. Fed signaling continued interest-rate increases and the Chinese government threatening to devalue the yuan. Conversely, commodity-oriented currencies such as the Australian dollar and the Canadian dollar lost their safe-haven status — along with declines in emerging-market currencies, many (although not all) of which are commodity-dependent. So we conclude that weak commodity prices further encouraged the movement of capital to U.S. dollar-denominated assets.

All in all, the U.S. dollar was in a powerful upward trend for the last several years, backed by some significant convergent forces. Likewise, the perennially steadfast Swiss franc was especially strong — to the point that market forces (rather than central bankers) even drove longer-term interest rates to negative levels, a situation we hope won’t occur in the United States.

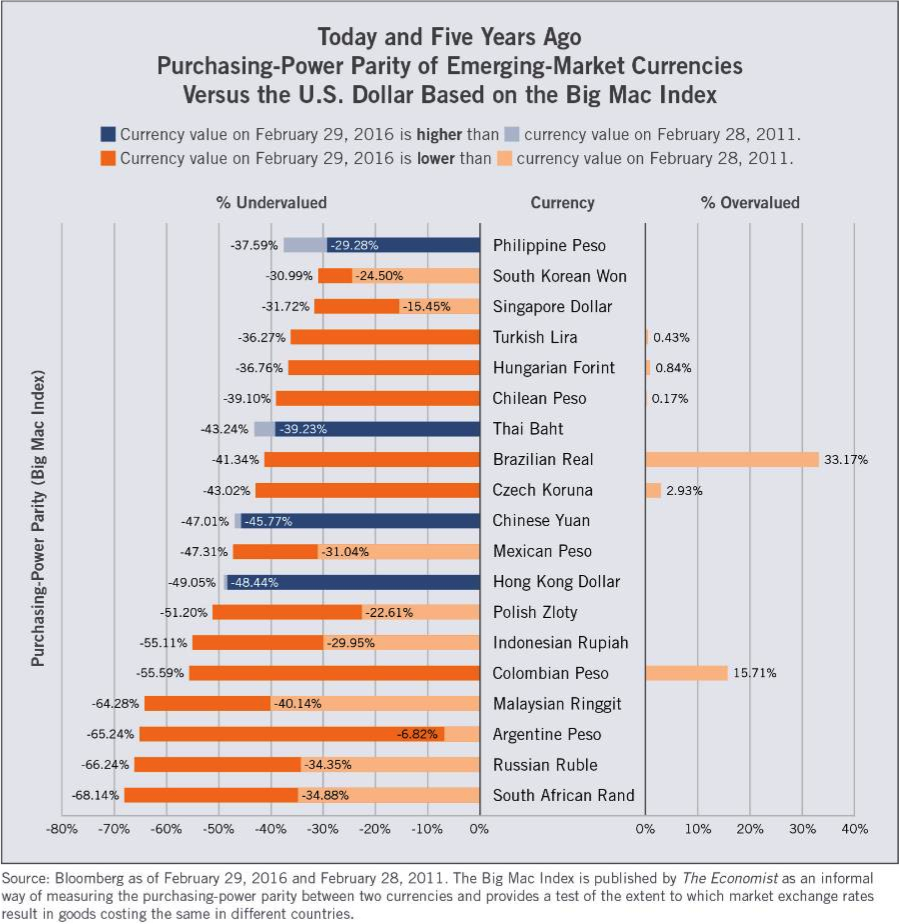

Resulting from the conditions described in this paper, many emerging-market stocks, bonds and currencies are now undervalued in our view. Regarding currencies, the “Big Mac Index” is a measure popularized by the The Economist to show the relative overvaluation or undervaluation of various currencies based on the concept of purchasing-power parity. The Index uses a consistent mix of goods and services (in this case, those involved in producing a McDonald’s hamburger) and current currency exchange rates to determine the “correct” level. By this measure, the chart below shows the extent to which various emerging-market currencies are “undervalued” relative to the U.S. dollar.

It’s important to note that the exact level of overvaluation or undervaluation on a purchasing-power parity basis is not the main point. (Emerging-market currencies will almost always appear undervalued relative to the U.S. dollar.) The important point is the degree of change from five years ago.

The dark bars in the chart show the currency valuations today (February 29, 2016). The light bars show the currency valuations five years ago (February 28, 2011). Orange indicates currencies that have fallen in value during the five years. And blue indicates currencies that have risen in value.

There are several conclusions to draw from this chart. First, most emerging-market currencies have fallen during the past five years. For example, the Brazilian real has gone from 33.17% overvalued to -41.34% undervalued, for a total drop of -74.51% during the five years! Even the Mexican peso has gone from -31.04% undervalued to -47.31% undervalued, for a total drop of -16.27%. Now you can see why investments in these countries could perform very well if the currencies readjust to levels closer to five years ago — regardless of whether the underlying stock or bond prices move at all.

So why do we think most emerging-market currencies will initiate a sustainable reversal in the near future? Quite simply, when currencies deviate from fair value, they eventually tend to come back into line. We believe signs of stabilization in commodities and more-attractive yields in emerging markets have shifted the momentum in favor of emerging-market currencies. Additionally, the U.S. Fed has backed off its rhetoric regarding interest-rate increases. That’s another reason to expect weakness in the dollar, with corresponding strength in emerging-market currencies.

The exceptions to our optimistic currency outlook, of course, are the currencies in blue. These currencies have risen during the five years. Look at the Chinese yuan and the Hong Kong dollar. It makes sense that these currencies are fairly close to where they were five years ago because they’ve mostly been pegged to the U.S. dollar. We think that will change going forward, which means the Chinese yuan and the Hong Kong dollar may devalue — hence our less optimistic view on Chinese and Hong Kong stocks as described earlier.

We could also make the case that the Philippine peso and the Thai baht have strengthened and are therefore not attractive at current levels. But for these currencies, we think the relative strength has to do with the fact that the Philippines and Thailand were not caught up in the commodities rout. And we actually like certain Philippine and Thai stocks without having a specific view on these currencies.

The Road Ahead: Emerging Markets Decouple and the Opportunity Set Narrows

In this paper, we’ve described why emerging-market stocks have generally performed poorly over the last five years — particularly for U.S. dollar-based investors. We’ve also explained why selectively chosen emerging-market businesses are now attractive in our view. Just as important, we’ve outlined the catalysts that could lead to sustainable advances in certain emerging-market stocks.

While China is still a large component of most emerging-market indices, we think it’s likely that we’ll continue to see a decoupling of China’s stock-market performance from the rest of the emerging-market universe and from the rest of the world in general. We may even see the creation of more emerging-market indices that specifically exclude China, just like there are Asian indices that exclude Japan. Such changes don’t mean China’s economy will disintegrate. They simply mean China will be perceived as having less of an impact on world markets.

Meanwhile, countries like India — whose GDP growth is now faster than China’s — will increase in prominence. In this regard, it’s interesting to note that China and India have very different economies. These two countries aren’t major trading partners with each other. Their businesses don’t compete heavily with one another around the globe. China has a bloated infrastructure along with corporate and government debt that must be digested, while India is poised to build its infrastructure for the future. And the Chinese and Indian stock markets aren’t highly correlated.

In addition to the decoupling from China, we think decoupling will take other forms. For example, emerging markets will cease to be defined as the “BRICS” (Brazil, Russia, India, China and South Africa). Oil- and other commodity-exporting countries will no longer be considered synonymous with emerging markets. Moreover, large state-owned enterprises (SOEs) will become less-dominant recipients of investor capital.

Along with the decoupling from outmoded perceptions, we believe the “new reality” is that the opportunity set for truly great emerging-market investments has narrowed. In particular, this opportunity set includes high-quality growth companies in the fields of Internet technologies, health care, business-process innovation, and products and services for the expanding middle-class consumer segments in emerging markets.

As we’ve already mentioned, the most-fertile ground for these companies are in places where capital is being allocated better — places like India, Indonesia, Mexico, the Philippines, South Korea, Taiwan and Thailand. While these countries, along with a few others, may seem to form a relatively small subset of the emerging-market universe, they give us plenty of investments to choose from as we strive to build high-quality, well-diversified portfolios.

Another part of the new reality is that a passive investment approach using index funds may not be ideal. Index funds haven’t effectively disaggregated the emerging-market category. They still reflect old perceptions regarding countries, industries and corporate governance (e.g., poor shareholder accountability among SOEs). Unlike actively managed portfolios, index funds also miss out on the boots-on-the-ground research that’s so essential in lesser-known areas of emerging markets, particularly for small-cap stocks.

In our view, the Wasatch emerging-market equity portfolios are currently positioned for the decoupling and more-narrow opportunity set described above. Many of the companies in which we’re invested also pay significant dividends. And for U.S. dollar-based investors, we think there’s strong potential for appreciation as the dollar weakens and emerging-market currencies generally strengthen. Based on these factors, we’re hoping for a “triple play” in emerging markets: 1) rising stock prices, 2) steady dividend yields, and 3) added boosts from currency adjustments. As of this writing, we’ve started to see improvement on all three fronts.

--

RISKS AND DISCLOSURES

In addition to the risks of investing in foreign securities in general, the risks of investing in the securities of companies domiciled in frontier and emerging-market countries include increased political or social instability, economies based on only a few industries, unstable currencies, runaway inflation, highly volatile securities markets, unpredictable shifts in policies relating to foreign investments, lack of protection for investors against parties that fail to complete transactions, and the potential for government seizure of assets or nationalization of companies.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read it carefully before investing.

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

CFA® is a trademark owned by CFA Institute.

ALPS Distributors, Inc. is not affiliated with Wasatch Advisors.

DEFINITIONS

A bear market is generally defined as a drop of 20% or more in asset prices over at least a two-month period.

The Big Mac Index is published by The Economist as an informal way of measuring the purchasing-power parity (PPP) between two currencies and provides a test of the extent to which market exchange rates result in goods costing the same in different countries. It “seeks to make exchange-rate theory a bit more digestible.” The index takes its name from the Big Mac, a hamburger sold at McDonald’s restaurants.

The “cloud” is the Internet. Cloud-computing is a model for delivering information technology services in which resources are retrieved from the Internet through web-based tools and applications, rather than from a direct connection to a server.

Devaluation is the planned or market-forced reduction in the value of a currency’s exchange value. Devaluation may improve a country’s balance-of-payments situation by boosting exports and reducing imports.

Dividend yield is a company’s annual dividend payments divided by its market capitalization, or the dividend per share divided by the price per share. For example, a company whose stock sells for $30 per share that pays an annual dividend of $3 per share has a dividend yield of 10%.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year.

The financial crisis of 2007-09, also known as the Global Financial Crisis (GFC) and 2008 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

The JPMorgan Emerging Market Currency Index measures the strength of the most traded developing country currencies against the U.S. dollar.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index designed to measure the equity market performance of emerging markets. You cannot invest in this or any index.

The MSCI World Index captures large and mid-cap representation across 23 developed market countries.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

OPEC is an acronym for the Organization of Petroleum Exporting Countries. OPEC was founded in 1960. It is a collective of countries that export large amounts of petroleum and was formed to establish oil-exporting policies and set prices.

The price-to-book value ratio is used to compare a company’s book value to its current market price. Book value is the value of a security or asset entered in a company’s books.

The price-to-cash flow ratio is a measure of investors’ expectations of a firm’s future financial health. Because this measure deals with cash flow, the effects of depreciation and other non-cash factors are removed. Similar to the price-to-earnings ratio, this measure provides an indication of relative value.

The price-to-earnings (P/E) ratio is the price of a stock divided by its earnings per share.

Purchasing-power parity (PPP) is an economic theory that estimates the amount of adjustment needed on the exchange rate between countries in order for the exchange to be equivalent to each currency’s purchasing power. Two currencies are in PPP when a market basket of goods (taking into account the exchange rate) is priced the same in both countries.

A sovereign wealth fund (SWF) is a state-owned investment fund investing in real and financial assets such as stocks, bonds, real estate, precious metals, or in alternative investments such as private equity funds or hedge funds. Sovereign wealth funds invest globally.

The Trade-Weighted U.S. Dollar Index, also known as the Broad Index, is a measure of the value of the United States dollar relative to other world currencies. The Index was introduced by the U.S. Federal Reserve Board in 1998 in response to the implementation of the euro. The Federal Reserve selected 26 currencies to use in the Broad Index. When the Index was introduced, U.S. trade with the 26 represented economies accounted for over 90% of total U.S. imports and exports.

Valuation is the process of determining the current worth of an asset, company or currency.

© 2016 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc.

WAS004083 4/30/2017