Six Questions on Emerging-Equity Turmoil

It’s been a terrible start to the year for emerging-market equities. But by maintaining perspective on long-term trends, investors can gain the comfort to stick with developing stocks, in our view.

Investors in emerging markets are understandably shaken. After three straight years of declines, the MSCI Emerging Markets Index tumbled by 8.4% in the first six weeks of 2016 in US-dollar terms. But as concerns about China, the Fed’s policy and commodity prices spur volatility, the following questions can provide context for the big picture.

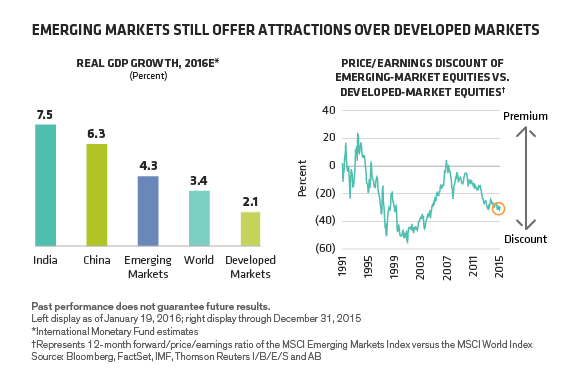

1. Why should I bother with emerging-market equities?

Economic growth in emerging markets is slowing. Yet even so, these economies are growing much faster than developed markets’ (Display, left). Emerging-equity valuations are depressed versus developed-market stocks (Display, right). And investors can find industries in emerging markets with powerful growth potential over the next 10–20 years, while these same industries are already mature and slow-growing in the developed world. For example, financial services, private education and private healthcare in many developing countries are rapidly growing from a very low base, driven by long-term social and economic change.

2. Should I avoid China completely?

Absolutely not. China is going through huge changes that are often misunderstood. The current economic slowdown is impacting traditional areas of growth, including the export, industrial and commodity sectors. However, domestic consumption is holding up relatively well and growth remains strong in new areas such as the Internet and private education. In some segments of the service sector, such as fast-food restaurants or car rental companies, penetration levels are still low and long-term growth opportunities are large.

The currency situation has clouded the outlook. But we think the government has the strategic incentives and powerful policy tools to avoid a sudden and sharp devaluation exceeding 10%; it would derail plans to shift the economy toward domestic consumption and could delay China’s transition to a developed market, in our view.

3. What about the Fed’s interest-rate hike?

There’s much less external debt in emerging markets than during the Asian crisis of 1997. So we think that a gradual Fed interest-rate hike will have a relatively small impact on growth in emerging markets. In addition, most investors have already positioned their portfolios in anticipation of Fed rate hikes. While cyclical growth will be affected, we generally expect structural growth—which is creating the best opportunities—to remain intact.

Of course, the Fed’s moves will affect money flows. Indeed, a sell-off of emerging-market bonds could lead to a spike in yields. And a further strengthening of the US dollar could trigger a run on currencies. Investors must be vigilant.

4. Are emerging markets more exposed to lower commodity prices?

Not necessarily. While commodity exporters like Russia are suffering, most Asian countries are net commodity importers. Countries that import commodities account for more than 65% of the MSCI Emerging Markets Index and benefit from low commodity prices, which have helped reduce inflation and interest rates in places like India and South Korea.

5. Which countries present the best opportunities today?

We believe bottom-up stockpicking should determine country positions—not the other way around. That said, we think India is attractive, as lower rates unlock opportunities in financial services and consumer durables. Indonesia’s economic improvements aren’t yet reflected in share prices. Peru tends to be beneath the radar, yet the country’s burgeoning financial sector is exciting. Beware of Brazil, where political and macroeconomic risk is too unpredictable to incorporate into fundamental stock analysis.

6. What’s the best way to approach emerging equities today?

Think about three things. First, invest in companies that can benefit from long-term structural growth trends, which can withstand short-term turbulence. Second, embrace volatility, which often creates opportunities in companies with strong fundamentals but mispriced stocks. Third, stay active. Investing in an emerging-market index will give you exposure to risky cyclical stocks and debt-laden companies that are vulnerable to rising rates. Active managers can steer away from trouble spots and toward companies capable of posting strong long-term returns in a recovery.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.