IMPRESSIVE

From the State Street Global Advisors White Paper “Closing the Gender Gap of Advice”

• Women control roughly $11 trillion in investment assets.

• Women have become the primary or sole income earner in 4 out of 10 households with children.

• Women now earn more than half of all college degrees.

• Women tend to think long term: 45% focus beyond five years when it comes to their investment timeframe.

But some of the news is depressing:

• Only 39% of female investors feel understood by the investment industry.

• Only 14% of women age 50-69 have a high degree of confidence in their investing skills and only 11% of those 70-84 have a high degree of confidence.

MARKET TIMING? TEMPTING, BUT NOT A GOOD IDEA

The problem is that timing requires TWO correct calls — when to get out and when to get back in. Unfortunately for the market timer, markets recover just as quickly as they tank. While timers are sitting in cash waiting for the “right” time to reenter, the market booms. Here’s a test that may help you put timing in perspective. Can you name the top 10 timers of all time? The top 5? The top 1? No? Food for thought before you try it.

FOR EXAMPLE

USA Today 11/13/2008 Headline:

“Stocks tumble near 2008 lows on more grim news”

S&P 500 Annualized Performance (dividends reinvested)

Through 11/2009 26.8%

Through 1/2016 13.7%

Investment News

10/17/2011: “MSSB [Morgan Stanley] plans for the worst with new asset allocation” “Morgan Stanley Smith Barney LLC’s global investment committee is adopting an overweight position in safe havens and an underweight position in risky assets…”

10/31/2011: “The tea leaves say ‘sell,’ portfolio manager says”

S&P 500 Annualized Performance (dividends reinvested)

Through 10/2012 21.5%

Through 1/2016 13.5%

Obviously there are no guarantees that in the future market timing’s lack of success will repeat the past, but I don’t suggest betting against it.

COMING TO AN AIPORT NEAR YOU

See the first pictures (on the next page) of the new Boeing 797 Airliner, 40 seats wide with eight aisles — 1,000 passengers and a huge crew!

It can comfortably fly 10,000 miles (16,000 km) at Mach 0.88 or 654 mph (1,046 km/h) fully loaded! I think I’ll pass.

My associate Clay is a party pooper. In proofing this issue, he sent me the following from Snopes: “The image is a conceptual picture from a Popular Science article about the future of aviation, and has been circulated since at least early 1996 in fictitious articles proclaiming it to be Boeing’s response to competition from the Airbus A380 in the commercial airliner business.”

MORE FOOD FOR THOUGHT

Next time you think you might get some inside insight on the markets from prestigious financial publications, you might want to reflect on Barron’s June 8, 2015 cover story “Who Will Win?” The heading reads, “Of 19 Republican contenders for the presidency, only seven have staying power. We predict the last men standing will be Jeb Bush and John Kasich.”

How about Donald Trump? “The rest of the field, in our opinion, is unlikely to break out nationally, despite some ardent followers … real estate developer Donald Trump … have little chance of making it to the final heat.”

GOODBYE 2015

February 2 10-Year Treasury yield makes a new low at 1.67%.

August 11 China abruptly devalues its currency to stimulate its slowing economy.

August 25 U.S. stocks bottom after a 12% correction sparked by fears about slowing global growth. November 13 ISIS-linked terrorist kill 129 people in multiple attacks across Paris.

December 11 WTI crude oil hits a six-year low of $35.62 a barrel. The price plunged 33% in 2015. December 14 Barron’s

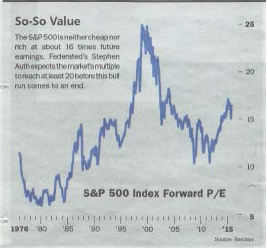

Looks a tad more rich than cheap to me.

BUT OPTIMISM SPRINGS ETERNAL

Headline in the January InvestmentNews:

“Advisors optimistic about 2016”

81% believe the economy will remain on par or improve over 2015

I hope they’re right!

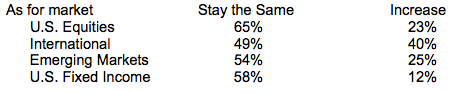

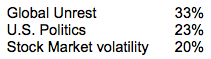

On the other hand, there are concerns — “Top risks facing the financial markets”

I’d put politics first.

COOL

At the beginning of the year, Financial Planning published the “150 RIA Leaders.” Noting that there are 59,422 Registered Investment Advisors (RIAs) and independent firms such as ours managing $2.7 trillion of client assets, the publication sorted for firms that were free of affiliation with broker-dealers, insurance firms, banks, and large outside investors to develop its list of the top 150. I’m proud to say E&K/FF made the list at #71 and we are only one of two listed from Florida (the other is W.E. Family Offices).

HELLO 2016

“Bullish, but Cautious” — A few examples of 2016 Year-End S&P 500 estimates from Barron’s top strategists:

The Optimist

Stephen Auth, Federated Investors 2500

The Pessimist

David Kostin, Goldman Sachs 2100

In Between

Jonathan Glionna, Barclays Capital 2200

Dubravko Lakos-Bujas, JPMorgan 2200

Savita Subramanian, BOA/Merrill Lynch 2200

Tobias Levkovich, Citi Research 2200

Adam Parker, Morgan Stanley 2175

Russ Koesterich, Blackrock 2175

Barron’s 12/14/2015

I like optimist.

A USEFUL SITE

Hospital Compare has information about the quality of care at over 4,000 Medicare-certified hospitals across the country. You can use Hospital Compare to find hospitals and compare the quality of their care. Just put in your zip code and it will give you a list of all the hospitals in your area and allow you to compare up to three at a time.

WARNING! MORE MARKET TIMING CAUTION

As usual, Money Magazine provides some useful tips. For example, here’s a reminder that most investors lose money by trying to market time. It’s the same story every year.

This may not seem like a big deal as the returns are so low; however, it is a BIG deal. Investor returns were 40% worse than they would have been had investors simply held their positions for the full year.

MIND-BOGGLING

From “DOL fiduciary rule will transform the annuity industry”:

61% of VA sales were in individual retirement accounts [my emphasis], according to Cerulli data. That’s little changed from 62% during the prior two years….

Fee-based variable-annuity sales only accounted for 4%, or $4 billion, of the $99 billion in total VA sales through the third quarter of 2015, according to Morningstar data. In full-year 2014, their share was 3.8% of a total $137.9 billion. Investment News Article

GUNS ACROSS AMERICA VETERAN TRIBUTE

KIND OF REMINDS ME OF ROBOS Planning without human intervention via computer algorithms is a hot topic today. I’m obviously biased, but it does seem to be a dangerous way to plan for your future. I’ll know more later this year as I’m working with a few other professors to study the efficacy of existing programs.

SPEAKING OF RESEARCH

I worked with the same group of academics on a paper titled “The Efficacy of Public Retirement Planning Software.” Our conclusion was highlighted in a Wall Street Journal article that was headlined:

“New Study Questions Retirement Planning Calculators’ Accuracy Available offerings of 36 such tools studied ‘are extremely misleading,’ researchers conclude in paper.” If you’re interested, you can find the full paper by clicking here.

KEEP THIS IN MIND

When someone tells you that the “big boys” have special insight into the markets, consider this. From Bloomberg News:

“MetLife Profit Falls 45% On Private Equity, Hedge Fund Slump MetLife Inc., the largest U.S. life insurer, said fourth-quarter profit slipped 45 percent as investment results deteriorated in private equity and hedge funds…”

MY FRIEND PATTI … … sent me a link to an article on Nerdwallet by Mike Eklund. Mike is an advisor who wrote an excellent piece titled “What a true financial advisor does.” I liked it so much, I thought I’d share some of his thoughts.

“Below are a few examples of how good planning in conjunction with a financial advisor can leave you with more money rather than less. A true financial advisor can help you:

• Stick to an investment plan to avoid panic selling and buying at market tops — moves that impact your long-term wealth much more than an advisor’s fee. Vanguard estimates that just two or three major decisions over a 30-year relationship can make up for the annual fees.

• Track your contributions to and withdrawals from your accounts and compare them with your goals, helping you reach or exceed those targets.

• Adjust your investment strategy to account for major life changes such as buying a house or starting a new job.

• Determine when and how to claim Social Security benefits.

• Determine how much life insurance you should have.

• Use tax planning to determine which accounts to save in during your working years and withdraw from during retirement.

• Allocate assets across all your accounts and rebalance your portfolio regularly.

• Maintain peace of mind about your retirement savings.

• Buy a new or second home.

• Minimize taxes after your death by assisting with the proper beneficiaries titled on your retirement accounts.

• Review all these items and others regularly to optimize your financial situation.”

OOPS!

In that same vein, my partner Steve sent me an excellent article, “Investment Advice That Will Pass Time’s Test,” by Bob Seawright, CIO at Madison Avenue Securities. I found these statistics particularly impressive.

“My friend Morgan Housel, a columnist for Motley Fool, looked at the average Standard & Poor’s 500 stock index forecast made by the 22 chief market strategists of the biggest banks and brokerage firms from 2000 to 2014. On average, these annual forecasts missed the actual market performance by an incredible 14.6 percentage points per year (not 14.6%, but 14.6 percentage points!)… Sadly, such dreadful forecasting performance is indicative of dreadful investment performance. The vast majority of investment strategies are predicated upon the ability to forecast the future. These results are no better than the forecasts. As longtime chair of the Yale Endowment Charles Ellis outlines it, research on the performance of institutional portfolios shows that after risk adjustment, 24% of funds fall significantly short of their chosen market benchmark and have negative alpha, and 75% of funds roughly match the market and have zero alpha, while well under 1% achieve superior results after costs — a number that is not statistically significantly different from zero, largely because of fees…. To pick one particularly egregious example, hedge funds — despite (and partly because of) enormous fees — have badly underperformed. Since 1998, the effective return to hedge funds has barely been 2% per year, half the return achieved by simply investing in Treasury bills.”

LINDA’S RETIREMENT

“Yet the very anxieties and consumer ignorance that lead us to seek financial advice make us vulnerable when advisors face financial incentives to steer us towards overpriced or unwise investment products…

“It’s not that financial professionals are defrauding people or are criminals on the Bernard Madoff model. They are simply steering people into investments that are notably more costly than they need to be.”

WARNING!

A wise reminder from Bill Miller in Blomberg defending his reputation (he was a long-term golden boy money manager for Legg Mason until his portfolios were crushed during the grand recession). “The press was very quick to anoint people … who got something right ‘once in a row.’” Remember that next time some guru brags about his or her last (and only) right call.

CLOUDY CRYSTAL BALLS

Even with institutional crystal balls, outguessing the markets in the short term can be hazardous to your wealth. According to Bloomberg…

“Goldman Sachs Group Inc. said about 40 percent of its loans and lending commitments to oil and gas companies are to junk-rated firms.…

“Concerns about banks’ energy loans have helped spur share declines for lenders after the price of oil fell 42 percent in the past 12 months through Friday. … Goldman Sachs’s total is below some of its biggest competitors. Citigroup Inc.’s funded and unfunded commitments amounted to $58 billion…. Most of Wells Fargo & Co.’s $17 billion in outstanding energy loans is for companies that aren’t investment grade.” Click here for the full article.

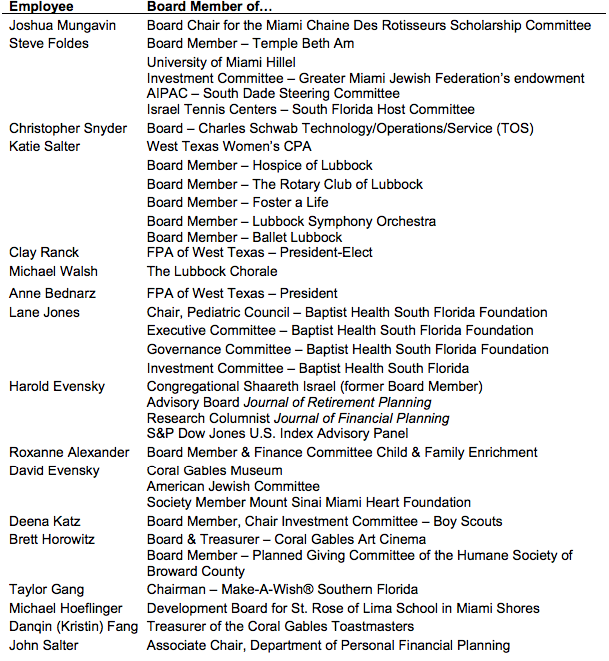

I’M UNBELIEVEABLY PROUD … … of my partners’ and associates’ commitment to our community:

AND THEY HAVE GREAT COMPANY

According to Money magazine in 2015

Value of time donated to charity work...................... $173,000,000,000 (that’s BILLIONS!)

Dollar contributions were ..............................................................................$358.4 billion!

WANNA BET?

According to Bloomberg, opportunities to bet on the Super Bowl abound. Next year you might consider betting on how long the national anthem lasts or what color Gatorade will be dumped on the winning coach. Among the most popular is “will the coin toss land on heads or tails?” This is all available on the Bovada betting site. P.S., I don’t recommend it.

AND EVEN MORE FOOD FOR THOUGHT

Headline – “Billionaire Dan Och's Hedge Fund Firm Plunges By 26%”

“There have been plenty of indications in recent months of the troubles being faced by prominent hedge fund managers who have been unable to navigate volatile markets without suffering setbacks. Big names like Bill Ackman, David Einhorn, Leon Cooperman and Larry Robbins have posted big losses in their hedge funds since last summer. Billionaire Dan Och’s hedge fund firm is now showing the latest sign of stress in the rich but reeling hedge fund industry.…

“Och-Ziff is the only big U.S. hedge fund firm with shares that are publicly-traded and it is somewhat of a window on what is going on inside these opaque businesses. It is also a reminder of why so few hedge fund mangers have joined Och in taking their firms public and listing them on an exchange. Shares of Och-Ziff plunged on Thursday by 26% and are now down by 70% in the last year.”

Click here for the full article.

THIS WAS FUN

I’ve served for a few years on the S&P Dow Jones U.S. Index Advisory Panel. We meet once a year in N.Y. and address questions raised by the S&P Index Committee. It is a bit different than my normal activities as almost all members are high-level representatives of global financial services firms, so it is also, for me, a major learning experience. This year’s meeting focused on the handling of Chinese A-shares in global indexes, Smart Beta, and finally, a discussion regarding U.S. real-time index calculations.

MORE SOAP BOX

Fiduciary duty for ALL financial advisors? Why? Well, a new report by three University of Chicago professors provides a partial answer. From the abstract:

“We construct a novel database containing the universe of financial advisers in the United States from 2005 to 2015, representing approximately 10% of employment of the finance and insurance sector. Roughly 7% of advisers have misconduct records. Prior offenders are five times as likely to engage in new misconduct as the average financial adviser… We show that differences in consumer sophistication may be partially responsible for this phenomenon: misconduct is concentrated in firms with retail customers and in counties with low education, elderly populations, and high incomes. Our findings suggest that some firms “specialize” in misconduct and cater to unsophisticated consumers, while others use their reputation to attract sophisticated consumers.”

Some surprising names on their list of firms with the percent of advisors who have been disciplined for misconduct:

The full study can be downloaded by clicking here.

GOTTA FEEL SORRY FOR HIM

It’s not my kind of music, so I have no opinion about his talent, but bankruptcy is no fun. Of course it’s supposed to mean you’re out of money. The bankruptcy judge obviously agrees as he’s ordered 50 Cent back to court to justify his Instagram photos flaunting stacks of money. From my associate Michael:

Click here for full article.

A NICE ENDING

Our Texas office personnel have become avid supporters of Ballet Lubbock. The real attraction isn’t the amazing skill and talent of the performers (although that is certainly an attraction), but rather the Ballet’s mission — to make Lubbock a better place to live. Their most recent effort literally brought tears to our eyes as we learned about their Arts in Medicine program. Kicking off with a special “Nutcracker Festival,” six performers presented a 30-minute condensed version of the Nutcracker for children who physically could not attend the ballet. The artists will be following up with personal lessons for the kids. Here are some wonderful pictures from the first class as the amazing Marcos Vasquez, a fourth-year member of the company, works with his first students, Landon and Mahari.

I hope you enjoyed this issue and that wherever you are, you’re beginning to see a bit more of the warmer weather. I’ll “see” you again in a few months.

Harold R. Evensky, CFP®, AIF®

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management