Conviction in Volatile Markets: The Value of Loans Across the Credit Cycle

SUMMARY

- The case for loans as a strategic fixed-income allocation has been proven across many credit cycles.

- Because of consistently disciplined underwriting standards with a significant margin of safety, loans have returned more than 99% of principal since 2001. Over that period, loans have returned about 500 basis points (bps) of annual income, with less than 100 bps of credit losses.

- We see compelling, high-conviction opportunities in today’s deeply discounted loan prices. Our analyses build on a foundation of facts that can be readily confirmed with transparent financial information.

- Thoughtful risk minimization has been key to successful loan investing, based on professional expertise and fundamental, bottom-up analysis.

The strategic case

The fundamental case for floating-rate loans as a strategic fixed-income allocation rests on four basic characteristics:

- Near-zero duration, thanks to the floating-rate feature, with minimal exposure to interest-rate risk and low – and often negative – correlation with traditional fixed-income sectors.

- Senior/secured positioning in the capital structure – a layer of protection that is unique in the corporate fixed-income market. The loan amount is typically covered 2x by the issuer’s enterprise value.

- Attractive yields that were second only to high-yield bonds, among U.S. fixed-income sectors (as of December 31, 2015).

- Facts confirmable with public financial information – loan-to-value is readily verified through fundamental financial analysis.

In 2015, “risk-off” sentiment was the dominant force in the credit markets. Worries included slower global growth, evidenced by China, weak commodity prices, stock market volatility and uncertainty over the U.S. Federal Reserve. Loans (and high-yield bonds) came under significant selling pressure primarily from retail investors, which helped push prices down and produce a total return for the year of -0.69% on the S&P/LSTA Leveraged Loan Index (the Index). This sentiment continued in early 2016.

Does this kind of volatility undermine the case for floating-rate loans? We argue to the contrary: Lower prices create the opportunity to build on a strategic allocation that seeks dependable income and the diversification benefits of the asset class.

About 97% of loans have returned their principal without defaults since 2001. To a large degree, this track record stems from time-tested underwriting standards – a legacy of the sector’s banking roots – and manager due diligence.1 When ultimate recoveries are accounted for in cases of default, principal returned increases to more than 99% over that period.

As loan investment managers, we believe that disciplined underwriting standards and sound fundamental analysis allow high-conviction investing in volatile markets. This paper outlines how such bedrock principles have served investors well across a number of credit cycles, and why the value in today’s market is so compelling.

1Based on average trailing 12-month default rate of 3.2% on the S&P/LSTA Leveraged Loan Index from January 2001 through December 2015, according to S&P Capital IQ/LCD.

Retail tail wagging

At the end of 2015, the price of the S&P/LSTA Leveraged Loan Index (the Index) was 91.3 – the cheapest it has been since September 2011, with further declines in early 2016. Because secondary loan market prices are typically set at the margin, based on demand for loans or cash on a given day, retail flows have become an outsized factor in the pricing of loans, even though mutual funds comprise just a little over one-fifth of the market in terms of assets.

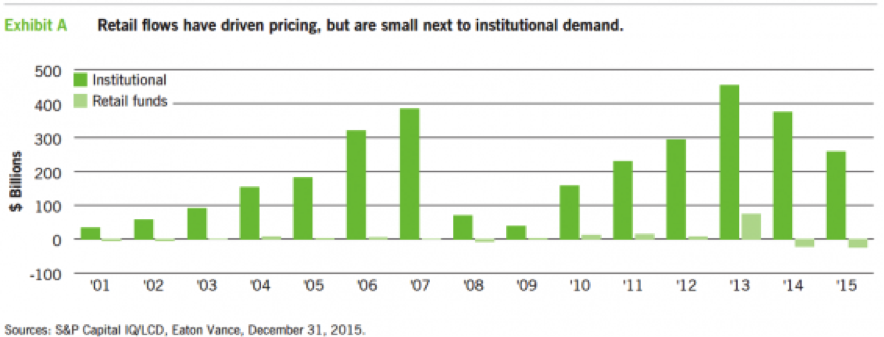

In 2015, retail investors were responsible, by and large, for all of the net outflows. After pouring $75 billion into the sector in 2013, retail investors pulled out $23 billion in 2014 and $26 billion in 2015. Institutional demand was a positive $258 billion – down from the prior two years, but still significantly higher than the average since 2001. Exhibit A shows how retail activity is dwarfed by institutional demand. In terms of pricing, it is the retail tail wagging the dog.

Fund managers who need to liquidate to meet redemptions will usually sell the more highly liquid loans first. As a result, loan prices of larger, more “on-the-run” issuers can get pushed down below what we consider to be fair value. As we will detail later, many quality names, in our view, have been swept up in the selling pressure. Human nature is to retreat amid falling prices, particularly when facts are hard to discern. Facts can be murky in so many sectors: emerging markets, foreign currency, Dutch municipal bonds, to name a few. We believe facts are much more transparent in senior/secured corporate debt, allowing for much higher conviction. The difference with loans is their readily verified (with publicly available information) margin of safety – one that stems from being senior and secured by assets and the durability of U.S. corporate enterprise value.

Next we examine what the discount on loans implies for potential future return.

Parsing pricing

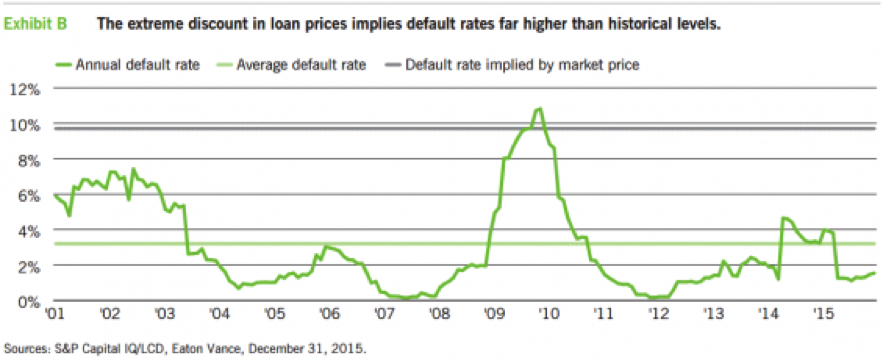

Loans are par instruments – absent defaults, investors are paid back 100 cents on the dollar. The price of 91.3 on the Index on December 31, 2015, indicates that the market is assuming credit losses from defaults to be 8.7 percentage points – or 2.9% per year over a three-year loan life (the average loan life Eaton Vance has experienced over 20 years). We emphasize “losses” to make it clear that the 2.9% figure is not the default rate, but what the market is expecting after recoveries.

Loans are senior in the capital structure and typically secured by all assets. Moreover, loans typically are sized at about 30% of enterprise value, meaning that there is an initial comfortable collateral cushion of 2x the par amount. As a result, recoveries from defaulted issuers over 20 years have averaged 70%, according to Eaton Vance’s experience – comparable to industry-wide levels reported by S&P Capital IQ/LCD. If we then view the 2.9% market expectation for credit losses as the remainder after 70% recoveries, the implied default rate becomes 9.7%.

To put that in perspective, the average annual default rate, over the past 15 years, including the 2008 financial crisis, has been just 3.2%. Exhibit B shows the large disparity between historical default rates and what is implied by the market price of loans. Note that the 9.7% default rate is an annual figure over the three-year expected life of the loan. Cumulatively, it is a prediction of defaults of almost 30% in three years. By comparison, at the height of the financial crisis in 2009-2010, the default rate stayed over 8% for less than 12 months.

Potential returns based on recent prices

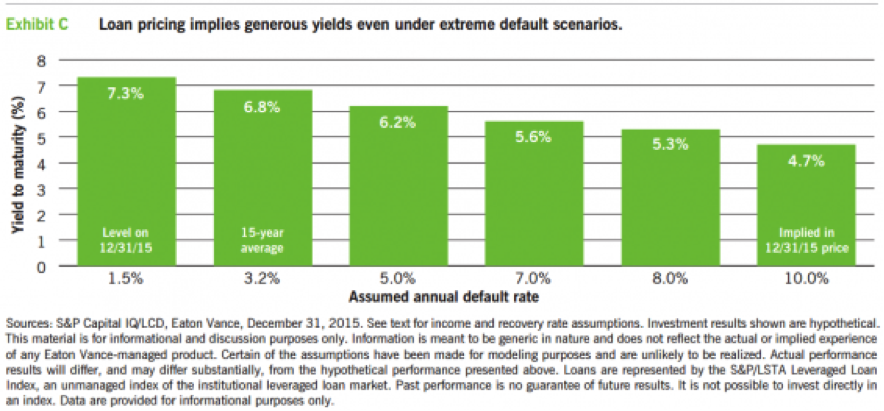

The clearest way to illustrate the value in today’s loan pricing is to look at hypothetical return scenarios under various default assumptions, like the ones we have just discussed. The yield-to-maturity (YTM) return scenarios in Exhibit C are based on the coupon level of 4.4% on the Index on December 31, 2015, and assume a three-year loan life and 70% recovery rate.

Assumed default rates range from the current level of 1.5% to 10.0% – just 30 bps higher than the 9.7% default rate implied by the 91.3 price on December 31, 2015. If default rates stay where they are today, the YTM is 7.3%. If they triple to 5%, the YTM is still 6.2%. If defaults soar to the 10% level touched once briefly during the financial crisis, the YTM of 4.7% is roughly what the coupon pays – a yield higher than all other fixed-income sectors, except high-yield bonds, as of December 31, 2015. It’s fair to say that these scenarios demonstrate the extraordinary “value cushion” represented by recent loan pricing.

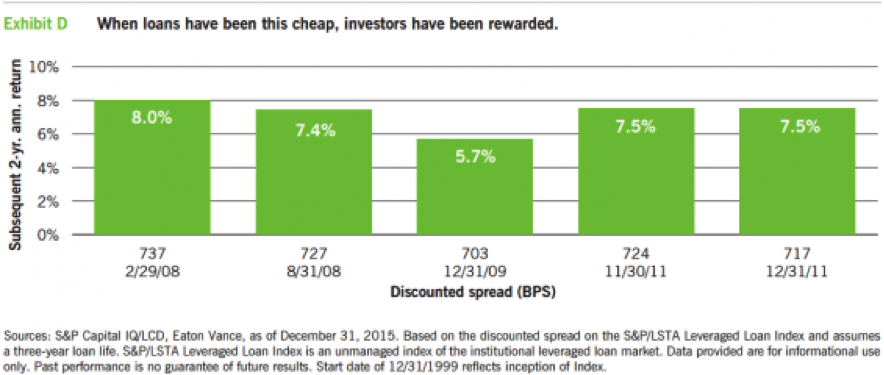

To test the validity of the hypothetical scenarios in Exhibit C, we looked back through loan pricing since 1999 to see how loans performed in the years following occasions when they were approximately as “cheap” as they were on December 31, 2015. We looked at the discounted spread, which captures both income and price information, to ensure “apples-to-apples” comparisons between periods.

In Exhibit D, each bar represents a time when the discounted spread on loans was higher or lower than the December 31 level of 714 bps by no more than 30 bps. Annualized total returns for the two subsequent years were between 5.7% and 8.0% – comparable to the scenarios in Exhibit C.

Some caveats must be kept in mind – we can’t predict exactly when rebounds will occur or to what extent. For example, note that the one-year return following February 2008 during the financial crisis was negative. However, the rebound in the second following year, after February 2009, would have resulted in a 2-year 8.0% annual return as shown in Exhibit D.

Recoveries seen as staying strong

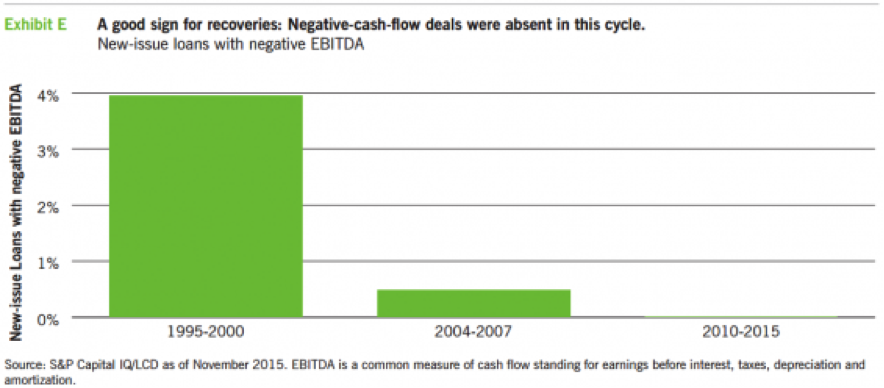

Given the importance of the recovery rate in determining net credit losses, it is worthwhile to consider whether future recoveries are likely to be at the same high level as the past. One recent study found that as long as a company has positive cash flow at the time of issuance – something uniformly true of recent vintage loans – a recovery is likely to be strong. A November 2015 study by Steve Miller, managing director of S&P Capital IQ/LCD, examined 410 institutional term loans that defaulted between 1998 and 2015, based on LCD’s database. Miller found that unlike positive cash flow, fundamentals such as coverage ratio, leverage and other measures associated with default probability were less useful in predicting ultimate recoveries in the 1998–2015 sample.

Miller noted that loans originated in 1995-2000 and 2004-2007 (ahead of subsequent default cycles), sometimes funded land development or telecom buildouts – ventures without any cash flow. As Exhibit E shows, the negative-cash-flow deal never resurfaced in this cycle. According to Miller, that bodes well for future recoveries. Most managers, he added, expect average recovery rates to be similar to those of the past, subject to “small movement” in either direction, depending on the severity of the downturn that brings on the next default cycle.

Searching for value

Regardless of where the market may be in the credit cycle, Eaton Vance believes that risk minimization is key to successful loan investing. Our focus is on building systematically risk-weighted portfolios with the goal of high income and preservation of capital, using bottom-up, fundamental analysis from four perspectives:

- Qualitative – Industry outlook, market position, scale management.

- Quantitative – Operating performance and financials, leverage, free cash flow, ability to repay debt.

- Structural – Seniority, security, collateral.

- Relative value – Market technicals, pricing/structure, comparative risk/return.

Applying fundamental analysis to drill down beneath the Index price of 91.3 illustrates the extent to which the sell-off in loans appears overdone. As of February 1, 2016, the great majority of the market – about 85% – was trading above 85, with an average price of 97. Of the hard-hit remaining 15%, 6% are in the energy/commodity sectors: iron ore companies (1% of the market, trading at 67); oil and gas companies (4% of the market, trading at 52); and coal companies (1% of the market, trading at 36).

That leaves 9% (of the hard-hit 15%) comprising about 40 noncommodity-related issuers, in diverse sectors, that trade at an average of about 70. Based on our fundamental analysis, only two of these companies are on our watch list – most, in our view, will ultimately be “par loans.” But if we again apply the arithmetic of defaults and 70% recoveries, the price of 70 implies that 100% of these issuers will default over the next three years. The odds of this are infinitesimal – rarely has the discrepancy between fundamental analysis and market prices been this big. Opportunity knocks.

Loans as a valuable – and durable – strategic allocation

We believe that taken as a whole, loan issuers are fundamentally sound as we advance in this protracted recovery from the Great Recession. According to S&P/LCD statistics, cash flow is still growing, albeit at a slower rate than a few years ago. Leverage is on par with historical averages, while interest coverage is 40% higher than historical average. We anticipate a modest increase in default rates, but as Exhibit C shows, today’s pricing structure implies generous yields even if default rates grow.

Such views can be readily confirmed in loan financial statements. Our analyses are rooted in fundamental facts readily available to all investors, including revenue scale, profitability, interest coverage, durability of the enterprise, its value and coverage of secured debt. Building on these basics helps create conviction in volatile markets.

As a strategic investment, the appeal of floating-rate loans can persist across the credit cycle. When the cycle weakens, seniority and collateral help protect investors; when it strengthens, loans have the potential to participate in two ways: price appreciation and yields that adjust with rising rates. With professional expertise and due diligence, we believe that loans have proven to be a valuable – and durable – strategic allocation. In today’s market, loans also appear to offer great value -- more than we have seen in a long time.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss. Elements of this commentary include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risk and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown, such as municipal and investment-grade bonds, carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum.

Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable.

The views expressed in this Insight are those of the author and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forwardlooking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

© 2016 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |