The “Gasoline Dividend” May Not Be That Powerful

- The “Gasoline Dividend” May Not Be That Powerful

- February’s Payroll Report Eases Recession Concerns

- The U.S. Job Market Is Strong But Uneven

I grew up in the city of Chicago, riding trains and buses to get where I needed to go. I didn’t get my driver’s license until I was 21 years old, after my wife decided we would be moving to the suburbs. She was actually the one who taught me how to drive; I would not recommend that arrangement to couples hoping to spend many happy years together.

It was only then that I became cognizant of gasoline prices and the impact they had on our monthly budget. The cost of a gallon had recently burst above $1, a shock to the system for Americans.

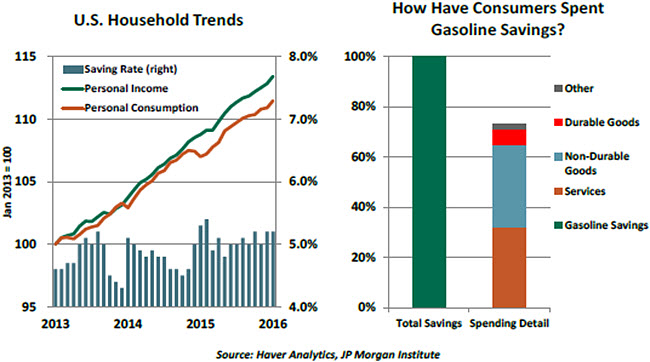

Flashing forward to the present day, the price of gas has again burst through a threshold once thought unapproachable. This time, though, the invisible line was at $2 per gallon. But happily, we breached it on the downside. The plunge in energy prices has freed an immense amount of household income to use for other things. In aggregate, U.S. consumers are estimated to have saved more than $100 billion last year, which analysts anticipated would add more than a half-percent to the rate of economic growth.

But that boost has not been apparent to the naked eye. What happened to the money? Answers begin to emerge once you look beneath the surface.

-

Only a little bit has been saved. As illustrated in the chart below, growth in consumption has lagged growth in income for over a year. The U.S. saving rate has risen, but not dramatically. At 5.2%, it is twice as high as it was prior to the financial crisis, but it has been essentially unchanged for most of the past three years. There is also little evidence that households have used gasoline savings to accelerate their debt retirement.

Studies published by credit card issuers, who can examine spending habits at a very granular level, corroborate this finding. One firm estimated that 80% of America’s gasoline savings was spent on other retail categories. This contradicts the contention that households hesitated to spend the windfall for fear that it might be transitory.

The narrative of newly frugal Americans saving their energy dividends is a popular one. Unfortunately, it’s not yet evident in the data. -

We’ve substituted one imported product for others. National income accounts add exports and subtract imports from domestically produced goods and services to calculate gross domestic product (GDP).

The United States produces a lot of oil but is still a major importer. So when gasoline gets cheaper, the nation’s purchases of imported products declines. This leaves more room in monthly budgets for purchases of domestic products, which would boost GDP.

As shown in the earlier chart, consumers spent about one-third of their gasoline savings on services, which are produced domestically. However, if households take their gasoline savings and purchase other imported products, the net benefit to U.S. economic growth is muted. As an example, sales of video and audio equipment spiked during the past six months; a substantial fraction of those items come from overseas.

-

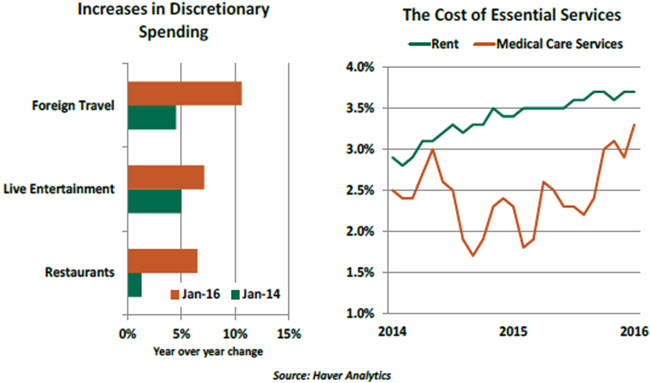

Families are eating out more and taking more vacations locally. Increased spending on meals away from home is one of the clearest signs of incremental largesse. This category rose by 6.5% over the past year.

As well, total miles driven on American roads rose by more than 3.5% in 2015, the largest increase in 20 years. Many of those miles were driven in larger vehicles, which enjoyed renewed popularity. Hotel occupancy jumped last year to a record level. And for those who can afford it, live entertainment and foreign travel became more popular.

-

Essential costs are rising. The data suggest that households with modest incomes are enjoying the biggest proportional gasoline savings. Those households are also more likely to rent than own their homes; rents have risen steadily as vacancy rates for multifamily properties decreased. In addition, medical costs are rising a little more rapidly after several quiescent years.

The increases in these categories, which lie outside the retail sales data, may account for the 20% of gasoline savings that were not spent on other retail categories.

Taking all this together, it appears that a good portion of America’s gasoline savings are being spent, but the impact on aggregate consumption has been muted.

Americans aren’t the only ones getting a gasoline dividend, and they’re not the only consumers who matter to the global economic outlook. But because we drive much more than other cultures do, cheaper fuel is potentially more beneficial to us. And U.S. consumption is critical to exporters the world over. So the focus on household consumption here is intense.

The potential release of pent-up gasoline savings has been cited as an upside for the consumer outlook this year. But the data suggest that this tailwind may not be as powerful as some might think.

Global Headwinds Do Not Prevent Hiring in the United States

On balance, the February employment report offers relief for those concerned about tightening financial conditions translating into economic weakness.

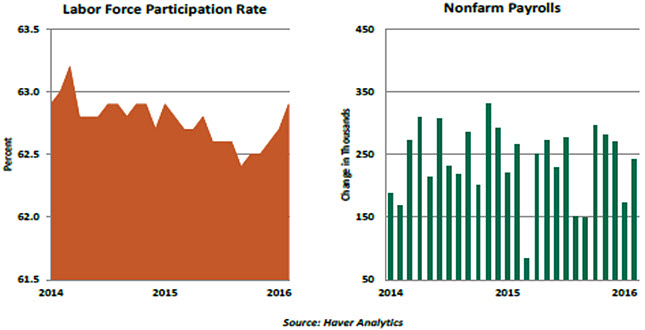

Payroll employment increased 242,000 in February, and revisions of the prior two months added 30,000 more jobs. The three-month moving average of new jobs is 228,000 – far above the pace needed to absorb the growth of the labor force. This was a very welcome reversal of the modest job gains we saw last month.

The unemployment rate held steady at 4.9%, while the labor force participation rate increased two notches to 62.9%. The 0.4 percentage point increase of the participation rate during the latest 3-month period is the best since 2010. This suggests that conditions are improving to the point that discouraged workers are returning to the labor force.

Goods-sector employment fell 15,000, reflecting a loss of jobs in the oil-related industry, an increase in construction jobs and a decline in factory jobs. The 245,000 jump in service-sector employment more than offset the weakness of hiring in the goods component. Heath care (+57,000), retail trade (+55,000) eating and drinking places (+40,000), and education (+28,000) posted the large increases in employment.

The 2.2% year-to-year increase in hourly earnings is a deceleration from the average seen during the last three months. Compensation in the financial sector dipped for the first time since June 2015, suggesting the decline could be a temporary factor. Hiring has registered significant gains on a sequential basis, but the trend of employment on a year-to-year basis is positive but slowing. This development appears to be a reason for the disappointment in wages.

The positive job report should lead to a spirited discussion at the March 15-16 Federal Open Market Committee meeting. “Hawks” will point to the strong hiring trend and stress that the Fed’s favored core inflation measure has risen 1.7% from a year ago (which is not too far from the Fed’s 2.0% inflation target). On the other side of the spectrum, the doves will point to the deceleration in hourly earnings and headwinds from weak global economic conditions. The Fed’s rhetoric has repeatedly been that it will pursue a “gradual” tightening of monetary policy. March is off the table, but our call for June and December policy rate changes remains in place.

Looking at the Labor Market with a Different Lens

The latest U.S. unemployment rate is close to the Fed’s estimate of full employment. But the impressive jobless rate conceals details that are less favorable and suggests a pause before we declare that the labor market is at its peak.

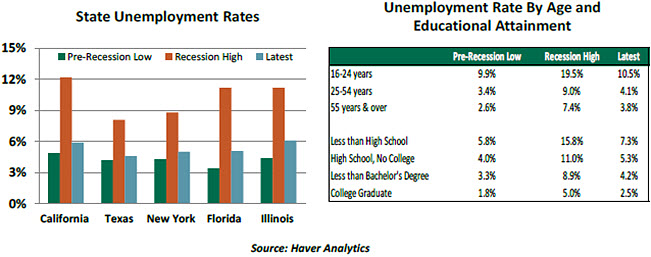

The current business expansion is just shy of turning seven years old, and it is the fourth-longest in the post-war period. Gains in overall employment have been very strong, and the U.S. jobless rate has fallen from 10% in early 2009 to 4.9% today. That may seem less impressive than the last expansion, which brought the nation’s unemployment rate down to a low of 4.4% in December 2006. But the unemployment rate peaked at 6.3% in the 2001 recession, thus the gains in employment were smaller.

Nonetheless, the report card for job growth is mixed. A look underneath the national aggregates reveals that the recovery in the job market, like the recovery in general, has been very uneven. Unfortunately, there may not be anything the Federal Reserve can do about that. Currently, the unemployment rate in 36 states remains higher than the pre-recession low. The five largest states measured by GDP all show a higher jobless rate today than the low seen in the prior cycle. This regional performance prevents many Americans from feeling confident that conditions are improving.

Dissecting employment conditions by age offers another view. The unemployment rate has declined across age categories from the highs seen during the last recession. But the latest readings indicate that those in their peak earnings years are seeing joblessness that is still higher than it was at the peak of the last expansion.

Classifying employment conditions by educational attainment also illustrates asymmetries in performance. Joblessness among workers with higher education levels has gotten closer to its pre-recession low, while those with more-modest schooling have had a more difficult time getting back to work.

Can Fed policy transform hiring trends such that a lower unemployment rate is achievable across all states and groups in the months ahead? Likely not.

First, monetary policy directly influences interest rates and not the labor market. The Fed buys Treasury or mortgage-related securities to adjust credit conditions. Sellers of these securities reinvest proceeds and bid up price of assets, which creates a positive wealth effect. The accommodative stance of the Fed helps to increase spending by businesses and households. Spending lifts production and increases demand for labor. Thus, there are several steps involved before the labor market sees the benefit of monetary policy easing.

Second, the Fed’s policy cannot guarantee prosperity for every industry and region, given the global forces at play. Even the beneficial impact of accommodative policy may not be enough to offset the decline in energy prices challenging Texas’ economy, for example. As another example, China’s economic moderation may be limiting California’s economic progress, as the state relies in part on commerce with Asia.

Finally, monetary policy cannot directly address structural unemployment, which stems from factors such as a mismatch of job skills, regulation and the aging workforce. It is widely recognized that a large share of part-time unemployment today reflects structural changes in the economy. Factory employment has maintained a downward trend since the 1970s, and the services component of the economy continues to climb. Non-monetary policy reforms such as workforce retraining and education are necessary to address this sort of unemployment, which is not within the Fed’s remit.

Disparities in the labor market exist under both robust and soft market conditions due to differences in economic resources, education and structural factors. Monetary policy is a “blunt tool” that cannot be expected to produce universal prosperity.