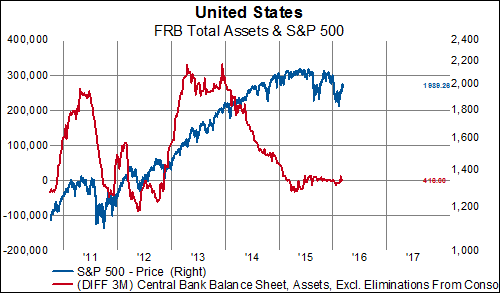

Ahead of tomorrow’s monetary policy meeting at the ECB, a majority of respondents expect both a cut in interest rates and an increase in the amount of monthly purchases in the Public Sector Purchase Program (PSPP) that began about a year ago. Speculation that markets may be disappointed should not come as a surprise, however. As we have noted here on multiple occasions, ECB asset purchases havenot been positively correlated with rising stock prices (in contrast to the effects of asset purchases by the Federal Reserve).

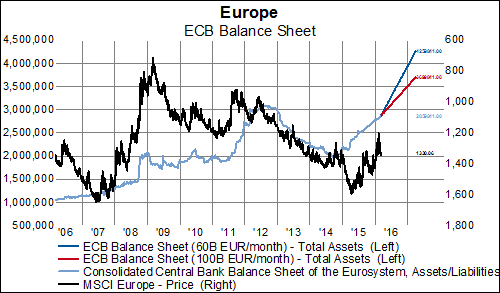

In the chart below, we plot the MSCI Europe (black line, inverted, right scale) against ECB assets (light blue line). The red and darker blue lines represent the current pace of asset purchases (60 billion euro per month) and what the trend would look like with an increase to 100 billion euro per month, respectively. As we can see, European stocks actually rose as the balance sheet shrank from all-time highs in 2012, falling as the level of assets increased sharply early last year.

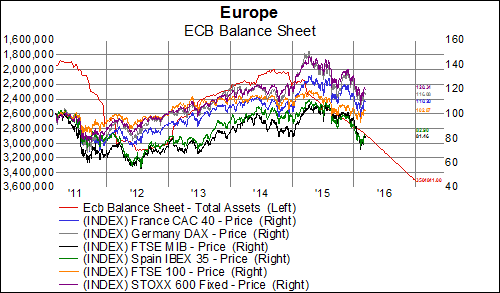

Country-specific stock indices have followed a similar pattern.

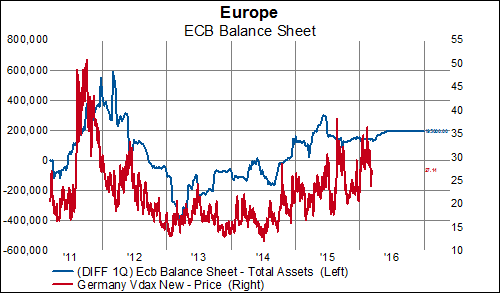

In addition, volatility of the German DAX has increased to levels not seen since 2012.

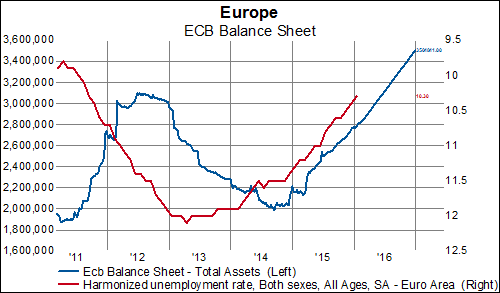

And, while the unemployment rate has fallen back to 2011 territory…

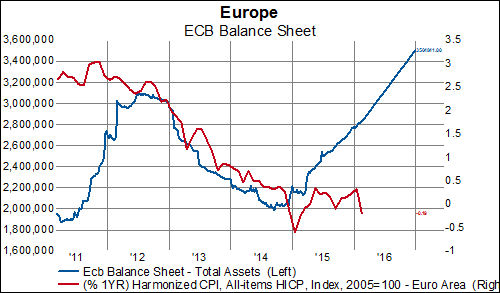

Perhaps most frustrating for policy makers, inflation has been largely un-moved by their efforts so far.

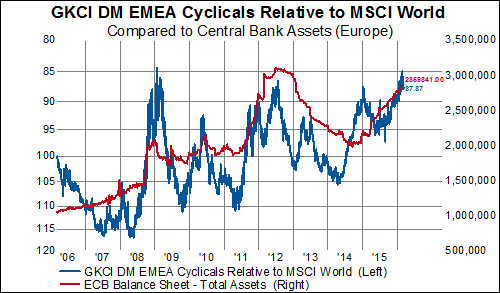

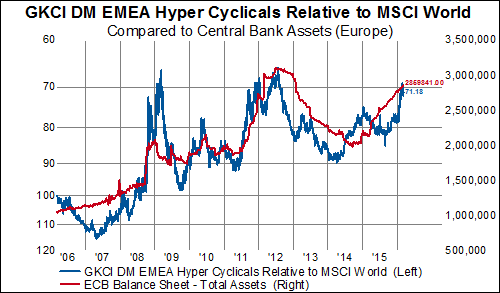

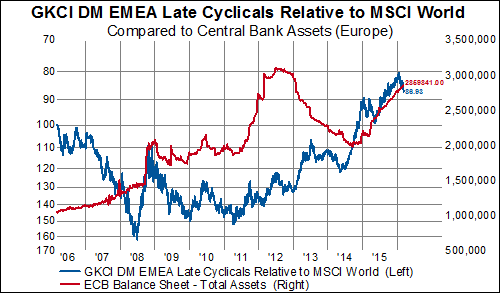

The lack of reflationary effects, in general, can be discouraging to any investors charged with selecting European holdings. But all hope is not lost– when we break down the overall market into our oft-cited baskets, we find that the Counter Cyclicals could offer some opportunity (especially when compared to the Cyclical groups).

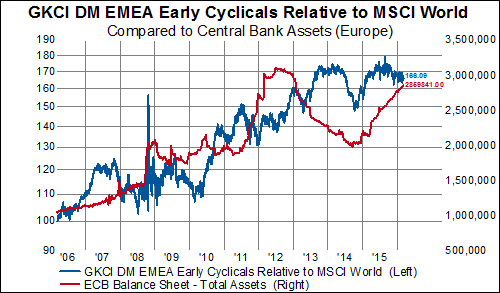

***note that the axis for the Cyclical groups below is inverted, meaning that they have underperformed against the broader index as ECB assets have expanded.

One Cyclical group that has defied this trend? Early Cyclicals (aka Consumer Discretionary stocks).

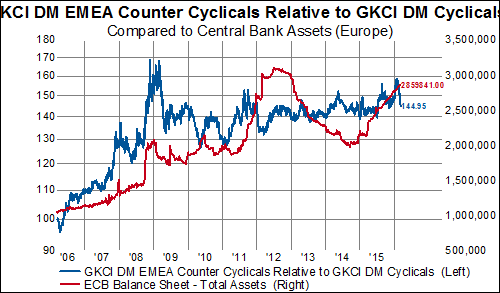

EMEA Counter Cyclical stocks (Consumer Staples, Health Care, Telcomm, and Utilities) have outperformed Cyclicals in the developed world by nearly 45% over the last decade, largely in-line with changes in the size of the ECB’s balance sheet.

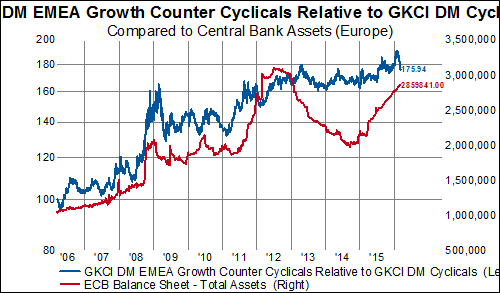

The Growth Counter Cyclicals (Consumer Staples and Health Care) in EMEA have performed even better, rising more than 75% relative to the Cyclicals over the last ten years.

Based on the positive relationship with ECB asset purchases, the best places to hunt for compelling European holdings should continue to be the Consumer Staples and Health Care sectors.