Senior Floating Rate Loans Provide Income and Value

While equity volatility at the start of the year prompted handwringing among many investors, one of the most vexing issues in the current environment is in the fixed income market.

Income-oriented investors face a troublesome dilemma: Traditional “safe haven” assets provide historically low yields and many higher-yielding fixed income securities bring either increased credit or duration risk. Both of these risks are meaningful since credit instruments could materially decline if the economy slows and, conversely, long-duration securities could be drastically impacted if inflation picks up or if the Federal Reserve raises interest rates faster than consensus estimates.

Although it may appear safe to stretch for yield in longer-duration securities as central banks move from zero interest rate policy (ZIRP) to negative interest rates (NIRP), investors should be wary of adding interest rate risk to defensive, income-oriented portfolios. As a reminder, long-duration securities suffered a severe selloff during the mid-2013 “taper tantrum,” when the Federal Reserve communicated a policy change and investors in 10-year Treasuries experienced 10% losses over only four months.

The Investment Strategy Group would like to thank Joe Lynch for his valuable contributions to this piece. Joe, Stephen Casey and Dan Doyle currently manage $9.9 billion AUM in senior floating rate loan strategies, including separately managed accounts and mutual funds, for Neuberger Berman.

We believe one area of the market—senior floating rate loans— could help bridge some of these issues. These securities have a relatively high current income profile. They can also help mitigate some of the risks of rising interest rates, and could provide more of a downside buffer than high yield bonds and other credit securities in a mild economic contraction.

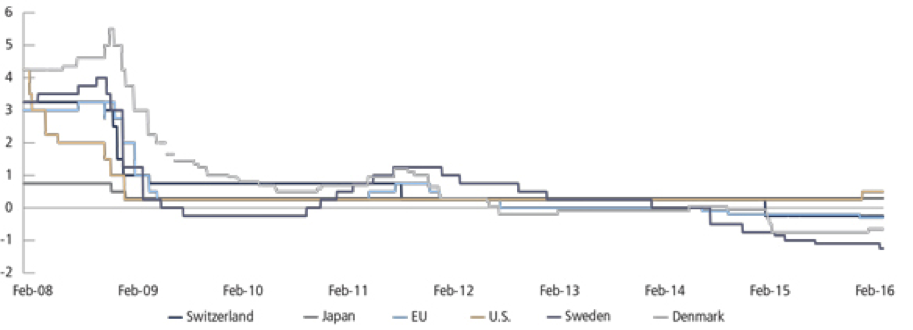

Figure 1: From ZIRP to NIRP—Declining Short-Term Risk-Free Rates

Source: FactSet, data through February 29, 2016. Short-term rates are represented as follows: Denmark—certificate of deposit rate, Sweden—deposit rate, U.S.—Fed Funds Rate, EU—deposit facility rates, Japan—basic discount and loan rates, Switzerland—SNB target rate.

Senior Floating Rate Loans: How They Work

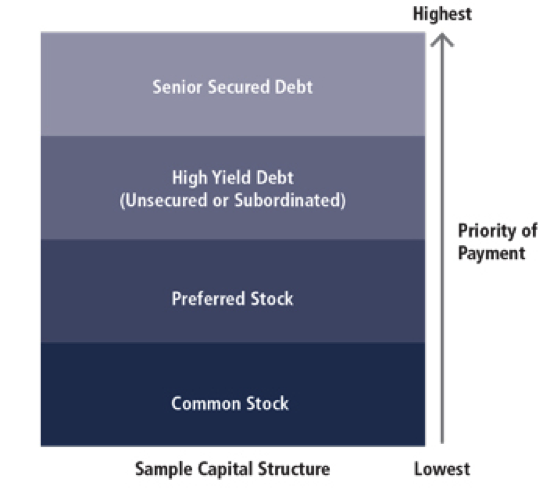

Figure 2: Senior and Secured

Position of Loans in the Company Capital Structure

Source: Neuberger Berman.

Senior floating rate loans (also known as floating rate secured loans or leveraged loans) are loans made by banks to non-investment grade companies to finance various corporate activities, including mergers and acquisitions, leveraged buyouts, recapitalizations and capital expenditures. The loans are floating rate, which means that the coupons readjust every quarter to a spread over a base rate (typically LIBOR). If interest rates rise (or fall), the coupon on these loans rises (or falls) along with market conditions. The loans are generally secured, implying they are in the senior-most position in the capital structure. Because of this, holders of these loans typically have a first priority lien on the assets of the borrower and must be repaid before any other obligations, including to bondholders or stockholders, in the event of a default.

The floating rate and secured characteristics are key reasons why senior loans are considered less risky than high yield bonds, which do not have readjusting coupons and are both non-secured and typically subordinate to loans. The table below provides a more detailed comparison between senior loans and high yield bonds.

Figure 3: Comparison—Senior Floating Rate Loans vs. High Yield Bonds

|

Senior Floating Rate Loans |

High Yield Bonds |

|

|

Security: |

Secured by stock and assets |

Generally unsecured |

|

Seniority: |

Structurally senior |

Subordinate to secured loans |

|

Interest Rate/Coupon: |

Floating rate |

Fixed rate |

|

Tenor: |

Typically 6–8 years |

Longer-dated, typically 8–10 years |

|

Amortization: |

Required quarterly principal payments + residual at maturity |

Bullet payment at maturity |

|

Optional Prepayments: |

Typically prepayable at par without penalty |

Call protected |

|

Mandatory Prepayments: |

Most credit agreements require an issuer to prepay loans with proceeds from: · Debt and equity issuance · Asset sales · Excess free cash flow |

Typically, the indenture contains some provisions for mandatory prepayments once loans are fully repaid if proceeds are not reinvested during specified period |

Source: Neuberger Berman.

Recent Volatility: Shaky Sentiment but Steady Fundamentals

Concerns about an economic slowdown caused a material selloff in “risk assets” earlier this year. High yield bonds were particularly hard-hit due to the large proportion of energy and mining companies in the asset class. Year-to-date (through February 29), the benchmark Barclays U.S. High Yield Corporate Bond Index was down 1.0%, following a 4.5% decline in 2015, and high yield spreads in the energy sector have recently widened to a near record +1,439 basis points (bps) over Treasuries. The weakness in the high yield market has impacted the floating rate loan market. Spreads for the S&P/LTSA Leveraged Loan Index have risen from lows of around 450bps in 2013 to current levels of around 665bps and average loan prices have fallen to approximately 91% of par.1

Investment Perspective

We believe loans are attractively priced and that much of the recent selloff is sentiment-driven, with loan prices decoupling from fundamentals. The broad S&P/LTSA Leveraged Loan Index yields 7.1%, compared to 2.3% for the Barclays Aggregate Bond Index and 1.9% for the Barclays Municipal Bond Index.1 Loans also offer much lower duration than many other fixed income asset classes.

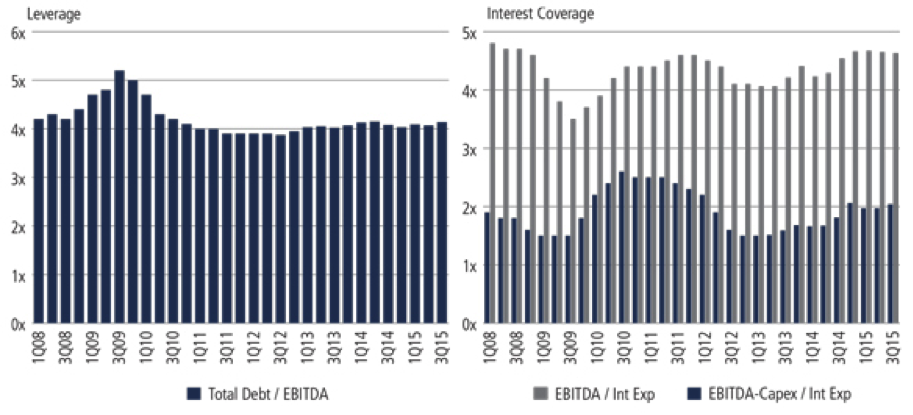

Key fundamental financial metrics such as leverage and interest coverage ratios (the ability of companies to pay interest on existing debt obligations) lend support to the notion that the general health of loan issuers remains strong. In addition, the “maturity wall” appears manageable: Only 14% of loans in the market are due in the next three years, which may suggest a somewhat low risk that issuers will be unable to refinance their upcoming debt maturities.

Figure 4: Leverage and Interest Coverage Ratios Look Strong

Source: J.P. Morgan, data as of September 30, 2015.

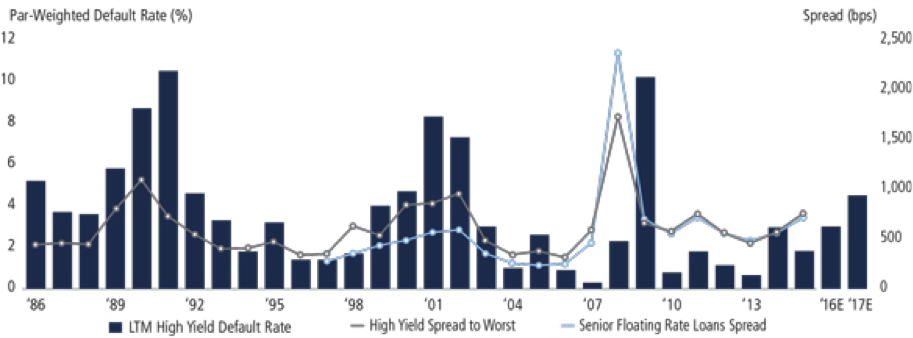

Figure 5: Spreads vs. High Yield Default Rate

Source: J.P. Morgan Default Monitor. Default Rate based on par amounts. High Yield Spread to Worst is represented by the J.P. Morgan Global High Yield Index. Senior Floating Rate Loans Spread is represented by the Discount Margin (3-year life) of the S&P/LSTA Leveraged Loan Index.

There are macro risks. If economic conditions deteriorate significantly, loan prices and liquidity could drop as they did in late 2008. However, we do not anticipate a recession for the next 12 months and senior loans could generally be more defensive than high yield bonds if we do enter a downturn, as loans are structurally senior to high yield bonds. From 1990 to February 2016, the average recovery rate from defaulted loans was approximately 67% versus 40% from high yield, or more than 50% higher.2 Thus, we believe the incremental yield or spread on loans over U.S. Treasuries should generally be lower than for bonds. However, this is not currently the case, which supports our view that loans are currently trading at a more attractive valuation than bonds.

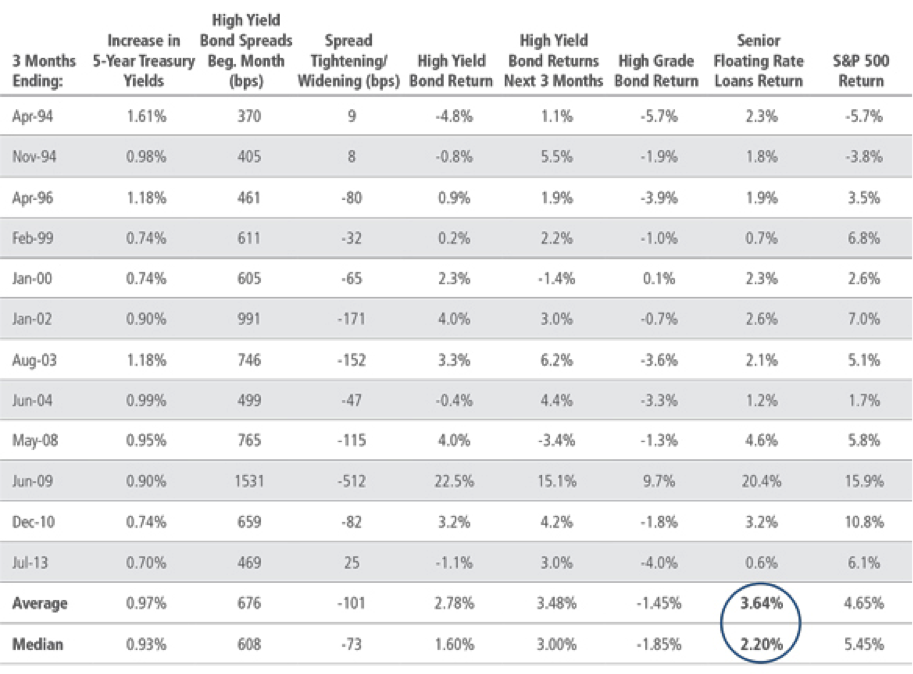

Another common concern for fixed income strategies today is the potential impact of rising U.S. interest rates. Given current economic headwinds and the aggressive easing bias of many non-U.S. central banks, we anticipate only gradual and moderate rate increases from the Federal Reserve. However, should interest rates move up faster than anticipated, it’s worth noting that floating rate loans will reset their coupons. Notably, floating rate loans have often performed well in rising rate environments and, since 1994, have had positive returns in every period of rising rates. As shown below, floating rate loans have on average returned +3.6% over the 12 periods of rising interest rates since 1994. Conversely, high grade bonds have declined by an average of -1.5% during the same 12 periods.

Figure 6: Performance in Rising Rate Environment

Performance of loans, bonds and equities during periods of rising interest rates since 1994

Source: J.P. Morgan; S&P/LCD; Neuberger Berman. The table presented above represents performance when 5-Year Treasury yields rose 70 basis points (or more) during a 3-month period since 1994. High Yield Bond Return is represented by J.P. Morgan Domestic High Yield Index. High Yield Bond Returns next 3 months represent the 3-month return of the J.P. Morgan High Yield Index for the 3-month period following the 3 months ending period, as listed in the first column of the table above. High Grade Bond Return prior to 1999 is represented by Merrill Lynch Corporate Master Index, and after 1999, High Grade Bond Return is represented by J.P. Morgan High-Grade Index (JULI). Senior Floating Rate Loans Return prior to 2007 is represented by S&P Performing Loans, and after 2007, Senior Floating Rate Loans Return is represented by J.P. Morgan Leveraged Loan Index. Past performance is not indicative of future results. Indices are unmanaged, include reinvestment of any dividends, capital gain distributions or other earnings and do not reflect any fees or expenses.Investors cannot invest directly in an index.

Conclusion

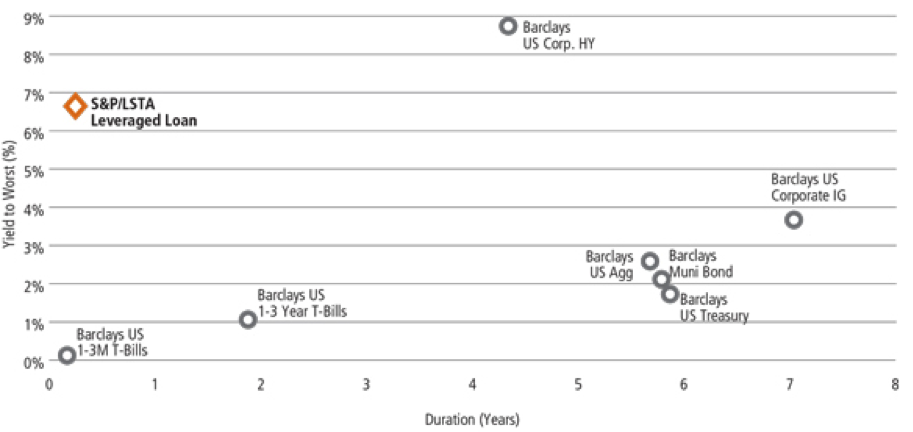

We believe floating rate loans currently provide a compelling opportunity for income-oriented investors; the asset class has a relatively high income profile, is generally more defensive than high yield bonds and can also help mitigate against rising interest rate risks (see Figure 7).

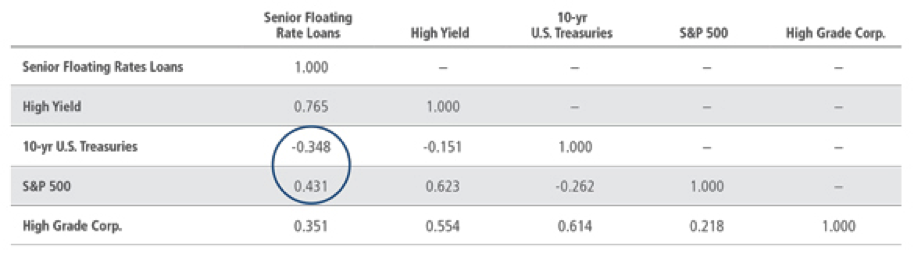

In addition, over the long term we believe that floating rate loans can provide valuable diversification benefits to a portfolio. Floating rate loans typically exhibit low correlation to traditional equity securities and a low or negative correlation to traditional fixed income securities (see Figure 8). Thus, loans have the potential to help mitigate equity market drawdowns and heightened volatility.

Figure 7: Loans Provide High Income with Low Duration

Source: Barclays; S&P/LSTA; Neuberger Berman. As of December 31, 2015. Senior floating rate loans are represented by the S&P/LSTA Leveraged Loan Index. Yield to Worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting. The yield to worst is calculated by making worst-case scenario assumptions on the issue by calculating the returns that would be received if provisions, including prepayment, call or sinking fund, are used by the issuer. Indices are unmanaged, include reinvestment of any dividends, capital gain distributions or other earnings and do not reflect any fees or expenses. For the S&P/LSTA Leveraged Loan Index we have used the Yield to Maturity. Past performance is not indicative of future results. Investors cannot invest directly in an index.

Figure 8: Loans Exhibit Low Correlations to Traditional Stocks and Bonds

Asset Class Correlations, 1997–2015

Source: Standard & Poor’s, as of December 31, 2015. Senior Floating Rate Loans are represented by the S&P/LSTA Leveraged Loan Index; High Yield is represented by the Bank of America-Merrill Lynch US High Yield Master II Constrained Index; US Treasuries are represented by Bank of America-Merrill Lynch 10-Year Treasury Index; Equities are represented by the S&P 500 Index; and High Grade Corporates are represented by the Bank of America-Merrill Lynch High Grade Corporates Index. Past performance is not indicative of future results. Indices are unmanaged, include reinvestment of any dividends, capital gain distributions or other earnings and do not reflect any fees or expenses. Investors cannot invest directly in an index.

Source: Standard & Poor’s, as of December 31, 2015. Senior Floating Rate Loans are represented by the S&P/LSTA Leveraged Loan Index; High Yield is represented by the Bank of America-Merrill Lynch US High Yield Master II Constrained Index; US Treasuries are represented by Bank of America-Merrill Lynch 10-Year Treasury Index; Equities are represented by the S&P 500 Index; and High Grade Corporates are represented by the Bank of America-Merrill Lynch High Grade Corporates Index. Past performance is not indicative of future results. Indices are unmanaged, include reinvestment of any dividends, capital gain distributions or other earnings and do not reflect any fees or expenses. Investors cannot invest directly in an index.

1 Data as of February 29, 2016.

2 Source: J.P. Morgan Default Monitor, March 1, 2016. Average issue-weighted recovery rates based on price 30 days after default date. 2009 adjusted recoveries are based on year-end prices.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types.

The views expressed herein generally reflect those of Neuberger Berman’s Investment Strategy Group (ISG), which analyzes market and economic indicators to develop asset allocation strategies. ISG consists of investment professionals who consult regularly with portfolio managers and investment officers across the firm. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events may differ significantly from those presented. Investing entails risks, including possible loss of principal. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

A bond’s value may fluctuate based on interest rates, market conditions, credit quality and other factors. You may have a gain or loss if you sell your bonds prior to maturity. Of course, bonds are subject to the credit risk of the issuer. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the investor’s state of residence. High-yield bonds, also known as “junk bonds,” are considered speculative and carry a greater risk of default than investment-grade bonds. Their market value tends to be more volatile than investment-grade bonds and may fluctuate based on interest rates, market conditions, credit quality, political events, currency devaluation and other factors. High yield bonds are not suitable for all investors and the risks of these bonds should be weighed against the potential rewards. Neither Neuberger Berman nor its employees provide tax or legal advice. You should contact a tax advisor regarding the suitability of tax-exempt investments in your portfolio.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/ disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

Certain products and services may not be available in all jurisdictions or to all client types.

© 2009-2016 Neuberger Berman LLC. | All rights reserved