RIP Central Banks: Examining Negative Rate Scenarios

Beneath the turmoil in emerging markets and commodities, global central banks have resorted to unprecedented measures to stoke growth. Interest rates in Japan and parts of Europe are now negative, with Japanese 10 year bonds recently yielding 0%! Despite central banks' best efforts, increasing growth has been close to impossible. Long terms changes to the global economy have made central bankers increasingly irrelevant and sowed the seeds for deflation and slow growth.

Helicopter Ben Et Al.

Conventional economic wisdom tells us that in times of a sluggish economy, central banks can spark growth by easing monetary policy. Typically, this has come in the form of low interest rate policies. Low rates decrease the cost of borrowing, increasing both spending and inflation. More recently, central banks have adopted asset purchase programs to inject money directly into the economy. The Fed led the way with quantitative easing in 2008 during the Great Recession. Central bankers now had a tool to directly change the shape of the yield curve and the old days of prolonged recessions were over: with enough QE could any economy be lifted out of recession?

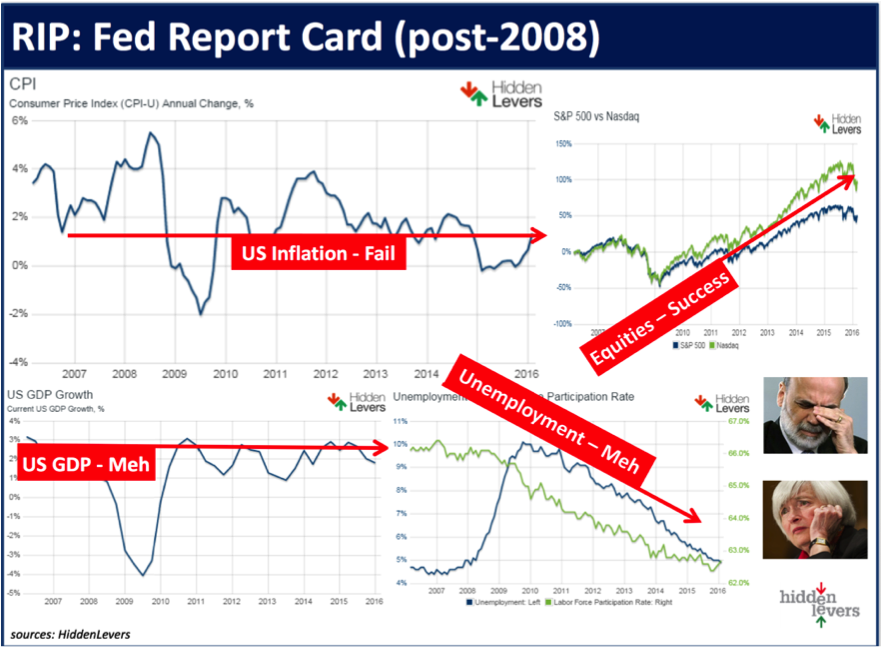

Actions from the Federal Reserve have lifted equity valuations, and tempered unemployment. Inflation and GDP growth have remained muted.

Negative Rates – The Implication

Fast forward 8 years and 3.5T in asset purchases: the Fed has finally started raising rates while other major economies have tried to replicate the Fed’s asset purchase program and many have even adopted negative short term rates to encourage spending.

HiddenLevers’ February War Room Webinar explored the implications of falling interest rates and introduced our Negative Rates scenario. Below we have summarized three potential outcomes - using HiddenLevers, advisors can stress test portfolios against these outcomes to assess and manage downside risk.

US Exceptionalism – The Good

QE has not been without its critics, but it has shown some signs of success. Domestic equities have been on a tear since 2008: US banks are recapitalized and the US economy is starting to see signs of inflation. This has put the US in an admirable position compared to its peers; a rate increase against the backdrop of a growing economy will help lender’s margins and reassure the broader economy that the US can live without a never ending supply of money. However, beneath the facade of a growing economy, the US faces a historically low labor force participation rate (62.90%) and inflation that is largely driven by increasing healthcare costs and rents – not paychecks.

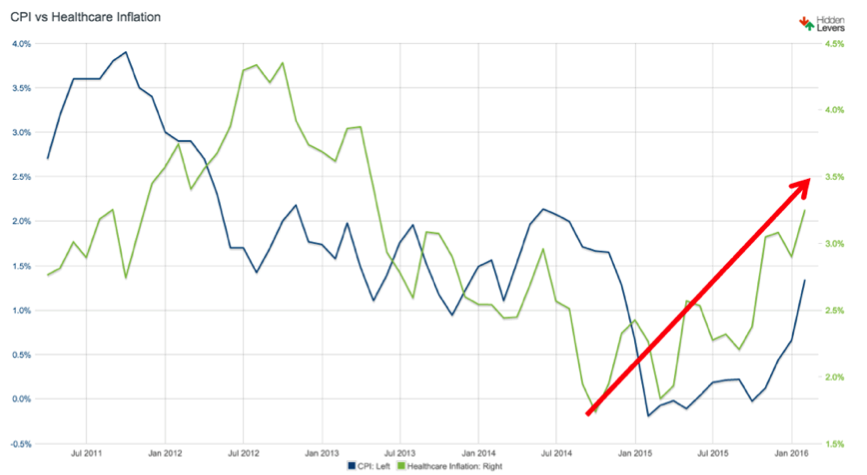

Inflation is coming from the wrong areas of the economy – rents and healthcare costs have moved in tandem with CPI.

Financials Struggle – The Bad

If inflation in the US does not continue on its path towards the Fed’s target of 2.0%, the Fed may be forced to delay its planned rate hikes. This would put pressure on US financial institutions who face razor thin lending margins. Delayed rate hikes could also act as a signal that the US economy is not as strong as the Fed previously thought – equity markets could move lower as market participants anticipate a bearish economy and a central bank that is increasingly impotent.

US Joins the Club – The Ugly

Increased automation, rock bottom commodity prices, and demographics shifts have pushed inflation to an all time low. The US has not been immune to these trends – wages in the US and across the globe have been stagnant since the financial crisis and jobs continue to be displaced by technology.

Are Helicopter Ben and Mother Yellen responsible for populist politicians? Disparate returns to capital and labor have increased inequality since the dawn of QE and low rates. (Photo collage: Chicago Tribune)

If deflation infects the US, the Fed will join its global counterparts in adopting an ultra aggressive monetary policy. The Fed may move rates negative in a Hail Mary effort to stoke demand. Unfortunately, with $1.2 trillion paper dollars currently in circulation, US savers are likely to keep money under their mattresses rather than in banks that charge them to deposit savings. Further, unfunded liabilities will balloon as pensions apply a lower discount rate to future liabilities. This outcome would be negative for equity markets and would bring the US into a mild recession as deflation overwhelms the Fed and the US joins its negative rate cousins.Are Helicopter Ben and Mother Yellen responsible for populist politicians? Disparate returns to capital and labor have increased inequality since the dawn of QE and low rates. (Photo collage: Chicago Tribune)

Are Negative Rates the New Black?

A negative rate policy in the US would be an unprecedented move and would signal the increasing irrelevance of central banks and their ability to combat deflation. Regardless of the Fed’s actions, advisors and portfolio managers should use stress testing to determine how their portfolios will perform in the context of multiple monetary regimes and identify hedges to volatility in the US and abroad.

Advisors can stress test a portfolio in the context of these outcomes by clicking this link.