Schwab Market Perspective: Sigh of Relief

Key Points

- Stocks, commodities, and beaten down sectors have staged an impressive rebound as fears of recession have abated. But that doesn’t mean the all clear signal has sounded, and volatility will likely stay elevated.

- The Federal Reserve held steady at its recent meeting, but kept future rate hikes in play. With a tight labor market, inflation rising, and financial markets calming down, we could see a couple of hikes still to come this year.

- The recent European Central Bank (ECB) and Bank of Japan (BoJ) meetings were relatively beneficial to their respective markets. There is some improvement in global growth but risks of a policy misstep remain and volatility should continue.

Whew!

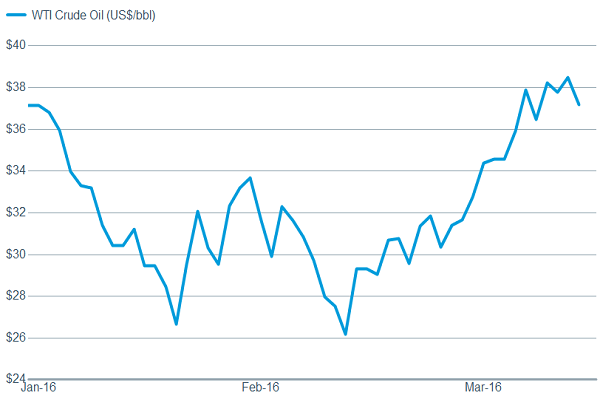

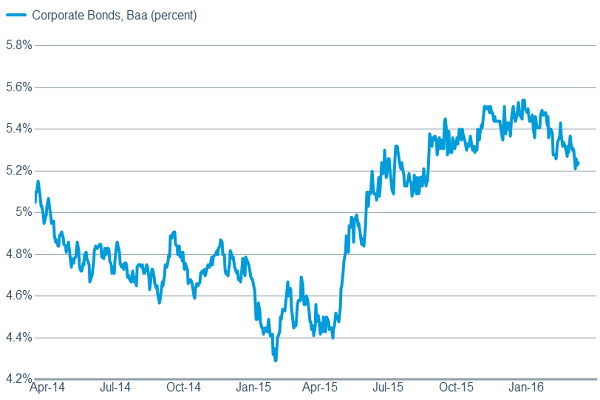

Beaten down areas of the market have staged a nice turnaround. Stocks have moved well off the lows and the S&P 500 is now within shouting distance of the flatline for the year. Areas of the market that were some of the hardest hit—such as materials, energy and financials—have posted some of the best gains over the past month. Other measures of risk aversion have also moved in a positive direction: Treasury yields have risen, meaning some money has moved out of the safe haven investment; commodities—including oil—have risen; and junk bond yields have fallen; all indicating an increasing appetite for risk among investors.

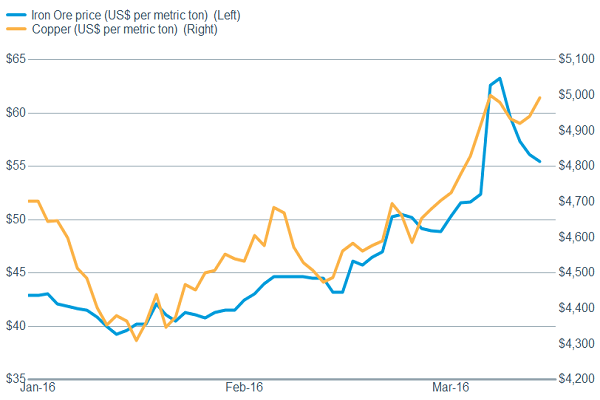

Commodities have bounced as recession fears have eased

Source: FactSet, Commodity Research Bureau. As of Mar. 15, 2016. China import Iron Ore 62% FE spot.

Source: FactSet, Dow Jones & Co. As of Mar. 15, 2016.

While measures of risk aversion have fallen

Source: FactSet, Federal Reserve. As of Mar. 15, 2016.

So is it clear sailing from here? Not exactly. While we’ve been of the opinion that stocks were overestimating the chances for a recession in the United States, headwinds remain. . From a contrarian sentiment perspective, investors don’t appear to be embracing this rally, as according to the Ned Davis Research Crowd Sentiment Poll investors have moved off of extreme negative sentiment, but are only now in neutral territory. We believe stocks can move modestly higher over the course of the year, but believe investors should be mindful of risks and not become greedy. Earnings will likely play a large part in market movements in the coming months after a couple of quarters of negative earnings growth, with investors looking for any increase in profits momentum.

Economy growing, but not booming

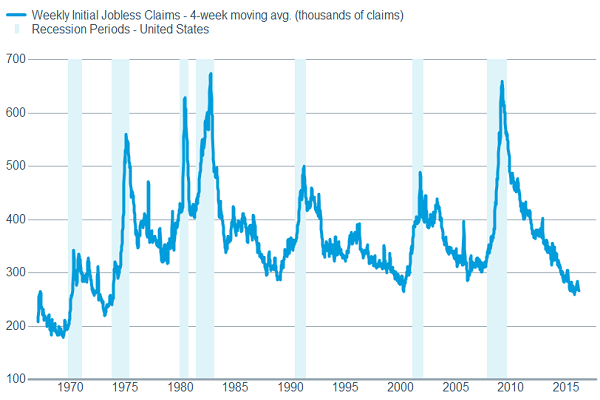

The earnings outlook will be greatly influenced by the economic outlook, which in our view remains relatively modest. It still appears to us that we’re in a 2-2.5% “real” (inflation-adjusted) gross domestic product (GDP) growth environment, so the muddle along characterization of the economy remains apt. The labor market continues to be the star of the economic picture, with unemployment at 4.9%, the labor force participation rate ticking up recently, and the sharp decline in forward-looking initial jobless claims indicating continued strength.

Claims remain quite healthy

Source: FactSet, U.S. Dept. of Labor. As of Mar. 15, 2016.

But manufacturing remains a weak spot. Although we have seen some improvement in various surveys, such as the Institute for Supply Management’s Manufacturing Index and the Empire Manufacturing Index in recent weeks, we’re still hovering around the expansion/contraction line. And somewhat concerning was the drop in the National Federation of Independent Business (NFIB) Optimism Index to the lowest level in about two years; however, the recent weakness in the stock market may have been a contributing factor.

Politics play a role, while the Fed maintains flexibility

Business confidence is important for the US economy to start to see accelerating growth. Businesses have hired to keep up with increasing demand, but capital spending has been decidedly lackluster. It appears that a lack of confidence in the future could be playing a role in the reluctance to make long-term capital commitments. In the same survey by NFIB referenced above, business owners said economic conditions and the political climate were their top two concerns. Nearly a quarter of small business owners said complying with government regulations was their biggest challenge over the past 12 months.

And we have a less-than inspiriting election season so far, which has likely contributed to market volatility and is not inspiring a lot of confidence among business owners. Bombastic statements from both sides of the aisle blasting trade and promising to restrict the movement of goods between countries through various measures doesn’t strike us as being conducive to improving economic growth.

The Federal Open Market Committee (FOMC) met and declined to make a move on rates, as was expected, but set the stage for potential hikes later in the year. Although the tenor has been dovish, in speeches before the meeting, several members noted that the labor market is tight and inflation is starting to pick up. Those comments, combined with the FOMC’s continued desire to normalize policy, leads us to believe two rate hikes in 2016 are possible, which is what the Fed’s projections also indicate.

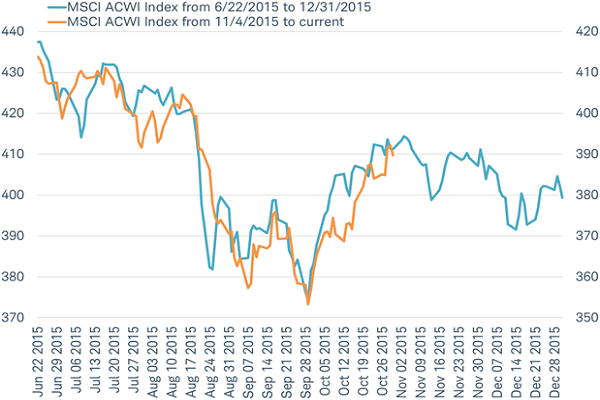

Global stock market rebound meets its first major test

The FOMC also continued to note global issues as being a concern. The rebound in the global stock market has repeated the pattern from last fall as it came up against its first major test—a series of major central bank meetings in Europe, Japan and the United States, all within a week of each other.

Déjà vu: Global stocks retrace pattern of last fall to critical juncture

Source: Charles Schwab, Bloomberg data as of 3/15/2016.

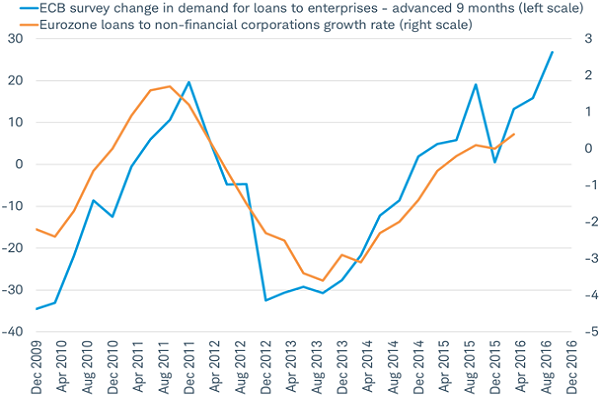

The ECB held the first of the series of major central bank meetings on March 10. Although the stock market’s initial reaction to the announcement was mixed, the Bloomberg, U.S., and European Financial Conditions Indexes improved, and European stocks moved higher over the following days, as measured by the MSCI Europe Index. The announcement included an increase in the quantitative easing (QE) bond buying program, and expanded the types of bonds purchased to include non-bank corporate bonds. In addition, to buffer the impact on bank profits of a further move into negative interest rate policy, banks that qualify will get paid to borrow from the ECB to make loans. Lending has been on the rise in the Eurozone, as you can see in the chart below. The new incentives may unlock more lending, a precursor to better economic growth.

European bank lending has been back on the rise

Source: Charles Schwab, Bloomberg data as of 3/15/2016.

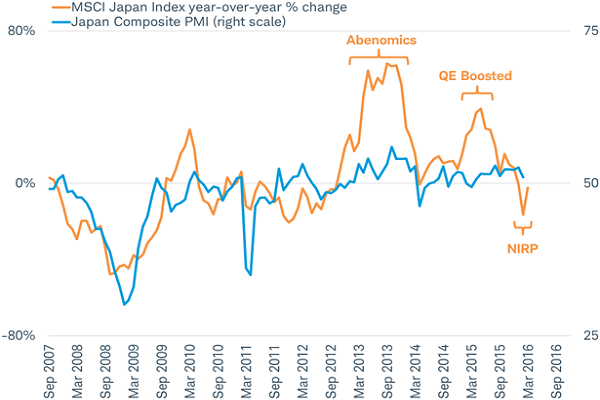

The BoJ held the second of the central bank meetings on March 15. Its actions backfired and resulted in a stronger yen and worsening financial conditions as financial stocks were pressured by the adoption of negative interest rate policy. Historically, stocks in Japan have tracked economic activity as measured by the Japan Composite Purchasing Managers Index (PMI); except during periods of exceptional policy changes, such as during the adoption of “Abenomics” or the expansion of Japan’s QE asset purchase program (see the chart below). The adoption in January of a negative interest rate policy (NIRP) led to stock market performance veering to the downside and away from the economic trend. As a result of the reaction to NIRP, at the March 15 meeting the BoJ left rates and its QE program unchanged; but made it clear to the market it may cut rates further into negative territory, if needed.

Negative interest rate policy led Japanese stocks to underperform the economy

Source: Charles Schwab, Bloomberg data as of 3/15/2016.

The current interdependence of the markets, central bank policy, and financial conditions define a key test for all. Central bank actions late last year and early in 2016 worsened financial conditions, led to deterioration in stock markets, and raised risk premiums across markets, effectively undermining policy objectives. The response by central banks in the form of a shift in focus away from currency depreciation versus the U.S. dollar, and toward restoring financial stability and lowering market risk premiums, supported the rebound. Central banks can help to sustain the recovery by calibrating their policies to allow for a more stable U.S. dollar versus emerging market currencies, and by limiting the impact of NIRP on the financial sector. This more favorable policy combined with the recovery in oil prices, better economic data, more stable capital flows from China, and an easing of geopolitical tensions in Syria may work to further lower global risk premiums and continue the rally, bucking the pattern of last fall. The initial outcome of the central bank meetings is encouraging, but policy missteps could still cause conditions to deteriorate again and result in a renewed decline for stocks. Investors should remain globally diversified as heightened volatility is likely to continue.

So what?

We’ve seen a nice rebound in stocks off the lows but we don’t believe the market can sustain the pace of gains seen over the past month. Economic growth remains sluggish, earnings growth has been weak, and monetary, political and regulatory uncertainty is elevated. We think U.S. stocks continue to experience bouts of volatility but that a growing economy and a healthy U.S. consumer will contribute to equities ultimately moving higher. Overseas central banks seem to have corrected some of their mistakes from earlier meetings, fostering a rebound in global equities. Risks still remain of course, but there are glimmers of improvement, and investors should remain globally diversified.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification strategies do not ensure a profit and cannot protect against losses in a declining market.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The Empire Manufacturing State Index is a regional, seasonally-adjusted index published by the Federal Reserve Bank of New York distributed to roughly 175 manufacturing executives and asks questions intended to gauge business conditions for New York manufacturers.

The Institute for Supply Management (ISM) ManufacturingIndex is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

NFIB - Single Most Important Problem: question posed in the NFIB (National Federation of Independent Business) Small Business Optimism Survey which is based on the responses of 740 randomly sampled small businesses in NFIB’s membership, surveyed monthly.

MSCI ACWI (All Country World Index) is A market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets.

The Markit Japan PMI Composite Index tracks business trends across both the manufacturing and service sectors, based on data collected from a representative panel of companies from the manufacturing and services sector. The index tracks variables such as sales, new orders, employment, inventories and prices.

The MSCI Europe Index captures large and mid cap representation across 15 Developed countries in Europe. With 448 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The Bloomberg Eurozone Financial Conditions Index is an overall gauge of the health of the financial and credit markets.

The MSCI Japan Index is designed to measure the performance of the large and mid cap segments of the Japanese market. With 318 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0316-DU32)