It’s an age-old adage: buy low and sell high. This mantra is typically seen as a recipe for success in stock market investing, particularly among value investors. In order to determine whether or not a stock is cheap, many value investors use fundamental ratios, such as price-earnings, price-to-book and price-to-sales. Low multiples are taken as an opportunity to buy, while high multiples are seen as an opportunity to sell. Following this line of reasoning, value investors typically shy away from stocks that appear expensive based on valuation ratios, and are drawn to stocks that appear cheap.

The low volatility anomaly

But there is more to valuations than meets the eye, and prevailing market conditions can have significant influence in pricing stocks with certain characteristics. A case in point is low volatility stocks. The “low volatility anomaly” states that stocks with lower volatility tend to outperform stocks with higher volatility. This behavior is an anomaly because it is not supposed to occur. Instead, investors are expected to earn returns consistent with the amount of risk taken — the greater the risk, the greater the return. Of course, low volatility cannot be assured.

Yet, in the case of low volatility stocks, research shows that excess returns have been driven more by the macroeconomic environment than by security valuations. Valuations may even provide the wrong signal to investors.

Low volatility performance during different market cycles

To illustrate how low volatility stocks have performed during different market cycles, I examined the PowerShares Low Volatility Portfolio (SPLV), which is based on the S&P 500 Low Volatility Index — a widely used benchmark of low volatility stock performance. The fund contains the 100 stocks in the S&P 500 Index with the lowest realized volatility over the preceding year at the time of reconstitution and rebalance.

SPLV will be five years old in May, and has experienced four interest rate cycles over its lifetime — two up and two down. Over the course of these cycles, low volatility stocks have outperformed when Treasury yields are falling, economic growth is slow and market volatility is high and rising.

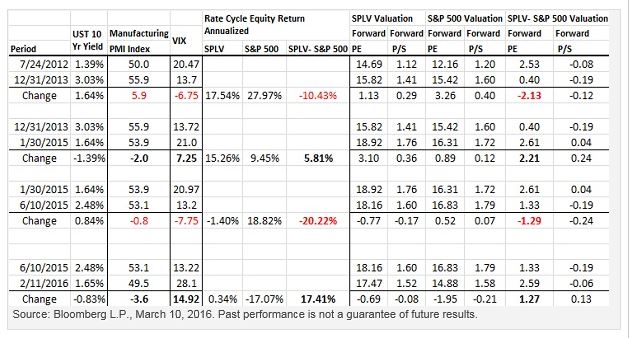

The following table highlights the cycles. The left side of the table reflects the macro environment, as measured by the Manufacturing PMI Index (manufacturing activity), VIX (market volatility) and 10-year Treasury yields (interest rates). The change in the 10-year Treasury yield from trough to peak and peak to trough is provided. The corresponding change in the ISM Manufacturing Index and VIX are also included. On the right side of the table is the expected price-earnings (P/E) ratio. SPLV’s standardized performance can be found here.

This table provides a number of insights:

- SPLV has outperformed the S&P 500 Index when there is an adverse investment environment, as represented by a declining 10-year Treasury yield, a declining ISM Manufacturing Index and rising market volatility (VIX). These conditions were evident from December 2013 to January 2015 and June 2015 to February 2016, when SPLV’s P/E and price-to-sales ratios increased.

- SPLV has lagged the S&P 500 Index in favorable investment environments, as represented by a rising 10-year Treasury yield, a rising ISM Manufacturing Index and falling VIX. This was seen in the July 2012 to December 2013 and January 2015 to June 2015 periods, when SPLV’s P/E and price-to-sales ratios declined.

- P/E and price-to-sales ratios have tended to rise during much of SPLV’s existence. The upward trend in valuations did not seem to change the reaction to macroeconomic conditions.

What conclusions can we draw from these trends?

Since low volatility investors aren’t compensated for assuming risk, valuations may not play a traditional role in determining performance. Moreover, low volatility stocks have the potential for downside risk mitigation and partial upside participation. That means that stocks with low volatility shouldn’t fall as hard or rise as fast as stocks with high volatility. As a result, the attractiveness of low volatility stocks may rise in bear market conditions and fall in bull market conditions, with less dependence on valuations than investors might expect.

Learn more about the PowerShares S&P 500 Low Volatility Portfolio (SPLV).

Important information

Market returns are based on the midpoint of the bid/ask spread at 4 p.m. ET and do not represent the returns an investor would receive if shares were traded at other times. Performance data quoted represents past performance, which is not a guarantee of future results. Investment returns and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than performance data quoted. After-tax returns reflect the highest federal income tax rate but exclude state and local taxes. Fund performance reflects fee waivers, absent which performance data quoted would have been lower. After Tax Held and After Tax Sold are based on NAV. Returns less than one year are cumulative.

Price-to-book ratio is the market price of a stock divided by the book value per share.

Price-to-earnings (P/E) ratio, also called multiple, measures a stock’s valuation by dividing its share price by its earnings per share.

Price-to-sales ratio is a stock’s capitalization divided by its cash for the fiscal year.

The S&P 500® Low Volatility Index consists of the 100 stocks from the S&P 500® Index with the lowest realized volatility over the past 12 months. An investment cannot be made into an index.

The ISM Manufacturing Index, which is based on Institute of Supply Management surveys of more than 300 manufacturing firms, monitors employment, production inventories, new orders and supplier deliveries.

VIX® futures provide a pure play on implied volatility independent of the direction and level of stock prices and serve as a gauge of near-term market volatility.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The fund’s return may not match the return of the underlying index. The fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the fund.

Investments focused in a particular industry or sector, such as the industrials sector, are subject to greater risk and are more greatly impacted by market volatility than more diversified investments.

The fund is nondiversified and may experience greater volatility than a more diversified investment.

There is no assurance that the fund will provide low volatility.

S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (S&P), and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones). These trademarks have been licensed for use by S&P Dow Jones Indices LLC. S&P® and Standard & Poor’s® are trademarks of S&P, and Dow Jones® is a trademark of Dow Jones. These trademarks have been sublicensed for certain purposes by Invesco PowerShares Capital Management LLC (Invesco PowerShares). The index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Invesco PowerShares. The fund is not sponsored, endorsed, sold or promoted by S&P Dow Jones Indices LLC, Dow Jones, S&P or their respective affiliates, and neither S&P Dow Jones Indices LLC, Dow Jones, S&P nor their respective affiliates make any representation regarding the advisability of investing in such product(s).

Beta is a measure of risk representing how a security is expected to respond to general market movements. Smart beta represents an alternative and selection-index-based methodology that seeks to outperform a benchmark or reduce portfolio risk, or both. Smart beta funds may underperform cap-weighted benchmarks and increase portfolio risk.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus/summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the Fund, call 800 893 0903 or visit invescopowershares.com for the prospectus/summary prospectus.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Are valuations relevant to low volatility investors? by Invesco Blog