India: 2016-17 Union Budget - A Budget for the Real Economy

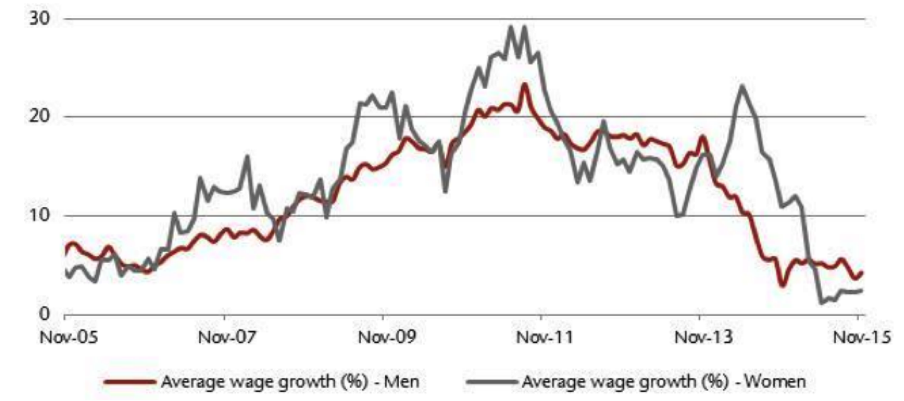

India’s Finance Minister, Mr. Arun Jaitley presented the 2016-17 Union Budget yesterday where he chose macro stability over short term growth tactics, earning credibility on fiscal discipline and empowering the bottom of the pyramid. The budget clearly outlined the government thrust on the rural economy while taxing urban and the top of the pyramid consumption. India’s rural economy has been going through a rough patch on account of two successive poor monsoons, lower rural wage allocation by the Government of India (GoI) through the Mahatma Gandhi National Rural Employment Guarantee Act (MNREGA) and soft commodity prices. MNREGA is the world’s largest social security and public works programme in the world and as the name suggests, works towards enhancing livelihood security in rural areas by providing at least 100 days of wage employment in a financial year to every household whose adult members volunteer to do unskilled manual work. The scheme has cumulatively spent Rs.3.2tn generating 2 billion man days of work till date. However, MNREGA spending has been low in the last 3 years and rural wage growth is at decadal lows. Stress in the India’s rural economy has coincided with lower allocation to MNREGA The central government has taken cognizance of the stress in the rural economy and the budget carried the highest ever allocation to MNREGA. Most importantly, there are visible efforts to spend more effectively; allocation to the agriculture sector has increased while thrust is on skill development and job creation.

Rural wage growth remains near decadal lows

Source: Jefferies

This budget was about credibility and character, presented amidst heightened global volatility and economic upheaval. China has been doing its own Yin & Yang which the global investor community is at a loss to decipher. The EU and Japanese central banks continue to print money to extract some small juice of growth but have failed miserably. Even the US after having raised rates sure footedly, is now giving mixed signals on the trajectory and pace of monetary policy. And here is India, facing growth issues, and historically prone to wilting under pressure and relaxing fiscal discipline standards at the drop of a hat. NOT THIS TIME folks, not this time! This budget showed spine and chose to stick to the fiscal deficit target of 3.5% for the coming financial year. When the entire world is talking about stimulus spend and QE, it takes character to talk about tight capital expenditure. Building trust in this fragile global environment will stand India in good stead for years to come.

This budget showed that the government is sticking to its initial disposition of clampdown on black money, subsidy rationalization and push for job creation. Various estimates have put the black economy at par with and even higher than the real economy. The thrust on bringing back black money into productive use in the real economy can rejuvenate the economy and put us back in growth trajectory while simultaneously keeping a lid on inflation.

Simplification and rationalizing taxes was another aspect of this budget and coupled with the thrust on black money is expected to bear fruit over a longer time. Mr. Jaitley has committed to providing a stable and predictable taxation regime and has proposed structural changes in the taxation framework to ease payment of taxes. Some amount of discretion in penalty for tax offences have been reduced moving the system towards transparency. The budget focused on process simplification and speeding clearances promoting small and medium business and supporting entrepreneurs.

The fiscal arithmetic of this budget is more credible with conservative tax projections albeit being optimistic on asset sales. Gross tax revenues are budgeted to rise by roughly 11.7% which is conservative. The budget has assumed roughly 11% growth in nominal GDP in FY17 which is reasonable. On the other hand, proceeds from telecom spectrum auction budgeted at Rs.990 billion looks aggressive and will be critical to the government’s fiscal arithmetic. Having said that, market conditions will play a key role in asset sales but lower tax assumptions suggest that overall revenue is achievable.

Adherence to original fiscal consolidation plan and lower than expected borrowings by the central government is good for fixed income segment. It may be noted that in the previous policy, India’s central bank, the Reserve Bank of India (RBI), while maintaining the accommodative stance, had stated that it will wait for the forthcoming budget, for further monetary easing. And of course, with budget delivering what RBI governor Dr. Rajan hoped for in Davos (fiscal rectitude) earlier this year, a small rate cut can’t be far away. With the government adhering the fiscal rectitude, the RBI can be expected to follow up with a rate cut to the extent of 25-50bps. The bond market has already rallied in anticipating a rate cut by RBI with yields on the 10 year benchmark bond rallying by 12-15bps.

Mr. Jaitley has delivered a good strategic and mature budget during testing times. Given the strategic nature of this budget, the benefits will take time to accrue and there might be some short term squeeze on account of absence of any major big bang spending. So, while the budget is structurally positive in medium term, limited room to spend and a tight fiscal stance will act as a dampener for capital markets.

On the other hand, introduction of the Monetary Policy Committee should modernize central banking and other proposed reforms in the areas of infrastructure, subsidies and agriculture are steps in the right direction.

Disclaimer: The views expressed are of Tata Asset Management Ltd. and are in no way trying to predict the markets or to time them. The views expressed are for information purpose only and do not construe to be any investment, legal or taxation advice. Any action taken by you on the basis of the information contained herein is your responsibility alone and Tata Asset Management will not be liable in any manner for the consequences of such action taken by you. Please consult your Financial/Investment Adviser before investing. The views expressed may not reflect in the scheme portfolios of Tata Mutual Fund.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.