KEY TAKEAWAYS

· Last year was difficult for European corporate earnings and stock market performance, with this year not appearing much better.

· Many “wildcards” may cause European equities to outperform low expectations, but at current valuations we do not believe investors are being properly compensated for the risks associated with the asset class.

Forecasts for European corporate earnings have become increasingly pessimistic. Analysts have reduced calendar year 2016 expectations to just under 3% earnings per share (EPS) growth, currently from nearly 20% as of the end of September 2015. Even though European stock prices have declined, the collapse in growth expectations suggests that these markets are still fairly valued; few, if any, bargains have been created. Recent aggressive monetary policy by the European Central Bank (ECB) may have boosted stock prices, but the implications for corporate earnings are much less certain. At just over 15 on a forward basis, the price-to-earnings ratio (PE) is well above the average since 2004 of 12.8 and does not present a great opportunity given the uncertainty around 2016 earnings expectations. Existing growth forecasts may be at risk due to political events, most notably the referendum on Britain’s continued membership in the European Union (EU). Central bank activity has created volatility in the currency markets, volatility for which U.S. dollar–based investors are not likely to be compensated. These factors lead us to be cautious on Europe at this time.

MORE THAN THE USUAL OPTIMISM

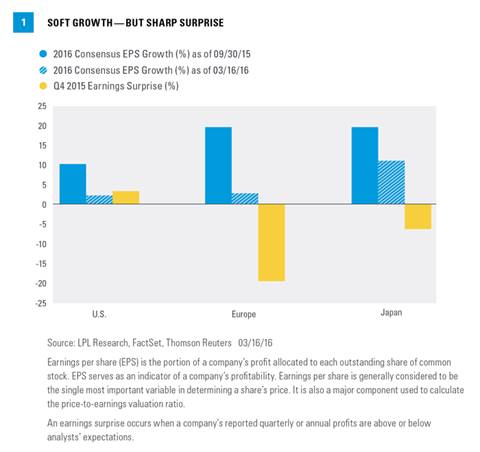

Investment analysts are typically overly optimistic when beginning to forecast earnings and earnings growth for a given time period. Analysts subsequently revise those forecasts downward. Forecasts for Europe in 2016 have dropped dramatically, from expectations of nearly 20% growth to now less than 3%. Though forecasts for other regions were revised down, the apparent reversal of opinion on Europe was much greater [Figure 1]. Financial analysts were very optimistic on both Japanese and European corporate earnings growth as recently as September 2015. Expectations for U.S. earnings growth were not as robust, so although they fell to about the same level, the drop is less dramatic. Despite continued loose monetary policy from their respective central banks, earnings forecasts fell, but much more for Europe than Japan or the U.S.

What happened? First, the fourth quarter was dreadful for European companies. The majority of companies (52.3%) missed the already lowered earnings expectations, while 58.2% of their U.S. peers outperformed expectations. Furthermore, the magnitude of the earnings miss in Europe was extreme at -19.5%, again contrasting to the positive 3.5% outperformance of U.S. companies relative to their fourth quarter expectations. After seeing the poor performance of so many European companies relative to expectations, analysts had to substantially reconsider future forecasts.

The macro backdrop for the region also gives the market little reason to believe that Europe can break out of its nearly five-year earnings recession. European earnings peaked in November 2011 and have fallen 16% since then. Gross domestic product (GDP) for the EU grew at 1.9% in 2015, and forecasts for 2016 are for 1.8%. These forecasts are at risk given the potential damage that could be caused should Britain decide to leave the EU. This is not the supportive backdrop European companies need for accelerated earnings growth.

IS THE STORY IN THE SECTORS?

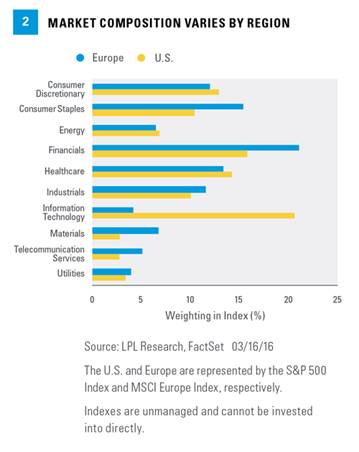

Given the dramatic decline in energy prices, it is not surprising that the subsequent earnings and price decline of energy stocks influences and perhaps distorts broader market metrics. In fact, 85% of the market capitalization of European energy stocks consists of the three major multinational integrated energy companies—those that extract, refine, and sell finished products such as gasoline and diesel. In the United States, less than half of the market capitalization consists of the top three companies, with many more pure exploration and production companies or service providers in the energy industry. Therefore, earnings forecasts for European energy stocks are highly reliant on a small number of very similar companies. Given the composition of the sector, we expect U.S. energy stocks to be more sensitive to underlying commodity prices.

Looking beyond energy, European materials, telecoms, and utilities sectors also saw earnings declines during the quarter. These three sectors comprise 15.8% of the MSCI Europe Index, compared to 9% of the S&P 500 Index. Collectively, these sectors tend to be lower growth. Figure 2 shows the relative sector weights for the U.S. and Europe. In particular, Europe provides investors with a greater exposure to materials stocks, including major mining companies where most of their production comes from Australia and Africa. These companies are highly sensitive to the Chinese slowdown. In fact, the companies in Europe that performed best relative to expectations in the fourth quarter of 2015 were those where most of their business was conducted within Europe. The companies that performed worst relative to expectations had the most exposure to emerging markets.

EUROPEAN FINANCIALS AND NEGATIVE INTEREST RATES

Another significant difference between the U.S. and Europe is that Europe has a much larger financial sector. Both current and expected earnings of financial stocks in Europe have been impaired by the negative interest rate environment in Europe. The ECB was so concerned about the impact of negative rates impacting banks that it announced a new Targeted Longer-Term Refinancing Operations provision (officially called the TLTRO II, suggesting that the ECB has run out of clever acronyms). This program will lend banks money interest free, and if that bank increases its lending over the next two years, the ECB will reward it with additional money. This program represents the ECB’s attempt to stimulate the economy, while improving the “business of banking,” and therefore, encouraging more lending. Regardless of any success over the life of the program, the nature of the program is not expected to have any impact on earnings until 2018.

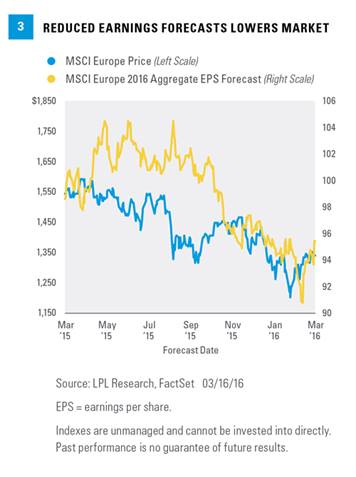

Despite negative returns for the MSCI Europe Index last year and a 5% decline this year, these markets are still not cheap. Prices for European equities declined fairly steadily last year and the first six weeks of 2016, as earnings forecasts were revised downward, consistent with the weakening earnings and economic backdrop. Stocks and growth forecasts have rebounded with energy prices more recently. But have they fallen enough to make Europe attractive, considering this background? Data suggest that they have not [Figure 3]. Forward valuations for the market suggest a PE of around 15x expected 2016 earnings. This is consistent (if not at a premium) with the longer-term average for the market.

CURRENCY MATTERS

Currency matters for European investments, but can have both positive and negative effects. The euro declined last year against all of Europe’s major trading partners, including the U.S., Japan, and China. This provided some boost to export-oriented companies, though clearly not enough to have a major impact on overall earnings. However, the declining euro also impairs returns for U.S.-based investors. Our expectation is for the dollar to be more stable this year.

The significant wildcard of the “Brexit” remains. Should Britain leave the EU, we would expect significant currency weakness versus the U.S. dollar and other currencies, almost certainly in the British pound, but also likely in the euro as well. In our view, given current equity market valuations, investors are not being rewarded for taking on the politically induced currency uncertainty.

CONCLUSION

European companies and equity markets’ performance has been a disappointment. The major underperformance of companies relative to expectations has made analysts pessimistic for this year as well, forecasting just 2.9% earnings growth for all of 2016. At this point, nothing in the political or economic environment is suggesting a significant reversal in this position; if anything, the political issues in Europe are adding uncertainty to the market. Given current valuations, we do not believe investors are being rewarded for this uncertainty. For the foreseeable future, we will remain cautious on the European market.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

International investing involves special risks, such as currency fluctuation and political instability, and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Because of its narrow focus, investing in a single sector, such as energy or manufacturing, will be subject to greater volatility than investing more broadly across many sectors and companies.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation; a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with a lower PE ratio.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Currency risk arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI Europe Index is a free float-adjusted, market capitalization-weighted index that is designed to measure the equity market performance of the developed markets in Europe.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.