The Collision of Aspiration and Reality in India

- The Collision of Aspiration and Reality in India

- Productivity Remains a Controversial Topic

As China falters somewhat, India has become the world’s new economic darling. Hopes of residents and global investors are lofty, but reality suggests a cautiously optimistic stance.

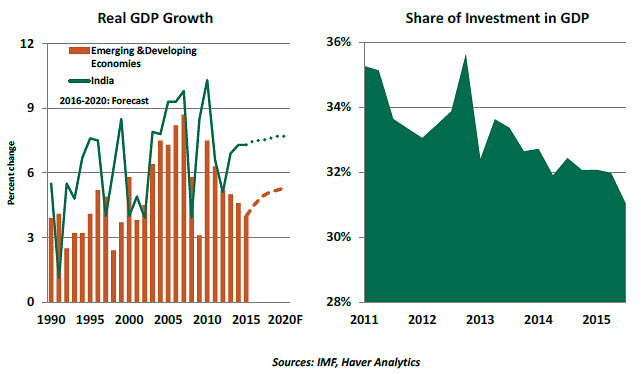

The recent economic profile of India paints an impressive picture. Real gross domestic product (GDP) of India advanced a little over 7% during 2014-2015, while the average momentum of emerging economies was lower. Favorable oil price trends have helped to bring down inflation in the last two years. India’s current account deficit is less than 2% of GDP, down from three years ago. The budget deficit was 4% of GDP in 2015, representing a gradual narrowing of the fiscal shortfall. India has a comfortable cushion of foreign exchange reserves in place.

India is member of the BRIC (Brazil, Russia, India and China) club. Within this peer group, the Indian economy stands tall because there are no visible excesses or economic calamities threatening growth.

Brazil faces an economic recession and significant political discord; economic recovery is not on the horizon now. Economic weakness in Russia, partly fueled by the plunge in oil prices, is unlikely to improve soon. The Chinese economy is engaged in a tightrope walk, rebalancing the economy toward consumer spending and away from exports and investment, while also managing its foreign exchange reserves, currency and capital flows. Thus, the relative standing of India is economically favorable and enables analysts to adopt a sanguine view about India.

Looking ahead, the economy is projected to grow at a sustained pace of more than 7% in the next five years and exceed the average of emerging markets.

But there are risks and deficiencies germane to the India economy to consider. There are three factors that could trim economic growth in the near term. First, India remains vulnerable to capital outflows, which could be initiated by monetary policy tightening in the United States or disenchanted investors leaving as the government fails to keep its promises. The net result would be a depreciation of the rupee and its associated repercussions on inflation.

Second, a hard landing in China presents a risk to India’s economy, despite limited exposure. If such a scenario occurred, all emerging markets (including India) are likely to experience capital outflows. In addition, India’s trade linkages with economies that have strong ties with China would suffer and weigh on growth.

Third, India’s banking sector is in a vulnerable position. The public- and private-sector banks face a serious challenge from non-performing loans, with the former accounting for the large share of stressed assets. The new budget sets aside INR 250 billion for bank recapitalization, which some view as insufficient. The pace of credit growth has increased slightly in recent months, but the pickup follows a significant deceleration. The central bank is firm about banks cleaning up their balance sheets by March 2017. Within this context, it may be not be surprising to see only soft credit trends in the months ahead, which is another drag on growth.

Even if we assume that these risks are well-managed and India’s growth meets expectations, there are significant economic issues within India to keep in mind when assessing the country’s medium- to long-term prospects.

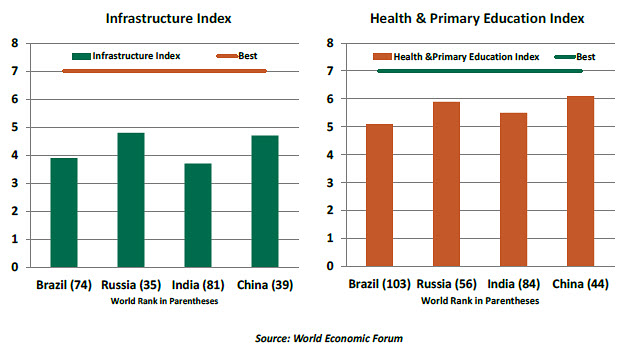

- From a broad perspective, infrastructure in India is woefully inadequate and a large part of what exists needs repair. The World Economic Forum’s Infrastructure Index indicates that India ranks 81st among 140 countries, far below most of its peers. The World Bank estimates India will need more than $1.5 trillion in infrastructure investment by the end of the decade.

The critical role of infrastructure in promoting growth and raising the quality of life is well-known. Until India catches up with better roads, electricity, water and the like, any plan to boost growth will have limited success. The fiscal year 2016 budget includes funding of the National Investment and Infrastructure Fund, which was initiated in last year’s budget. But it has yet to commence operations. The inertia of implementing plans and the large lack of infrastructure bode poorly for sustained strong growth. - The share of private-sector investment spending averaged around 35% of GDP during 2011-2012 and has since declined. A failure to lift investment implies a severe blow to realizing the potential capacity of the nation. Land acquisition in India to build new factories is a major difficulty due to antiquated laws. A new land acquisition bill is on the table, but actual reform is not expected soon.

- India’s population is greater than 1.2 billion, and the median age is 27. A healthy and educated workforce is necessary to ensure robust growth. India is struggling to meet this challenge. India ranks 84th out of 140 countries on the Health and Primary Education Index of the World Economic Forum. Reforms to improve health and primary education are imperative to lift the standard of living.

Frequently, analysts note that India’s pace of growth could surpass China’s in 2016. A word of caution is warranted here. Real GDP of India is around 26% that of China. Growth in China was maintained at a double-digit pace for nearly two decades. These numbers suggest that it will be a while before India is the next China.

The Paradox Thickens

Over the past several years, few topics have captivated the economic community more than productivity. Growth in the output that a given person can produce in a given time frame has slowed substantially over the past decade or so. The debate over why this has happened (or even if it has happened) has been deepened by some new publications.

Declining productivity is serious business, as it threatens improvements in standards of living, asset valuations and debt sustainability. So the search for a root cause of the recent decline, and a remedy for it, is very important.

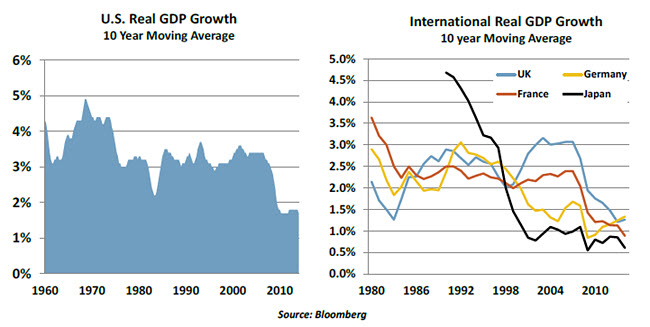

The broad evidence is shown below. Long-term economic growth began slowing in major developed economies about 10 years ago. The trend pre-dates the 2008 financial crisis, but has clearly accelerated since then. The charts show a 10-year moving average, which should remove most cyclical effects.

Explanations for this phenomenon fall into two camps. The darker of the two is the secular stagnation theory, which holds that an aging population combined with an absence of innovation has permanently lowered the potential of economies to grow. This point of view was summarized in “The Rise and Fall of American Growth,” by Robert Gordon of Northwestern University. Gordon has been an economic pessimist for some time; the book’s title evokes Edward Gibbon’s history of the Roman Empire, which ended in ruin.

Gordon’s economic analog is the American economic empire, which he sees as constrained by headwinds of demographics, debt, education and inequality. He argues that it requires significant amounts of job-creating, productivity-enhancing new innovation to compensate for these limitations. Sadly, according to Gordon, innovation is slowing and its benefits have largely been reaped.

Technology is a particular whipping post for Gordon. He tends to downplay the economic benefits of the Internet, and the multitasking devices that access it. In speeches, Gordon playfully asks audiences if they would be willing to give up indoor plumbing or their smart phones. (When I posed this choice to my teenager, she went out into the back yard and began digging a latrine.) For all of its flash, Gordon contends that the wired world adds little to productivity.

His opponents have contended that productivity gains are all around us, but are somehow being missed by our economic accounting systems. The potential mismeasurement of output has been cited as a potential reconciliation of the productivity paradox; economic activity is always difficult to gauge, but especially so in the technological realm. For example, Google’s search engine has value to users, but it is costless.

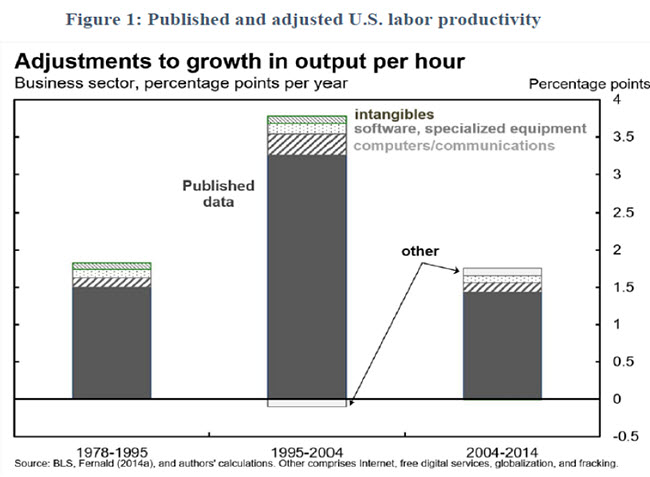

Two recent papers attempt to examine the mismeasurement issue rigorously. The first, from economists at the Federal Reserve and the International Monetary Fund, found that there is a potential undercount of output related to new technology. However, the discrepancy is small and has not grown over time.

The authors pointed out that many of the Internet services that we use are not entirely absent from the national accounts. Websites like Google are supported by advertising, so they are not strictly “free.” The value of advertising services is embedded in the prices of goods and services, which are accounted for in gross domestic product (GDP). And we pay (dearly, in some cases) for Internet service.

Much of the utility we derive from using our tablets and smartphones is “non-market,” meaning that it adds to our leisure value but not to GDP. Buying tickets to a concert counts towards national income, but using Instagram to post pictures of ourselves at the concert simply enhances the enjoyment we derive from the experience.

The second paper, from Chad Syverson of the University of Chicago, concurs with this conclusion. He estimates that U.S. GDP over the past 10 years would have been almost $3 trillion greater had productivity continued upward at its former pace. In his view, under-measurement of technology accounts for only a small fraction of this “missing output.”

Syverson finds that productivity has slumped in a number of countries, many of which are not nearly as reliant on the information and communications industry as the United States. He concludes that “the reasonable prima facie case for the mismeasurement hypothesis faces real hurdles when confronted with the data.”

While carefully done, these recent missives will probably not settle the issue. Some of the data still generate substantial disbelief; the measurement of real software output (which does count toward GDP when a household or business purchases it) does not appear to account properly for all of the additional capability and speed that today’s products provide.

Further, there are those (Martin Feldstein among them) who think that GDP is a very limited measure of economic progress. For example, the accounting process counts the price paid for a particular drug, but not the outcomes it produces.

Those of us who are more sanguine suggest that cyclical headwinds are the main reason for slow growth in output and productivity. The press of indebtedness pre-dates the crisis, and may have begun to curtail the trajectory of consumption and productive investment long before 2008. A lot of economic infrastructure is primarily the responsibility of the public sector, which has been forced into austerity at many levels because of past fiscal mismanagement. Without government investments in productivity, we cannot reap the returns.

In the private sector, incentives to invest would be a welcome part of any new Administration’s economic platform. Properly structured, these features would be accretive to GDP in the long run and therefore budget-neutral.

Of course, it is a fair point to ask how long cyclical headwinds have to go on before being considered secular. While some progress has been made in repairing balance sheets around the world, much remains to be done. It could be a long while before we see the conditions of the mid-2000s again.

Developed economies clearly need to do more to ensure that productivity grows acceptably. But the notion that growth as we know it has come to an end seems like an extreme conclusion.

(c) Nothern Trust