Have Currencies Around the World Overshot Fair Value?

We think there’s a case to be made that most emergingmarket currencies, along with some developed-market currencies, have seriously overshot in their weakness against the U.S. dollar. A reversal of this trend would be very positive for emerging-market investors. Moreover, we believe such a reversal of the five-year trend may have already started or may be close at hand.

DOLLAR TOO HIGH, EMERGING-MARKET CURRENCIES TOO LOW

Many factors, including strong geopolitical forces, have led to the dollar being excessively valued relative to other currencies—especially emerging-market currencies. We also find it interesting that unlike central bankers in Europe and Japan, the U.S. Federal Reserve (Fed) has not forced short-term interest rates into negative territory. Such a situation—in which there’s actually a fee to keep money on deposit at a bank—indicates an extreme effort to stimulate an economy, but also has a tendency to produce currency weakness.

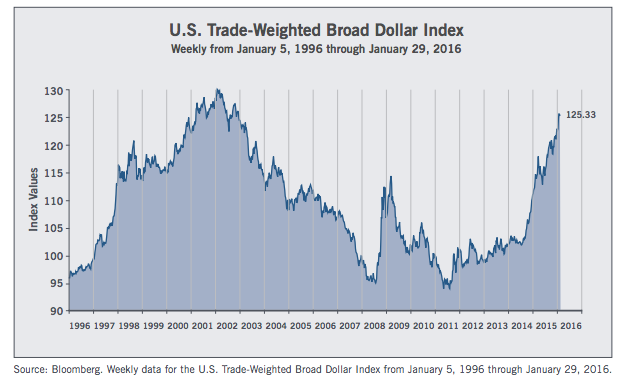

If emerging-market currencies reverse course and strengthen against the U.S. dollar, initially the changes could be very sharp until a new trend is established. Looking at the U.S. Trade-Weighted Broad Dollar Index chart on page 2 (where in January 1997 the Index equaled 100), we can see that the level on January 29, 2016 of around 125 for the greenback is at the upper end of the range since 1996, with the highest level having been at about 130 in 2002. The dollar has now surpassed the levels it held during the depths of the Global Financial Crisis in late 2008 and early 2009.

OUTLOOK BRIGHTENS FOR EMERGING MARKETS

During the end of 2015 and the beginning of 2016, the outlook for emerging markets had been clouded by investor fears and short-term volatility. Stocks globally were getting hit hard, and concerns regarding the Chinese economy and the country’s jittery currency had become magnified. The Shanghai and Shenzhen stock markets had become so speculative that they resembled the casinos of Macau. In addition, the Shanghai-Hong Kong Stock Connect had shown a worrying “disconnect”—with valuations in Shanghai far exceeding those in Hong Kong. And even though stocks in Shanghai and Shenzhen are mostly owned by mainland investors, gyrations in these markets still hit global sentiment. But more recently, we’re seeing signs of an appropriate decoupling of mainland Chinese stock markets from those in the rest of the world.

Over the last few weeks, we’ve had more anecdotal evidence that commodity currencies—the currencies of countries like Australia and Canada that depend heavily on the export of certain raw materials for their income—and emerging-market currencies have overshot and are “cheap” relative to the U.S. dollar.

There’s nothing like having a restaurant meal in a foreign country to get a relative sense of currency value. In recent trips to Canada and Mexico, our research team noted how inexpensive the meals were. A meal in Canada is nominally the same price as one in the U.S. But since the Canadian dollar (CAD) is about $1.40 to the U.S. dollar (USD), a dinner in Canada at CAD$80 in fact cost USD$57.

More and more, Canadians have been choosing to bypass the U.S. and spend their vacations in Mexico. Similarly, tourists have been flocking to Japan and Australia, where the currencies are also cheap. Compared to the U.S. on a currency basis, these destinations seem attractively priced—especially if you’re from Hong Kong or China, where the currencies had historically been pegged to the U.S. dollar.

Among emerging-market currencies, we find it perplexing that the Mexican peso and the Philippine peso have become so cheap. Mexico and the Philippines are not overly dependent on commodity exports. As a result, we would not have expected these currencies to experience such significant declines in the face of the commodities rout. But if sentiment toward emerging markets improves even modestly, the Mexican peso and the Philippine peso could experience significant rebounds.

EMERGING-MARKET CURRENCIES DECLINED FOR ALMOST FIVE YEARS

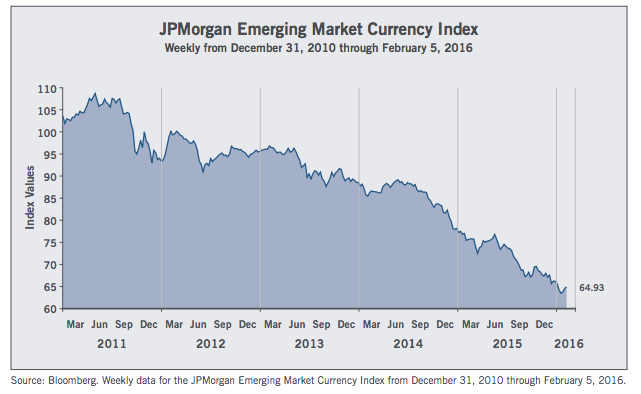

If we look at the JPMorgan Emerging Market Currency Index chart on page 3, we can see that a basket of emerging-market currencies started falling against the U.S. dollar in 2011—for a total decline of about -40%. So the bear market in emerging-market currencies had remained in force for almost five years.

With global growth slowing and geopolitical risks rising, the attraction of the greenback as a safe-haven currency went up in the last several years. More recently, that safe-haven position was enhanced by the U.S. Fed signaling continued interest-rate increases and the Chinese government threatening to devalue the yuan. Conversely, commodity-oriented currencies such as the Australian dollar and the Canadian dollar lost their safe-haven status—along with declines in emerging-market currencies, many (although not all) of which are commoditydependent. So we conclude that weak commodity prices further encouraged the movement of capital to U.S. dollar-denominated assets.

All in all, the U.S. dollar was in a powerful upward trend for the last several years, backed by some significant convergent forces. Likewise, the perennially steadfast Swiss franc was especially strong—to the point that market forces (rather than central bankers) even drove longerterm interest rates to negative levels, a situation we hope does not occur in the United States.

CAPITAL OUTFLOWS MADE THE SITUATION WORSE

In the case of emerging-market currencies, it’s likely that the recent undervaluation was magnified by significant outflows from emerging-market bonds and stocks. So what was the scope of asset outflows from emerging markets in 2015? According to an article in the January 27th issue of the Financial Times, “The Institute of International Finance, an industry group, estimates that total net capital outflows from EMs amounted to $735bn last year, the first year of net outflows since 1988.” These outflows were so strong that the International Monetary Fund’s orthodoxy of open capital accounts is being reconsidered.

On the bond side, according to the Financial Times, “Investors are deserting emerging market bonds at the fastest rate on record, withdrawing more money than they did at the height of the global financial crisis.” Stock outflows from emerging markets in 2015 were also huge, compounded by a number of factors. For example, we estimate that tens of billions of dollars were withdrawn from emerging markets by sovereign wealth funds in the second half of 2015. But we now believe most of the selling by these funds has already taken place.

There’s an important point about asset outflows from emerging markets: In general, investors taking assets out of emerging markets haven’t discriminated among countries. Asset allocation for both emerging-market bonds and stocks has been largely indexed, unlike for developed markets. For example, developed-market investors have tended to proactively decide on their German allocation or their Japanese allocation—rather than invest in countries as a group.

Emerging markets, on the other hand, have often constituted a “basket trade” for investors. So if the basket was sold because China’s prospects looked weak, then all the emerging-market countries in that basket would be sold—including those with better prospects. This tendency partly explains why emerging-market stocks and countries have sold off for reasons that are not specific to them.

There have also been reflexive effects, however. For example, if Mexico was sold because it was in the basket, then the Mexican central bank might end up raising interest rates to defend the country’s currency, which of course would have knock-on macro implications. This scenario illustrates the slower-burn contagion that has been brought about by the indexing-induced linkages mentioned above.

PURCHASING-POWER PARITY

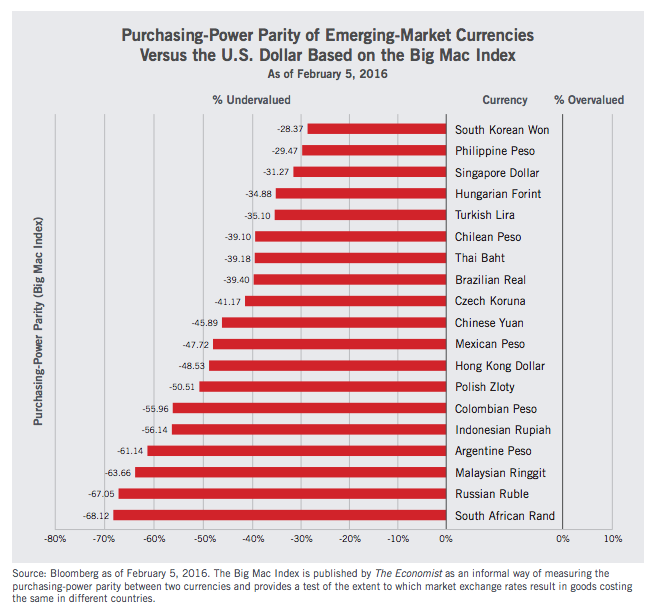

Resulting from the conditions described in this commentary, many emerging-market bonds, stocks and currencies are now undervalued in our view. Regarding currencies, the “Big Mac Index” is a measure popularized by the The Economist to show the relative overvaluation or undervaluation of various currencies based on the concept of purchasing-power parity. The Index uses a consistent mix of goods and services (in this case, those involved in producing a McDonald’s hamburger) and current currency exchange rates to determine the “correct” level. By this measure, the chart above shows the extent to which emerging-market currencies are “undervalued” relative to the U.S. dollar.

It’s important to note, however, that this chart does not describe how currency values have changed recently and how various currencies match up relative to a benchmark other than the U.S. dollar. For example, we believe the Chinese yuan is significantly overvalued on the world stage despite the yuan’s implied undervaluation based on the Big Mac Index.

FIVE-FACTOR MODEL: EMERGING MARKETS ARE NOT CREATED EQUAL

We can classify countries based on a simplistic fivefactor model in which they get “dinged” on “yes” answers to the following questions: (1) Is the country an emerging market? (2) Does the country have a commodity-oriented currency? (3) Is the country being impacted by difficult geopolitics? (4) Is the country being impacted by difficult domestic politics? (5) Is the country contending with a weak macro environment? Of course, each of these factors can impact the others.

Based on this model, we give Russia four dings (emerging market, commodity currency, impacted by difficult geopolitics and a weak macro environment). But Russia’s domestic politics are autocratically stable. We also give Brazil four dings. In a geopolitical sense, Brazil appears to be alright. But the country’s domestic political situation is unstable. And the country’s three other dings are obvious. Russia and Brazil are the extreme cases. Both countries have political problems. Both are emerging markets. Both have commodity currencies. And both are contending with weak macro environments.

The Philippines, on the other hand, gets only one ding from us. Although the Philippine peso has weakened along with other emerging-market currencies, forecasts are for the Philippines to produce 6% gross domestic product (GDP) growth in 2016. In addition, the country has a current account surplus of 3.4%, a fiscal budget deficit of only -0.8% and consumer price inflation of a mere 2.7%. So we believe the Philippines was simply subject to the contagion risks driven by persistent outflows of assets from emerging markets overall. Unfortunately, those outflows failed to distinguish among the “good,” the “bad” and the truly “ugly” emerging-market countries.

DOLLAR STRENGTH MAY HAVE PEAKED

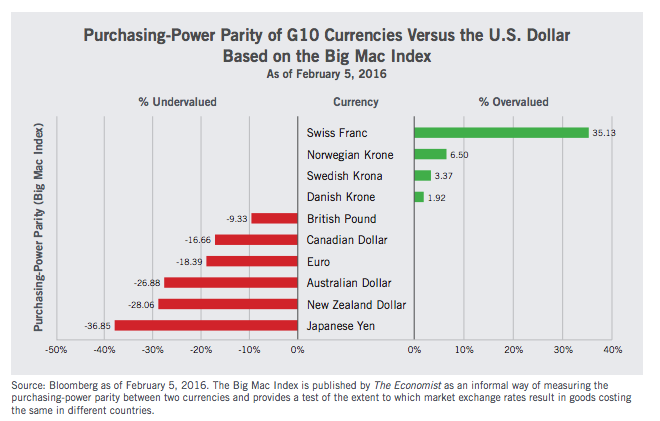

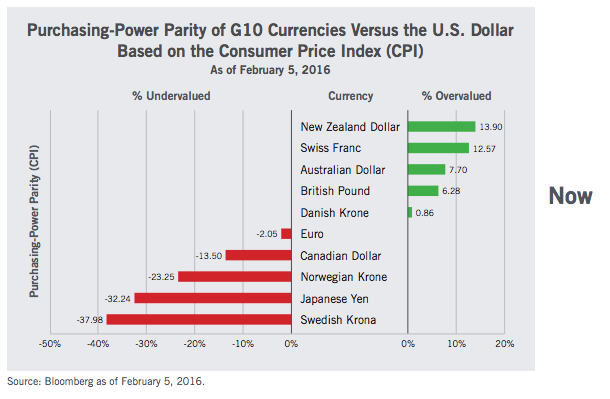

Part of what we’ve been talking about had to do with the strength of the U.S. dollar, not just the weakness of emerging-market currencies (i.e., the currency-valuation mismatch was largely influenced by too much global capital flowing into U.S. dollar-denominated assets). We can find evidence of this by comparing the greenback to other G10 currencies using the Big Mac Index. Note that in the chart above, most of the commodity-oriented currencies look undervalued.

Another way to evaluate currencies is based on the purchasing-power parity of the consumer price index (CPI), which is illustrated in the chart on page 6. While there are significant differences between the Big Mac and CPI methodologies, the Japanese yen looks very undervalued based on both methodologies.

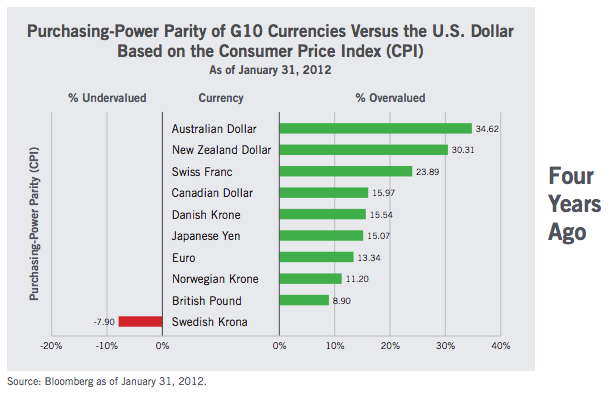

While official CPI figures are often criticized for being politically influenced and for underreporting inflation, it’s interesting to compare the data from four years ago for the same countries. The second chart on page 6 shows the data from January 31, 2012. Back then, almost all of the G10 currencies appeared overvalued relative to the U.S. dollar, a much different picture from what we see today.

DRAWING CONCLUSIONS

What does all this mean? Asset prices and currency values can show momentum (positive or negative) for longer than expected. It’s possible that influences such as geopolitics, for example, can extend the strength of the U.S. dollar for longer than a purchasing-power-parity model or economic data would justify. But we believe macro forces have pushed the dollar up too far even at today’s interest-rate levels. And if the U.S. joins Europe and Japan with negative rates, the dollar is even more likely to lose some of its recent strength.

Regardless of slight movements in U.S. interest rates, many emerging-market companies appear reasonably valued. Emerging markets have different demographics and the need for capital in these countries (even with their reduced GDP growth) may offer higher yields compared to what’s available in developed markets. Moreover, central banks in emerging markets have more scope to bring down interest rates with disinflation. If we see some strength in currency values and some stabilization in commodity prices, the emerging-market universe should look more attractive again.

Part of that attraction could come from investors getting used to a “new normal” of slower economic growth in China—but also from higher-quality, more-sustainable growth. Another part could come from a further decoupling of world stock markets from those in Shanghai and Shenzhen on China’s mainland. Finally, emerging-market equities may get a boost from the recognition that economic growth is weaker in the United States than in many emerging markets and that the U.S. Fed may delay any previously proposed rate increases.

Our view is that many emerging-market currencies are poised to appreciate 10% to 15%, and at that point they would still be undervalued. We also believe that currency appreciation is likely to be accompanied by rising stock prices in emerging markets and reversal of the capital outflows. Such a scenario can happen fast. And while no one knows if 2016 will be the year that emerging markets reverse course, we think it’s a real possibility.

CHINA MAY GO ITS OWN WAY

What about China? How can the emerging-market indices do well if Chinese stocks—which comprise the largest country component of the MSCI Emerging Markets Index—are still excessively valued and are not poised to rise? We have two observations in this regard. First, Chinese stocks seem to have recently decoupled somewhat from other emerging-market equities (and from developed-market equities for that matter). Second, the practice of indexing emerging markets going forward may be a greater disadvantage if China is fundamentally unattractive, as we believe it is—somewhat akin to Japan in the 1990s when many global portfolio managers had secular underweights in Japanese stocks.

Another currency-related point is that we believe the evidence suggests the possibility of devaluation of the Chinese yuan and the Hong Kong dollar, both of which had been pegged to the U.S. dollar. While most emergingmarket currencies are arguably poised to rise, we think the yuan and the Hong Kong dollar have room to fall.

PUTTING IT ALL TOGETHER: CURRENCY AND STOCK-PRICE ADJUSTMENTS

While determining “correct” prices for stocks is difficult enough, getting one’s arms around the “intrinsic” values of currencies is even more challenging. Measures like purchasing-power parity are relative to other currencies. Another way to understand a currency is to assess how much that currency has deviated from its mean value relative to another currency or basket of currencies over a given time period. For example, over the last 12 years (which includes the period before the Global Financial Crisis), the Indian rupee has periodically been above and below its mean value relative to the U.S. dollar. Currently, the rupee is about 2.3 standard deviations below its mean value, which is the largest deviation (positive or negative) that the rupee has had in 12 years. And deviations typically move back toward the mean over time.

We also see that the Mexican peso relative to the U.S. dollar is about 1.6 standard deviations below its 12-year mean value. For other emerging-market currencies, we see similar standard-deviation figures. As a result, we think the excessive valuation of the U.S. dollar compared to other currencies has moved to an extreme and may be showing signs of a possible reversion. Any reversion would be good for emerging markets’ purchasing power and for asset flows into these countries.

Regarding valuations, emerging-market stocks on average are trading at a ratio of about 1.3 times book value, which is close to the bargain level reached in 2008 during the Global Financial Crisis. So when we combine possible changes on the currency front with attractive valuations for emerging-market stocks, and then we also see signs of a bottoming process after five years of lackluster returns, we believe the upside potential for emerging-market investors is strong.