5 Myths About the Recent Decline in the Stock Markets

The financial news in early 2016 hasn’t been good. When we say the news hasn’t been good what we really mean is that the news media has been hyperbolic in their treatment of the weak market. Here are a few of the adjectives used to describe market activity: nightmarish, plunged, dive, rocked, plummeted. And this is just from a single article!1 Yes, we know the market is down and frankly we’re not happy about it. But…

Here’s a news flash: the world isn’t ending. Further, there is a lot of good news and some of the purported bad news is really good news. Below we debunk some myths that seem to be driving investor worries.

Myth Number 1: China’s Economy is a Disaster and Will Lead to a Global Economic Cataclysm

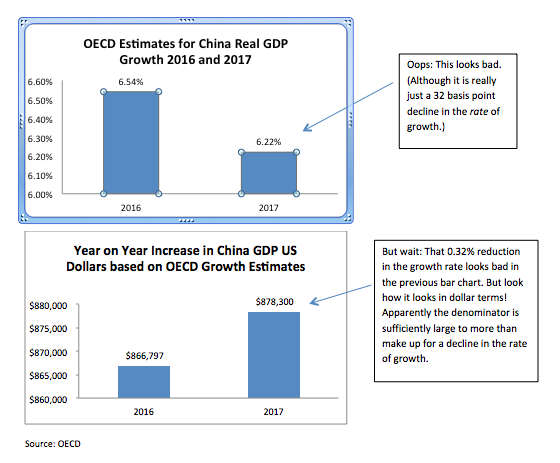

China’s economy is slowing, meaning its rate of growth is lower year over year. That is not a surprise and in fact is natural as a rapidly growing economy matures. We’ll examine the numbers in a minute, but let’s articulate one basic fact about the Chinese economy: it is among the fastest growing of any major economy in the world—only India is expected to grow faster.2 The Organization for Economic Co-operation and Development (OCED) is estimating China’s Gross Domestic Product (GDP) to grow by 6.54% in 2016 and 6.22% in 2017. The rate of growth is slowing, but the growth is still well above most other major economies. The US, for instance, is expected to grow by 2.5% in 2016.3 But measuring the slowing growth of the Chinese economy in percentage terms misses a vital point. In dollar terms the growth in the Chinese economy will be greater in 2017 than 2016. The growth in dollar terms in 2016 will be $866 billion. In 2017 the dollar amount of growth will be $878 billion. If you’re worried about the global economy it is the absolute dollar level of the Chinese growth that matters, not the percentage growth rate.

Myth Number 2: China’s Consumption of Oil is Declining

China’s oil demand is growing and continues to grow smartly. In 2015 China consumed 11.3 million barrels of oil per day, up 6.6% over 2014 (10.6 million barrels). For 2016, China is expected to consume 11.6 million barrels, an increase of 2.7%. The media often reports the consumption (particularly imports) of oil in dollar terms. Given that the price of oil has declined by 60%, the dollar amount of the oil imports will naturally be much lower. The Chinese consumer in particular has been consuming oil; in November 2015 gasoline demand was up 12% year to date. And this demand is expected to continue to grow rapidly as China vehicle sales continue to rise sharply. 2015 vehicle sales in China are estimated at 24.6 million units (of which 21.5 million are expected to be passenger vehicles).4 As a point of reference, the US set a record in 2015 with the sale of 17.5 million cars and light trucks.5

Myth Number 3: Global Oil Demand is Down

False again. World oil consumption continues to grow. The International Energy Agency (IEA) is estimating global oil consumption will grow by more than a million barrels per day year over year for 2015, 2016 and 2017.6 This rate of growth is consistent with the long term growth in oil demand. The details: In 2014 the world consumed 92.8 million barrels of oil per day. For 2015 that figure is 94.6 million barrels. The IEA estimate for 2016 is 95.8 million barrels, and we are estimating an additional gain of 1.2 million barrels in 2017. The average per day annual increase from 2000 to 2014 was just over one million barrels per day. Longer term, say from 1980 through 2014, the average annual increase in consumption was 0.8 million barrels.7

Myth Number 4: Low Oil Prices Are Bad for the Economy

This current belief is counter intuitive and empirically false. For the economy as a whole, declining oil prices are a boost to the economy as lower prices increases the profits of companies that consume oil and decreases consumer costs for transportation and heating. The US uses about 137 million gallons of gasoline per day8 with about 65% of that for personal use.9 From 2011 through 2014 the average price of gasoline was $3.56 per gallon.10 For 2015 the average was $2.52.11 That savings of $1.04 per gallon means an annual saving of $750 per household. In early 2016 the national average has dipped below $2.00 per gallon for regular and the simple average of all grades is $2.12 per gallon.12 At that price the savings is $1.44 per gallon which raises the per household savings to $1,039 per year.

Additionally, for home heating oil, the drop in oil prices means a savings of about $600 per household for families that use home heating oil for the winter season.13

The amount Americans save on gasoline and heating oil is significant and that savings can either be spent or saved. Either of these actions is beneficial for the economy, although spending shows up immediately as a contribution to GDP. So far, consumers have been more inclined to save this low oil price dividend rather than spend it; the savings rate for US consumers rose to 5.5% in November, up nearly a percent from a year earlier.14

Ok, but what about job losses and the drag on GDP in the energy sector? This is the gray lining to the silver cloud. But how big of a drag does the decline in oil represent? According to the Dallas Fed Economic Letter15 one-half of one percent of the total US work force is in the oil and gas industry. The oil and gas industry represents about 2% of US GDP.17 Clearly there will be some contraction here, but as a percentage of the national GDP and employment it will be insignificant.

Myth Number 5: The Yuan is in Serious Decline

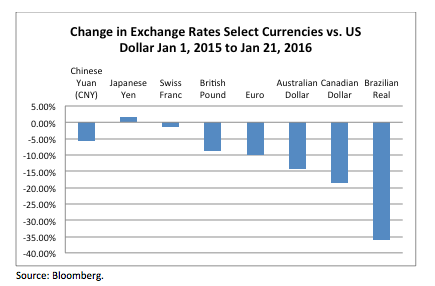

The media has seemingly appended the word plunge onto the word yuan. A Google search for the term “yuan plunge” produces 81,400 news articles.17 We argue that not only has the yuan not plunged, it is among the strongest currencies in the world. Here are the facts. From January 1, 2015 through January 21, 2016, the yuan (CNY) declined 5.69% against the dollar.18 Among the world’s major currencies, only the Japanese Yen (+1.77%), and the Swiss Franc (-1.31%) performed better relative to the US dollar over that period. The British pound (-8.71%), the Australian dollar (-14.39%), the Canadian dollar (-18.54%) and the Brazilian Real (-36.04%) all declined more against the US dollar over the period. Yes, the yuan lost value to the US dollar, but “plunged” seems a bit of an exaggeration. Note: most currency experts view the changes in the yuan, pound and euro as a result of a strong dollar rather than any particular weakness on the part of these currencies.

Further, in the first 21 days of the new year the yuan is down only 1.31% against the US dollar while the British pound is down 3.49%. If 1.31% is a plunge how are we to characterize 3.49%?

Our Take

So if the world isn’t going to heck in a handbasket then what is going on?

- The US economy is stronger than you think. The labor market should continue its very long and slow recovery. During this recovery there has been a lot of hand wringing about a lack of wage growth. Our long held belief is that wages would start to grow when the labor market reached a sufficient level of tightness that employers would be forced to raise wages. And indeed, in late January Walmart announced a wage increase for nearly 1.2 million workers.19 (Walmart is the largest private employer in the US.) To be clear, this isn’t going to rocket the economy into hyper growth, but it is a clear signal that things are improving for the labor force. The Wall Street Journal indicated that the raise was designed to “…combat a tighter labor market.”

- Americans are saving more. This is a bit of a double edge sword, as money saved is money not spent but one clear lesson for Americans that came out of the financial crisis is the need to save more and borrow less. We cited a 5.5% savings rate above, and frankly this isn’t a high number by international standards, but it is an improvement and that is a good thing. Money saved now can lead to money spent later and a more stable, stronger economy.

- The US is spending less on oil and importantly spending less for imported oil. While we are believers in free trade we prefer to spend less than more when purchasing commodities from overseas and we prefer, greatly prefer, not to send petro-dollars to countries that might be less than friendly with the US. In addition to benefiting consumers, as mentioned above, the decline in oil prices helps keep the trade deficit down.

- Despite their recent rise, interest rates are very low. While this may not necessarily be a good thing for savers, it is certainly a good thing for corporate profits in general and for borrowers. Many of us thought sub 4% (or even sub 3%) home mortgage rates disappeared with our parents’ mortgages and would never, ever recur. We understand general economic weakness is the reason behind the low rates but that doesn’t negate the benefit they provide.

- Inflation is low. Perhaps inflation is just over the horizon; and that argument is stronger given our argument about wage growth above. But let’s acknowledge that inflation was thought to be just over the horizon for much of the last decade. It hasn’t reappeared. Like low interest rates, this doesn’t benefit everyone equally. In fact it is the reverse of low interest rates as this benefits savers over borrowers. But those that lived through the 1970s and early 1980s will recognize inflation is a real drag on the economy as a whole and living in a low inflation world is an overall positive.

- The US is a creative/innovative juggernaut. We’re not the first to advance this argument and we won’t belabor it here. Our view is that technology and innovative thinking has led to our economy producing more with less than ever before.

We accept that some may wish to argue some of these points…maybe some will want to argue them all! But we believe on balance that the news media has a strong tendency to focus on the negative and to ignore the boring but important good news that is all around us. We don’t know what the stock market will do in the next week, month or year. But we do have an unshakable faith that the markets will do what they always do, which is fluctuate, wildly at times, but with a strong upward bias.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

This information is authorized for use when preceded or accompanied by a prospectus for the Guinness Atkinson Global Innovators Fund. The prospectus contains more complete information, including investment objectives, risks, charges and expenses related to an ongoing investment in The Fund. Please read the prospectus carefully before investing.

Mutual fund investing involves risk and loss of principal is possible. The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the market. In addition, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future or the anticipated acceleration of dividends could not occur. The Fund invests in foreign securities which will involve greater volatility and political, economic and currency risks and differences in accounting methods. This risk is greater in emerging markets. Medium- and small-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies.

Basis point is used to denote the percentage change in a financial instrument and is equal to 1/100th of 1%.

Distributed by Quasar Distributors, LLC

1 Article by KVDR.

2 The OECD is estimating 7% annual GDP growth rate for India.

3 Source: OECD.

4 Source: Statista.

5 Source: Wall Street Journal.

6 Source: International Energy Agency World Energy Outlook 2015 (released November 10, 2015). 2017 estimate is a Guinness Atkinson estimate.

7 Historical figures and averages (calculated) come from the BP Statistical Review of World Energy 2015 Workbook

8 Source: US Energy Information Administration.

9 Source: Energy Independence.

10 All grades of gasoline. This is the average of the annual averages for those years. Year by year: 2011: $3.57; 2012: $3.68; 2013: 3.57; 2014: $3.43. Source: US Energy Information Administration

11 IS Energy Information Administration; see footnote 2 for details.

12 Source: AAA.

13 Wall Street Journal December 10, 2015.

14 NBC News.

15 Published by the Federal Reserve Bank of Dallas, Newsletter dated April 2015

16 Source: Dallas Fed Newsletter April 9, 2015.

17 Total search results for this term are 738,000.

18 Currency exchange rates sourced from Bloomberg. Percentage change calculations by Guinness Atkinson.

19 Source: Wall Street Journal, January 21, 2016.