Key Takeaways

- Employment gains and upward pressure on wages remain the centerpiece of the FOMC’s rate-hike strategy.

- Fed Chair Janet Yellen made it clear that the FOMC is not considering a negative-interest-rate policy.

- Investors should pay attention to measures of actual or expected inflation in order to anticipate the Fed’s rate-hike timetable.

- Inflation-sensitive sectors such as materials, financials and TIPS could be early beneficiaries of rising inflation.

- How quickly and strongly the Fed reacts to higher inflation rates will be critical to equity-market performance this year.

FOMC takes a more dovish tone

Official statements following the US Federal Reserve’s two-day meeting made headlines even though the Federal Open Market Committee, the 17-member policy-making group, did not adjust the stance of monetary policy.

As usual, analyses of the decision to put further rate increases on hold focused overwhelmingly on the so-called “dot plot,” the chart showing the appropriate path (according to each of the 17 FOMC members) for the target federal funds rate through 2018. The pricing at work in money and fixed-income markets over the last several weeks suggested that investors anticipated that FOMC members would favor a slower pace of rate increases. And that’s what they got.

Slight, but meaningful, downward adjustments to committee members’ December 2015 forecasts for real economic growth underpinned the dot-plot revisions. For example, the FOMC member with the median forecast expects a real GDP growth rate of 2.2% (measured in the fourth quarter of 2016 vs. the fourth quarter of 2015), down from 2.4%; and 2.1% growth in 2017 versus the 2.2% forecast three months ago. The same forecast leaves unchanged at 2.0% the median estimate of longer-run US potential growth. A less-positive economic forecast could help the FOMC fend off potential pressure to increase monetary accommodation again if real economic growth this year generates a negative surprise.

FOMC members, on average, did reduce their estimate for the year-end unemployment rate in both 2017 and 2018, to 4.7% and 4.6%, respectively, and they nudged down their longer-run estimates of the natural rate of unemployment, to 4.8% from 4.9% in December. Persistent labor-market strengthening and the expected upward pressure it puts on wage rates remain the centerpiece of the FOMC’s overall economic forecast and rate-hike strategy.

In a similar vein, committee members, on average, cut their forecast of headline inflation (as measured by the PCE deflator) in 2016, apparently to reflect the impacts of weak commodity, energy and import prices. A bit surprisingly, however, the committee left unchanged its estimate of core inflation (which strips out the prices of food and energy) in 2016, at 1.6%. Actual core inflation, measured by the year-over-year rise in the PCE deflator, already is up 1.7%. For 2017, the committee, on average, also lowered its inflation estimate by 0.1% to 1.8%, just 0.1 percentage points above its current level.

Official statements reveal plenty that’s new

Perhaps the most critical longer-run outcome of yesterday’s FOMC announcements derives from the increased clarity they bring regarding the issues of greatest concern to the committee. These concerns focus around sustaining real economic growth, persistent weakness in core inflation, international influences on the US economy and financial markets, and the uncertain balance of risks. Let’s examine each of these concerns:

1. How to sustain real economic growth

The official FOMC statements delivered yesterday, as well as those of individual committee members, suggest that the committee may fear that increasing the policy interest rates too rapidly or too steeply could contribute to a premature downturn in overall economic activity. By opening the official post-meeting press release with a generally favorable, though mixed, picture of current US economic conditions, the committee put this concern ahead of all others. Such positioning is consistent with recent speeches by several Reserve Bank presidents and least one governor, which alluded to tentative signs of slowing US real economic growth. With the economy growing only “moderately,” the committee apparently does not want to confront accusations that its goal of raising the federal funds rate to its neutral, or more normal, level can throw the economy into recession.

2. Why core inflation is persistently weak

Embedded deep in the core of monetary-policy thinking is the tenet that when inflation is low, and inflation expectations have fallen, interest rates should not be increased. And this FOMC appears unwilling to go against that tenet. While recent core inflation data reveal that prices may be stirring, no conclusive evidence of a sustained upswing in inflation across multiple sectors and regions can yet be discerned. Thus, the latest press release, like so many of its predecessors, emphasizes that actual inflation and market-based expectations of inflationary expectations remain stubbornly low.

3. How international developments affect the US economy

International considerations are playing an increasingly larger role in the formulation of US monetary policy. Indeed, the committee’s official statement opens up with two references to international economic and financial influences on the US economy. The statement’s first sentence says that domestic US growth expanded “at a moderate pace despite the global economic and financial developments of recent months.” A few sentences later, it concludes that “global economic and financial developments continue to pose risks.”

Back in January, the post-meeting press release warned that the FOMC is “closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.” In contrast, yesterday’s statement acknowledged that “economic activity has been expanding at a moderate pace despite the global economic and financial developments of recent months.”

Yesterday’s statement more directly attributes US economic sluggishness, and heightened risks to future growth, to factors at work outside the US. That sentiment sets the stage for a future statement by the Fed justifying an eventual rate hike as reflecting improved economic conditions outside the US.

What’s more, several central banks (including the Bank of Japan, the Bank of Canada and the Reserve Bank of South Africa) had their own monetary policy committee meetings this week, with the Bank of England set to adjourn today. With the European Central Bank adopting broad, new stimulus; with Europe facing multiple complex challenges; and with troubled emerging-market economies being sensitive to US monetary policy and US dollar fluctuations, a nod to international developments bolsters the Fed’s standing as a cooperating team player in the community of central banks.

4. A divided outlook for the economy and markets

Members of the FOMC appear to remain deeply divided in their views about the outlook for the economy and financial markets. In her press conference, Fed Chair Janet Yellen spoke at length about the lack of consensus within the committee with regard to upside and downside risks. This division left the FOMC unable to construct a balance of risks statement for the second consecutive time. Yellen conceded that although risks to the outlook have diminished, they still continue to warrant vigilance. She revealed that the committee could not come up with “a collective judgment” as to whether risks are weighted to the upside or the downside. In that context, it was not surprising that she could not forge a consensus around the decision not to raise rates. Esther George, the president of the Kansas City Fed and a long-time “hawk,” dissented.

5. The uncertain balance of risks

Despite a lack of consensus about the balance of risks, Yellen stated emphatically that the committee did not discuss the possibility that it may be forced sometime soon to reduce interest rates and increase monetary accommodation. In that context, she made it clear that the committee gave no consideration to the possibility that it may be forced at some future date to push policy rates into negative territory. As such, the committee clearly does not anticipate a strong or sustained economic downturn anytime soon. To do so would be a tacit admission that the committee fears that US monetary policy will not accomplish its tasks.

Strong dot-plot central tendency

Despite the lack of consensus within the committee regarding the economic forecast, a strong central tendency formed in the dot plot.

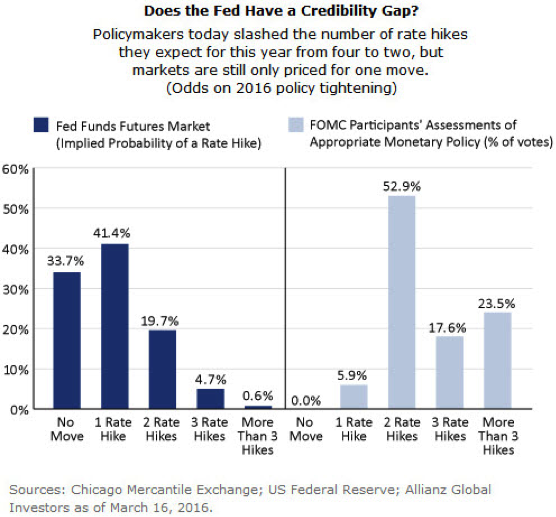

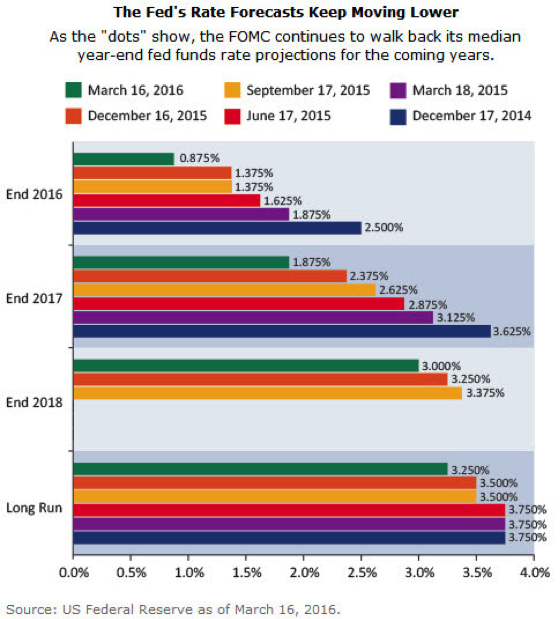

Accordingly, nine members of the committee see two 25-basis-point (bp) interest-rate hikes, to 0.875%, as the most appropriate path for the federal funds rate in 2016. Most likely, Governors Janet Yellen, William Dudley and Stanley Fischer (the Chair of the Board of Governors and the FOMC, the Vice-Chair of the FOMC and the Vice-Chair of the Board of Governors, respectively) fell into this group. In 2017, this group appears to favor four 25-bp hikes, bringing the year-end target federal funds rate to 1.875%, versus the 2.375% at year-end 2017 that was favored just three months ago.

For 2018, the dot plot calls for a slight acceleration in the pace of rate hikes, with the median dot showing 4.5 rate hikes and a year-end target federal funds rate of 3.0%. That compares with 3.5 hikes in 2018 and a 3.25% year-end rate lodged in the December 2015 median forecast.

The median projection for the longer-run neutral rate also came down a quarter of a percentage point, to 3.25%. That estimate is still probably still too high, but it has been moving down steadily, by 50 bps over the past year and by 75 bps since March 2014.

The lack of a rate hike complicates attainment of the ultimate goal

Nobody outside of the Fed can state authoritatively the extent to which market-based estimates of the probability of a rate change influence the FOMC’s decision-making. However, the futures-implied probability of four rate hikes in 2016 never was realistic, dropping earlier in March to below 1%; currently, the futures implied probability of two or more hikes this year is only 26%.

The FOMC’s toned-down vision of the appropriate path of interest-rate increases complicates the attainment of the committee’s stated goal to raise policy rates to their neutral, or normal, level as soon as is feasible. Speeches by two Fed governors discuss at length the need to shift risks away from monetary policy outcomes and toward the decisions by individual banking and financial institutions in individual markets. However, the press release and dots portray a committee that continues to follow a prudent policy that recognizes the asymmetric risks to tightening when at or near the zero lower bound.

Accordingly, just 16 months ago—in December 2014—policymakers envisioned an economic environment sufficiently strong to warrant a 2.5% federal funds rate at the end of 2016; now the median forecast puts it at 0.875%. It may be important to note that rate projections for 2017 have been cut each of the past five times the FOMC has released updated economic forecasts.

Investment implications of the FOMC’s policy slant

Financial markets in the US and in most other countries have so far endorsed the FOMC’s decision, with stock-market volatility diminishing further and prices of risk assets moving generally higher. The pricing at work in most money and fixed-income markets since January suggested that investors, for the most part, did not expect the FOMC to raise policy rates at this week’s meeting. Still, the announcements yesterday helped to clarify what likely will drive US monetary policy for some time to come.

We believe that yesterday’s announcements by the FOMC can be expected to boost investor confidence, at least temporarily. Over the near term, investors tend to take comfort from a diminished likelihood of an imminent policy rate hike, though Yellen did not rule out the possibility that the committee could act in June or even in April if all of the oft-stated preconditions for a rate hike are met. In addition, investors also can take a deep breath knowing now that the committee calls for a slower pace of rate increases when they do take place again.

In its communications yesterday, the Fed distinguished itself with its prudence, flexibility and patience, as well as its apparent resistance to a negative-interest-rate policy. In that regard, Yellen made it clear that the FOMC does not consider adoption of policies divergent from those adopted by other central banks to be disruptive to global economic and financial well-being. The removal of several sources of investor uncertainty tends to promote investment in risk assets.

Investors will need to pay particular attention to a wide range of measures of actual and expected inflation in order to anticipate the Fed’s rate-hike timetable in an informed way. Inflation and inflation expectation surprises to the upside may well steepen the long end of the yield curve, creating a particularly difficult environment for long-term bonds, especially those with very low coupons.

Meanwhile, investors likely will watch carefully the equity market’s reaction to a step-up in inflation. At first, rising inflation may be a positive signal for the stock market, as nominal wages rise and consumer demand strengthens, and as nominal profits go up, consistent with improved pricing power. However, vigilant investors will need to see how the FOMC reacts to rising inflation—whether it shuts inflation down at first sight or lets it run a bit to stimulate spending and credit growth. Inflation-sensitive sectors and industries (such as materials, financials and Treasury inflation-protected securities), could be early beneficiaries of rising inflation rates. How quickly and strongly the Fed ultimately reacts to the higher inflation rates will be critical to equity-market performance.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

About the Authors

Kristina Hooper is the US Investment Strategist and Head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law, a master's degree from Cornell University and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Steve Malin is an investment strategist with Allianz Global Investors. He has a B.A. in economics from Queens College and a Ph.D. in economics from the Graduate Center of the City University of New York.

Greg Meier is a strategist with Allianz Global Investors. He has a B.S. in business administration from the University of Montana and an M.B.A. from the University of Washington.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

AGI-2016-03-17-14748