I. Introduction

Value investing as an investment strategy has existed for at least 100 years, and likely for centuries (if not millennia). At its core, value investing is a fairly straightforward strategy: Investors seek to buy an asset when its price is perceived to be “cheap” relative to measures of fundamental value.

A magnitude of research over the past few decades points out that a strong “value premium” has existed over time.1 In other words, stocks that are “cheap”—in terms of some measure of fundamental value such as price-to-book ratio—have outperformed “expensive” stocks. Is this always the case? No, there have been many periods where expensive stocks keep getting more expensive and cheap stocks get cheaper. But over time, the value premium is meaningful,2 particularly in the small cap segment.

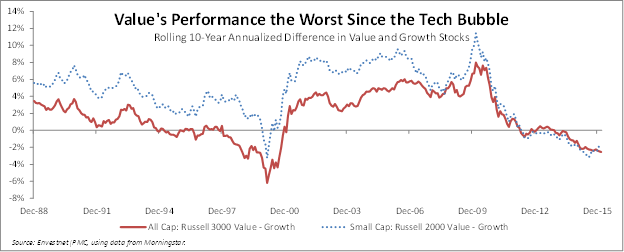

Yet we are currently in the midst of one of those periods where the performance of value is ebbing. Value stocks underperformed growth stocks by more than 900 basis points in 2015.3 As of January 31, 2016, value stocks have underperformed growth stocks by about 250 basis points annually over the past 10 years, the worst relative performance since the tech bubble in the late 1990s.

Given the poor performance in recent quarters of value investing as a strategy (at least relative to growth investing), some investors are questioning the efficacy of the approach. The concern over value has certainly not reached the fever pitch of 1999 at the peak of the tech bubble when headlines such as “Is Value Investing Dead?” were commonplace.4 However, given the rise of “smart beta” and other quantitatively driven products, it is fair to at least question whether the large value premium exhibited historically can continue going forward. Is this recent drought evidence that the value premium is being arbitraged away now that it is so well known, or that investing has somehow intrinsically changed so that fundamentally expensive stocks will now outperform cheap stocks?

Probably not. Value’s lackluster recent performance is likely part of the ebb and flow of the strategy, and value investing is still relevant, especially when used in concert with other approaches such as momentum.

II. The Evolution of Value Investing Strategies

Although the genesis of value investing as a framework is generally attributed to Benjamin Graham’s work beginning in the 1920s, investors have almost certainly been seeking values for, well, several millennia. In Old Testament times, Israelite patriarch Joseph was a shrewd value investor, buying up large swaths of land for Pharaoh during the famine from hungry and desperate Egyptians, and paying for it with the grain he had wisely accumulated during the years of plenty.

Some of the earliest data used in research on value investing dates from the 1860s.5 But the launching pad of modern day value investing arguably began with Graham and his Columbia University colleague, David Dodd, about 85 years ago.6 Graham and Dodd are well known for advocating an approach of buying stocks trading at discounts to their intrinsic value. Such opportunities are far scarcer today, but the Graham and Dodd philosophy has lived on, evidenced by a long line of wildly successful disciples, including Warren Buffett.7

Over the years since Graham and Dodd, two primary approaches to value investing have emerged: First, there is the fundamental approach in which the investor selects a stock based on an assessment of its valuation (often measured as the stock price relative to some financial statement component such as book value or earnings). Some fundamental value investors (especially in the hedge fund realm) will assemble a heavily concentrated portfolio which consists of only a handful of holdings, relying on their deep understanding of the companies in the portfolio.8 Others construct somewhat more diversified value portfolios, but the common thread between them is that they buy specific securities perceived to be cheap. The list of storied fundamental value investors is quite long, and in addition to Graham and Buffett includes, among many others, John Templeton and Marty Whitman.

The second primary approach increasingly being employed is what may be referred to as systematic, or diversified, value investing. The idea here is to capture the value premium generally across a broad group of stocks, and not necessarily through specific in-depth knowledge of individual companies.9 The purest form of capturing this premium is by going long cheap stocks and shorting expensive stocks. If operational or policy constraints limit shorting, simply going long (or overweighting) the cheap stocks can also add value. Investors employing this method tend to have a quantitative orientation, in part because of the amount of data that needs to be analyzed. Well-known investors employing this type of approach to value investing as part of their overall investment strategy include Dimensional Fund Advisors (whose investment strategies are largely based on the research of Eugene Fama and Kenneth French) and Cliff Asness and the team at AQR Capital Management. Many of the so-called “smart beta” exchange-traded funds are also simply systematic value investing strategies.

III. Performance of Value

Over the past 25 years or so, a massive amount of research shows that value investing (at least the systematic/diversified kind) has generated enviable returns. Just how large is the value premium historically? According to U.S. equity data from Kenneth French’s web site10, from the beginning of 1927 through January 2016, cheap stocks (those with high book value relative to market price, or “B/M”)11 have outperformed expensive stocks by almost 4% (400 basis points) on an annualized basis. One dollar invested on December 31, 1926 in a strategy of going long cheap stocks and shorting expensive stocks—often referred to as “HML”: High B/M Minus Low B/M—would have grown to more than $32 on January 31, 2016.

However, this does not mean that value is immune to years of negative returns, as approximately 40% of the calendar year returns since 1927 have been negative. Value can also go through fairly long stretches of underperformance. Since 1989, the HML strategy has suffered two prolonged periods of declines exceeding 20%: The first occurred during the tech craze—and eventual bubble—of the 1990s. The second has occurred over the past 10 years, a time marked by slow economic growth and aggressive monetary stimulus.12

Although the value premium can certainly disappear for longer than one would like, there is evidence that it is mean-reverting. In other words, value stocks eventually become so cheap relative to growth stocks that the performance of value rebounds, and often quite sharply. In a prescient article published in early 2000, Asness et al (2000) developed a model demonstrating that value’s performance is mean-reverting. Their paper concluded that in early 2000 the forecast one-year return spread of value relative to growth was near an historic high. Their forecast was exquisitely timed: as represented by the HML strategy, value outperformed growth by more than 75% (7500 basis points) over the subsequent three years.13

In the present environment, value is not treated with quite the disdain it faced in the late 1990s, but nevertheless it has severely underperformed growth for some time, particularly in the small cap segment. As has been the case during previous value bear markets, there are both risk-based and behavioral theories as to why value has performed so poorly. From a risk-based perspective, some theorists argue that the risk of value stocks relative to growth stocks has changed during this period. A common behavioral explanation is that investors have overpriced growth stocks in an irrational quest for sustainable earnings growth during a period of lackluster economic growth.

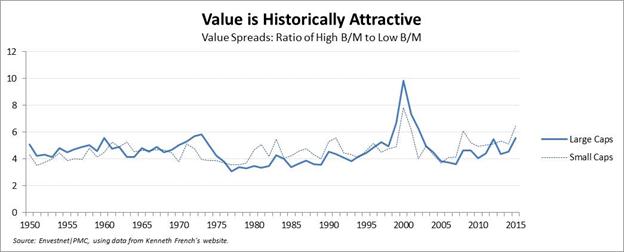

Whatever the reason, the underperformance of value has meant increasingly attractive valuations. The value spread is one measure of evaluating how cheap value has become. Kenneth French’s website provides historical ratios of summed book equity to summed market equity (BE/ME)—essentially aggregate B/M ratios—of both large and small companies. As in Asness (2015), the value spread for large caps can be calculated as the ratio of the BE/ME for the one-third of the stocks having the highest BE/ME ratios (cheap stocks) to the one-third of companies having the lowest BE/ME ratios (expensive stocks). The same approach can be followed for small caps. The nearby graph shows that while the large cap value spread is currently elevated (but not quite at historical highs), the small cap value spread is at the highest level since 1950, with the exception of the peak of the tech bubble in early 2000.

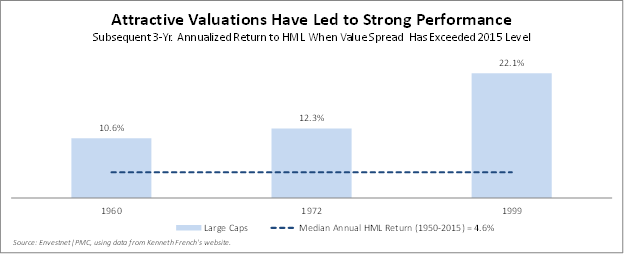

As value spreads have widened considerably, does that mean that value strategies will perform well on a relative basis going forward? Quite possibly, if history is a guide. Since 1950, there have been just three times when the value spread for large caps has exceeded its 2015 level, the latest year for which data is available. The three years following each of those periods have generated very strong annualized returns to the HML strategy, in each case far exceeding HML’s median annual return of 4.6% from 1950 to 2015.14

IV. Conclusion

Investing in value stocks has generated a long track record of superior performance relative to a strategy of investing in growth stocks. However, the value premium is not a constant, as value has encountered lengthy periods of underperformance. We are presently in the midst of one such value “drought,” but these periods of underperformance are usually accompanied by increasingly attractive valuations. One measure of this attractiveness is the value spread, which is currently at historically high levels, especially for small cap stocks. If past is prologue, it is quite possible that value will perform very well relative to growth going forward.

References

Asness, Clifford S., “How Can a Strategy Still Work If Everyone Knows About It?” AQR Capital Management website, August 31, 2015.

Asness, Clifford S., Jacques A. Friedman, Robert J. Krail, and John M. Liew, “Style Timing: Value versus Growth,” Journal of Portfolio Management, vol. 26, no. 3 (Spring 2000).

Chabot, B,, E. Ghysels, and R. Jagannathan, “Momentum Trading, Return Chasing, and Predictable Crashes.” Working paper, The Federal Reserve Bank of Chicago, November 2014.

DeBondt, Werner F.M. and Richard Thaler, “Does the Stock Market Overreact?” The Journal of Finance 40(3), 793–805, 1985.

Fama, Eugene F., and Kenneth R. French, “The Cross-Section of Expected Stock Returns,” The Journal of Finance 47(2) 427–465, 1992.

Fama, Eugene F., and Kenneth R. French, “Common Risk Factors in the Returns on Stocks and Bonds,” Journal of Financial Economics 33(1) 3–56, 1993.

Harvey, Campbell R., Tan Liu, and Heqing Zhu, “…and the Cross-Section of Expected Returns,” NBER Working Paper No. 20592, 2014.

Lakonishok, Josef, Andrei Shleifer and Robert W. Vishny, “Contrarian Investment, Extrapolation and Risk,” The Journal of Finance 49(5), 1541–1578, 1994.

Zhang, Lu, “The Value Premium,” The Journal of Finance 60(1), 67–103, 2005.

We changed our name—and our email address. JCPR is now JConnelly. Please make sure you update your address book so we can stay in touch. Visit jconnelly.com to learn more.

1 Research on the value premium extends back more than 30 years. DeBondt and Thaler (1985) were among the first to associate the outperformance of value stocks with investor behavior. In widely cited papers, Fama and French (1992) and (1993) find a value premium, but hold that it is a risk factor, and not a behavioral phenomenon.

2 In their evaluation of hundreds of factors impacting the cross-section of expected stock returns researchers have identified over the years, Harvey, Liu and Zhu (2014) found that value is among the most statistically significant.

3 Value and Growth stocks are represented by the Russell 3000 Value and Russell 3000 Growth indices, respectively. According to Morningstar, the Russell 3000 Value Index declined -4.13% while the Russell 3000 Growth Index advanced +5.09%.

4 Several articles from 1999 and early 2000 questioned the viability of value investing. For example: https://assetbuilder.com/knowledge-center/articles/is-value-investing-dead; http://www.valuewalk.com/wp-content/uploads/2013/01/Pzena-Investment-Management-The-Search-For-Value.pdf;

5 Chabot, Ghysels, and Jagannathan (2014).

6 Graham and Dodd taught finance at Columbia University, and together wrote the seminal Security Analysis. Graham also wrote the highly regarded The Intelligent Investor.

7 Buffett was a student of Graham’s at Columbia. Other notable investors having employed a Graham and Dodd approach include William Ruane (Sequoia Fund); Walter J. Schloss; Irving Kahn; Charles Munger (Buffett’s colleague at Berkshire Hathaway); Michael Price (Mutual Series); Joel Greenblatt (Gotham Capital); Seth Klarman (Baupost Group); and many others.

8 Some fundamental value investors (often, but not exclusively, hedge funds) employ an “activist” approach, in that after identifying a company as being undervalued, they encourage management to take certain steps to unlock the company’s perceived value.

9 Academic research often refers to identifying value across a given universe of stocks as “cross-sectional” analysis.

10 http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/Data_Library/f-f_factors.html.

11 The B/M ratio is the inverse of the price-to-book (P/B) ratio.

12 Between March 31, 1989 and February 29, 2000 the HML strategy generated a cumulative return of -31.3%. Between March 31, 2007 and January 31, 2016, the HML strategy declined -23.5%.

13 The HML strategy generated a cumulative return of 77.3% from 1/1/2000 – 12/31/2000.

14 Small caps present a similar story, although there has been only one instance – 2000 - when the small cap value spread exceeded the 2015 level. The annualized return to HML for the subsequent three years was 11.2%.