European banks’ contingent convertible (CoCo) junior subordinated Additional Tier 1 securities — the junior subordinated subset of the CoCo family — suffered a significant sell-off in January and February from which they have only partly recovered. However, Invesco Fixed Income believes the investment thesis for this asset class remains intact, especially following the European Central Bank’s (ECB) constructive actions announced on March 10.

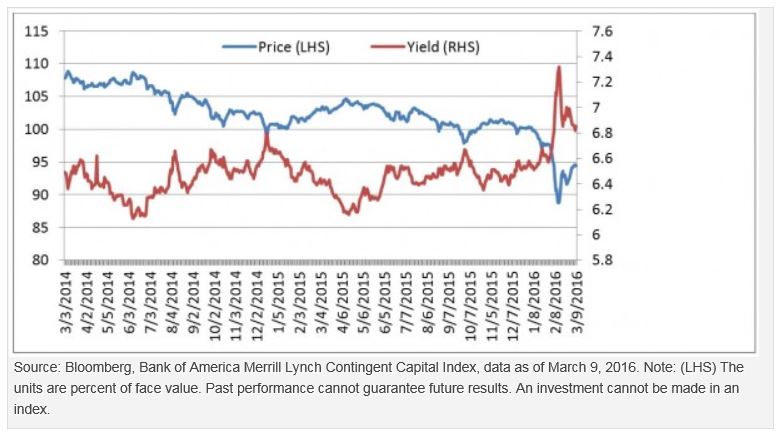

CoCos are up but still some way from their highs

Possible causes of the recent weakness in European bank assets include the restructuring of four small 2nd and 3rd tier Italian banks last year, the weak macro backdrop around the world (which led to fears of further declines in interest rates to negative territory), and the worry that the UK could vote to leave the European Union in a referendum.

However, we believe the fundamental balance sheet strength of European banks is at a multi-year high — with solid capitalization, liquidity and asset quality — with only some specific exceptions. While profitability has remained under pressure as a result of weak economic activity, most banks do remain profitable. Moreover, the equity market’s very positive reaction to the ECB’s March 10 announcement, which instituted new cheap financing lines for banks, suggests negative rate concerns have diminished. (Read more: ECB makes a bold move to boost growth.) At the same time, banks can do more to reduce costs and provisions.

European banks’ junior subordinated AT1 securities have a number of equity-like features that increase their riskiness. However, most if not all remain likely to be called at their call date — if not for economic reasons then to maintain the issuing bank’s reputation with fixed income investors whose support will continue to be required for future funding needs. Write-downs or conversion to equity is a vanishingly remote possibility due to the very high buffers to the relevant capitalization triggers. In most cases, issuers also boast reasonably high buffers above the coupon suspension triggers, and in any case regulators are thinking of allowing coupon payments to have priority over the usually much larger dividend payments, further supporting valuations.

The ECB’s announcement on March 10, which included a deposit rate cut but also measures to offer banks cheap ECB funding, caused equities and AT1 bonds to rally, the latter by about 2 points1 in price across the board. However, with the most solid Swedish, Swiss and Dutch names still yielding in the 6% to 7% range1, we believe there are still attractive investment opportunities.

1 Source: Bloomberg L.P., as of March 10, 2016

Important information

The Bank of America Merrill Lynch Contingent Capital (CoCo) Index tracks the performance of all contingent capital debt publicly issued in the major domestic and eurobond markets, including investment grade and sub-investment grade issues.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The value of convertible securities may be affected by market interest rates, the risk that the issuer will default, the value of the underlying stock or the right of the issuer to buy back the convertible securities.

AT1 means Additional Tier 1 securities, which are the junior subordinated subset of the CoCo bond family.

The common equity tier 1 ratio is a measure of capitalization using only equity, the purest form of capital that most easily absorbs losses.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Certain European bank CoCos still offer opportunities by Invesco Blog