Outlook Summary

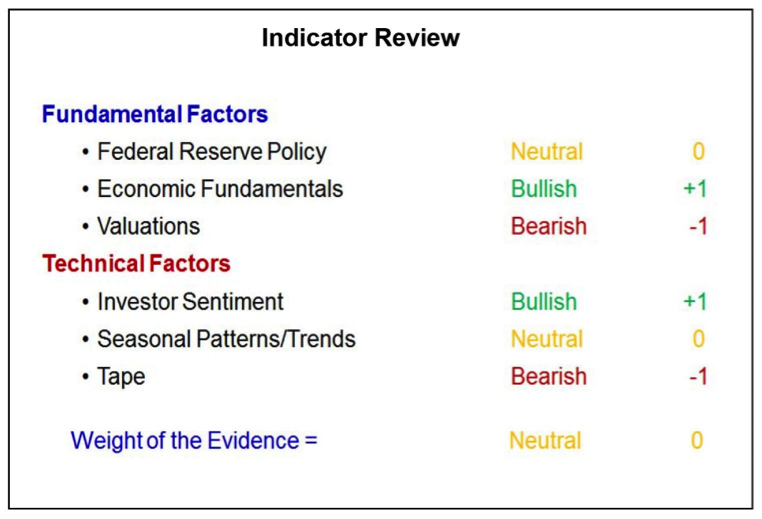

· Weight of the Evidence Neutral

· Valuation Excesses Have Not Been Relieved

· U.S. Large-Caps Showing Leadership

· Defensive Sectors Gaining Relative Strength

· Evidence of a Sustainable Low Still Lacking

2016 Already Offering a Rocky Ride

Highlights:

· Fed Policy, Election Season Fueling Volatility

· Economic Fundamentals Stable

· Investors Turn Pessimistic

· Broad Market Behavior Suggests Risks Still High

After several years of muted volatility, the January roller coaster in the stock market caught many investors off guard. Coming into the year, we thought 2016 held the potential to see an uptick in volatility, but had expected the usually strong seasonal tailwinds to delay significant weakness until after the first quarter. The S&P 500 was able to recover roughly half of the decline seen at its worst levels but still posted a 5% decline for the month.

We have pointed to four things to look for as evidence that a sustainable low for stocks is in place. From a longer-term perspective we would expect excessive valuations to be meaningfully relieved. Additionally, investor sentiment should show excessive pessimism, up-side momentum should replace down-side momentum, and breadth trends should show a meaningful expansion in rally participation. Of these, we do have investors turning fearful and downside momentum has been broken (although it is hard to say that upside momentum has emerged in its wake). Absent at present are significant improvements in valuation or breadth. As such, a cautious approach (echoed by a turn to neutral by the weight of the evidence) remains appropriate.

Graphic 1. Indicator Review

While stock market volatility has increased, there is little evidence that recession risks have significantly increased. This decreases the risk of a 2008-style melt down in the financial markets. Not over-correcting in response to near-term developments, but maintaining (or returning to) a disciplined approach to asset allocation remains the best strategy for most investors.

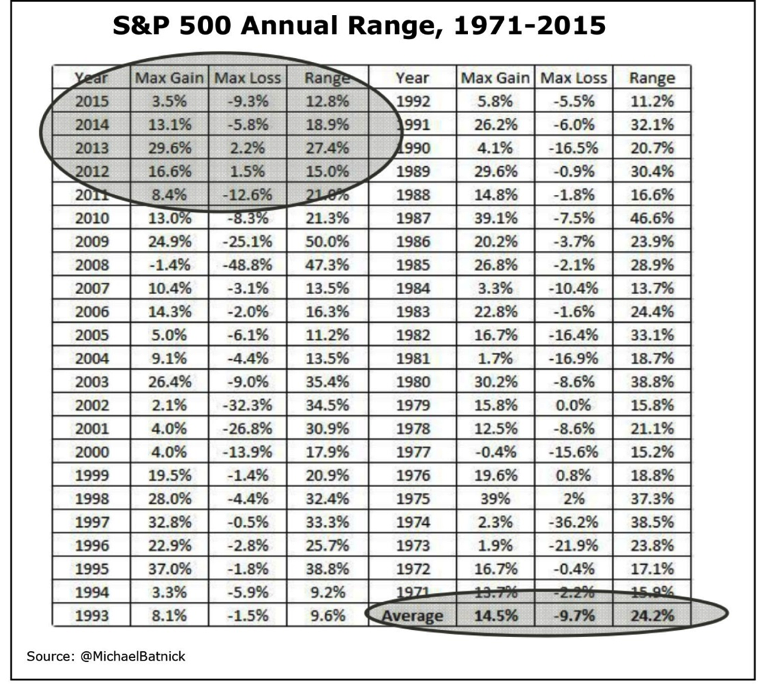

Outside of the August swoon and October surge, 2015 as a whole was a relatively quiet year. From the perspective of the range between the maximum year-to-date gain and maximum year-to-date loss, 2015 saw the narrowest spread since 2005. This range that was about half the long-term average. Despite this, investors had a sense that volatility was at extremely high levels. Given this reaction, and indications that stocks remain overvalued, breadth failed to follow through to the upside and investors remained fully allocated to stocks, it seemed a real return to volatility was more likely than not in 2016. So far, that has been the case. Volatility is not necessarily entirely negative for stocks, as high levels of volatility are usually seen as stocks make important lows.

Graphic 2. S&P 500 Annual Range, 1971-2015

Source: @MichaelBatnick

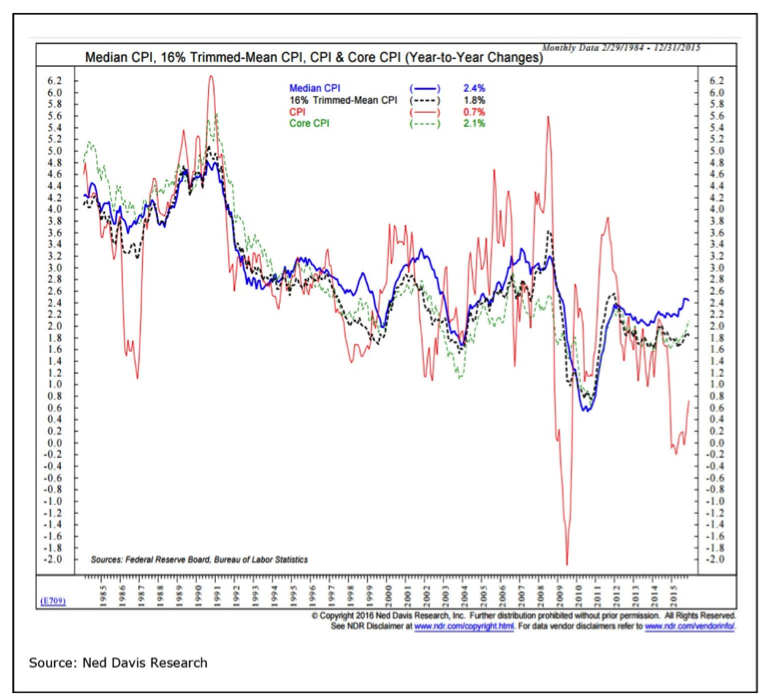

Graphic 3. Media CPI, 16% Trimmed-Mean CPI, CPI & Core CPI (Year-to-Year Changes)

Source: Ned Davis Research

Federal Reserve Policy is neutral. Another source of potential volatility is a less friendly Fed. The 25 basis point rate hike enacted in December is unlikely to represent a meaningful drag for the economy or for stocks. But by embarking on a path of normalizing interest rates, the perceived protection the Fed was supplying to the financial markets has been taken away. Further, while the collapse in oil prices has depressed headline inflation, core measures of inflation, as well as wages, are starting to accelerate. While we do not expect inflation to get out of control, there is room for some upside surprises in inflation and that could add to the noise that stocks must navigate.

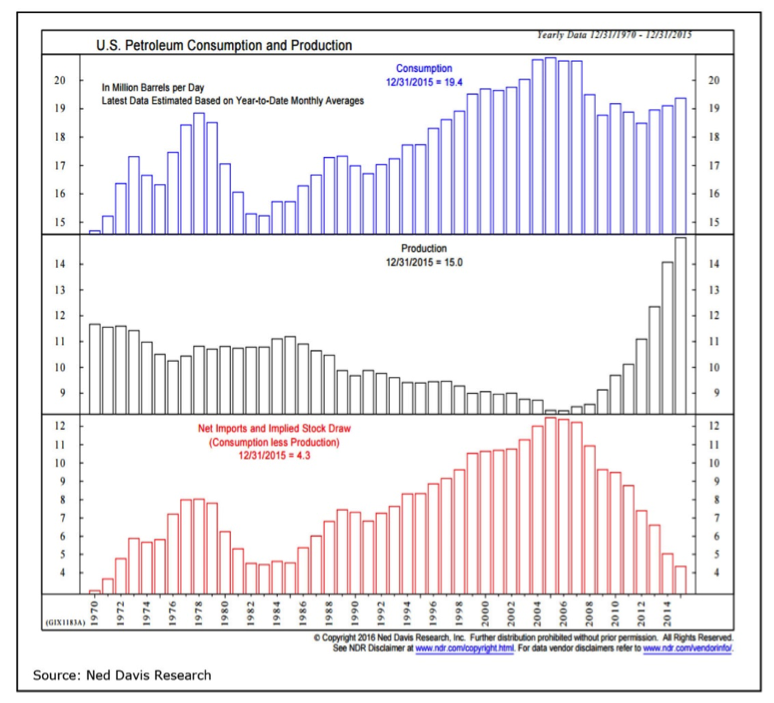

Economic Fundamentals remain bullish. The U.S. manufacturing sector continues to have pockets of weakness, but overall the economy remains on stable, if not spectacular footing. The decline in the price of oil has captivated headlines and is leading to increased concern about the health of the global economy. Just as parts of the U.S. economy are negatively impacted by weakness in the energy sector, so too are parts of the global economy (especially emerging markets). The driver behind lower oil prices, however, is not a collapse in demand, but surge in production, especially here in the U.S. We have doubled our annual production of oil over the past decade, while demand has held relatively stable.

Graphic 4. U.S. Petroleum Consumption and Production

Source: Ned Davis Research

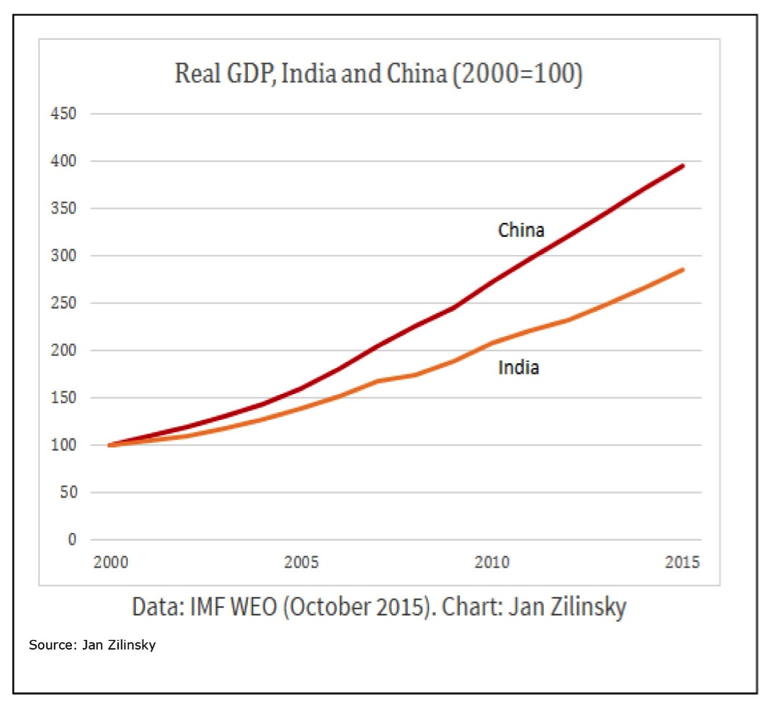

Graphic 5. Real GDP, India and China (2000=100)

Source: Jan Zilinsky

Another global economic concern has to do with slowing growth in China. To whitewash the imbalances that have emerged in the Chinese economy would be naïve, and whatever the actual growth rate is (the official numbers are viewed by many as somewhat suspicious), it represents a marked deceleration over the pace of growth seen in recent years. Some slowdown is to be expected, however, as the Chinese economy is now four times as a large as it was 15 years ago. China’s contribution to global growth is as large as in recent years even though its growth rate is slower. Despite its increased size, exports to China still represent only a tiny portion of U.S. economic activity.

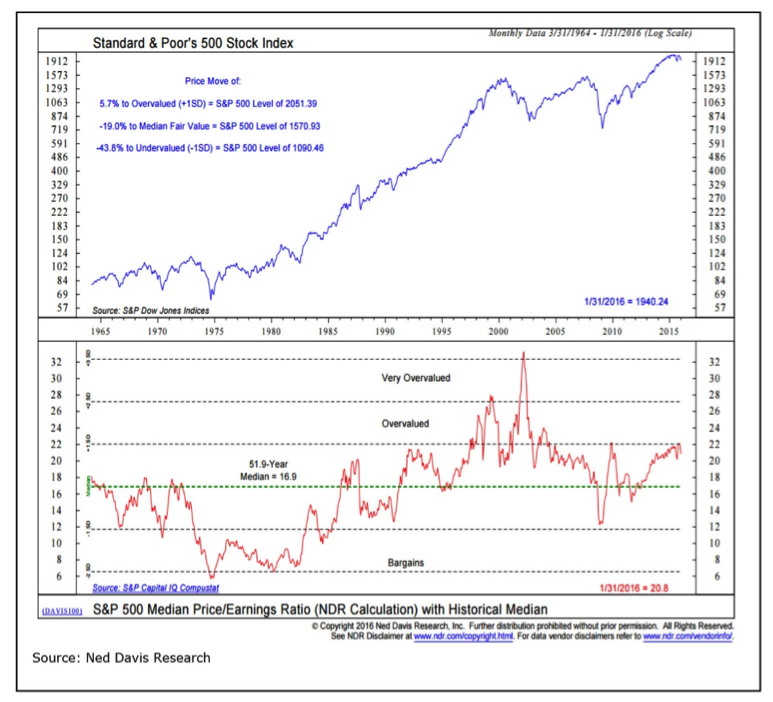

Valuations remain bearish. When considering valuations, we look at reported earnings on a trailing basis. Valuations based off of forward earnings or operating earnings can give a distorted view of the valuation picture. Operating earnings can be massaged and forward earnings have tended to be overly optimistic. Valuations have been building over the past few years as stock market gains have gotten ahead of fundamental improvements. A meaningful low in stocks is not likely to be reached when stocks are overvalued relative to their historical average. Importantly, valuation improvement can come through price correction, better earnings growth or, as may be the case in 2016, both.

Graphic 6. Standard & Poor’s 500 Stock Index

Source: Ned Davis Research

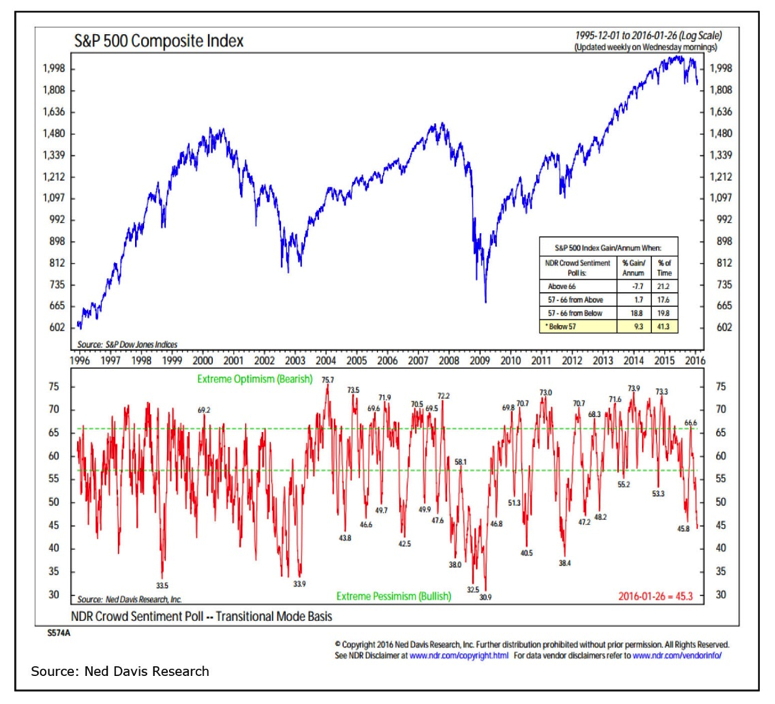

Graphic 7. S&P Composite Index

Source: Ned Davis Research

Sentiment is bullish, but this view comes with a caveat. Based on the experience of the past several years, pessimism is at a level from which stocks have tended to rebound. Investors have responded to the December/January stock market weakness by raising cash and tilting away from equities. The caveat is that this may be the beginning of needed longer-term asset allocation shift from equities to cash. When completed, that shift would have bullish implications, but as it is underway it may mean that more evidence of excessive pessimism is needed to fuel stock market gains.

Seasonal patterns and trends are now neutral. While there is modest bias higher in the first quarter of presidential election years, the overall pattern over the first three quarters of the year tends to be trendless volatility. Stocks tend to rise in the fourth quarter as the outcome of the election comes into focus. Early year volatility could be more exaggerated this year given the seemingly wide-open primary battles and the lack of a prevailing trend higher in stock prices. While the January pullback found support near last year’s lows, this chart of the S&P 500 shows that stocks have gone basically nowhere since the second half of 2014.

Graphic 8. $SPX S&P 500 Large Cap Index INDX

Source: Stock Charts

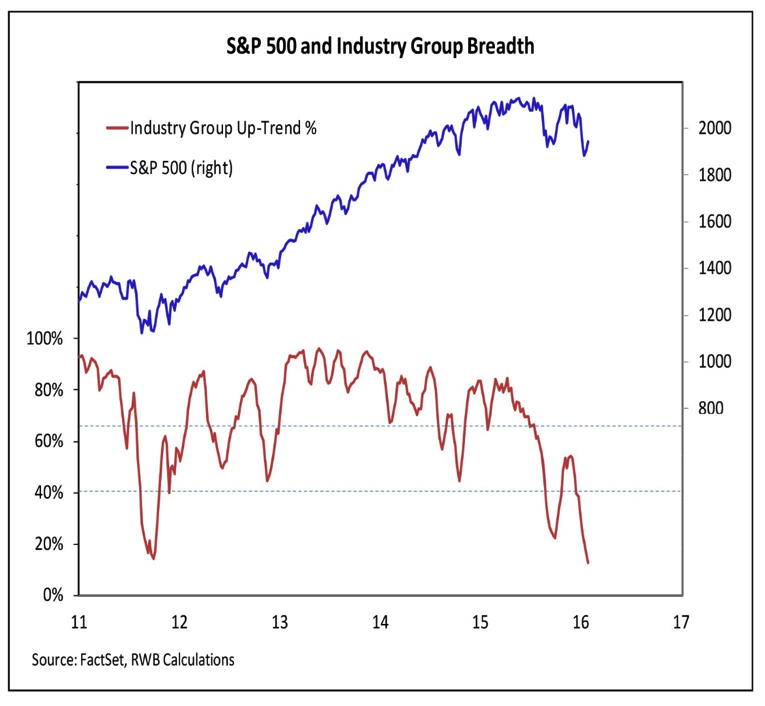

Graphic 9. S&P 500 and Industry Group Breadth

Source: FactSet, RWB Calculations

Breadth is bearish. The rally that emerged in October last year initially featured a turn higher in our industry group trend indicator. The pace of this improvement suggested broad rally participation, which was a change in tone over the deterioration that had been seen over the first half of 2015. This initial thrust higher stalled, however, and breadth has deteriorated in 2016. New lows have expanded and the percentage of industry groups in up-trends has contracted. Given the weakness in the broad market, we would view any price rallies seen in the popular averages with some skepticism. Breadth tends to bottom before price and there is not yet evidence that the broad market has made a good low.

Given the neutral assessment of the current environment from our weight of the evidence and the prospects for continued volatility, investors should consider using near-term rallies to trim exposure to equities to levels that are slightly below their longer-term target levels. Holding levels of cash can help mitigate the effects of higher volatility. Small-caps were unable to rally with seasonal tailwinds at their back, and it now looks like a longer-term trend in large-cap leadership is emerging. From a regional perspective, equity exposure should be tilted toward the U.S. and away from international stocks.

Graphic 10. $RUT: $SPX Russel 2000 Small Cap Index | S&_ Large Cap Index INDX

Source: Stock Charts

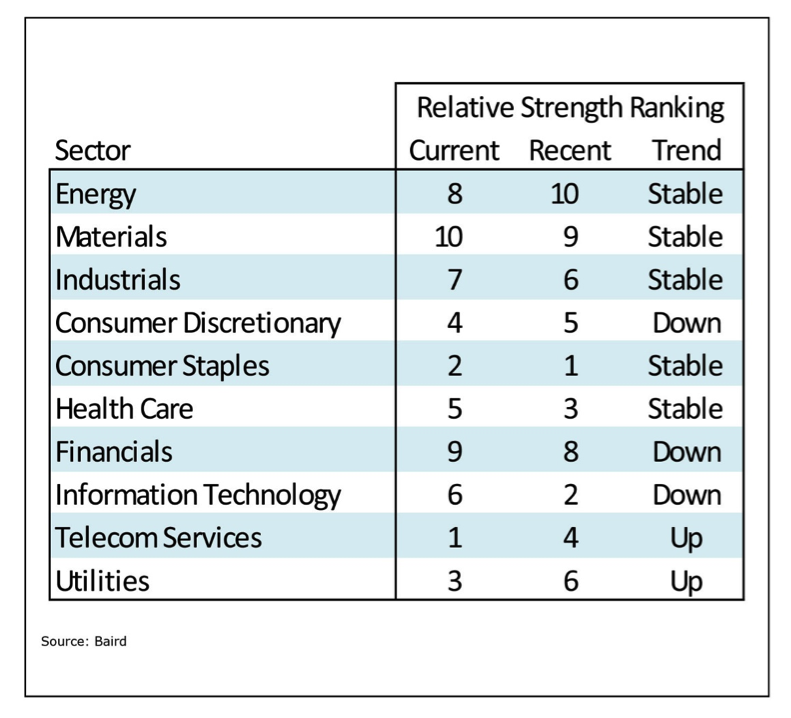

Graphic 11. Relative Strength Rankings

Source: Baird

Our relative strength rankings have shown a pronounced shift toward defensive leadership. Information Technology, Consumer Discretionary and Financials have ranking trends that are moving lower, while Utilities and Telecom have trends that are rising. Consumer Staples and Health Care are relative stable near the top of the rankings (although weakness within the Biotech space is weighing on the Health Care sector overall). Energy, Materials and Industrials are relatively stable near the bottom of the rankings. Industrials have not made a relative price low versus the S&P 500 since August and could be a contrarian way to benefit from better economic growth going forward given the overwhelmingly negative sentiment in that space.

Appendix – Important Disclosures and Analyst Certification

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy.

ADDITIONAL INFORMATION ON COMPANIES MENTIONED HEREIN IS AVAILABLE UPON REQUEST The indices used in this report to measure and report performance of various sectors of the market are unmanaged and direct investment in indices is not available.

Baird is exempt from the requirement to hold an Australian financial services license. Baird is regulated by the United States Securities and Exchange Commission, FINRA, and various other self-regulatory organizations and those laws and regulations may differ from Australian laws. This report has been prepared in accordance with the laws and regulations governing United States broker-dealers and not Australian laws.

Copyright 2016 Robert W. Baird & Co. Incorporated

Other Disclosures

United Kingdom (“UK”) disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited (“RWBL”) holds a MiFID passport.

This material is distributed in the UK and the European Economic Area (“EEA”) by RWBL, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB and is authorized and regulated by the Financial Conduct Authority (“FCA”).

For the purposes of the FCA requirements, this investment research report is classified as investment research and is objective.

This material is only directed at and is only made available to persons in the EEA who would satisfy the criteria of being "Professional" investors under MiFID and to persons in the UK falling within articles 19, 38, 47, and 49 of the Financial Services and Markets Act of 2000 (Financial Promotion) Order 2005 (all such persons being referred to as “relevant persons”). Accordingly, this document is intended only for persons regarded as investment professionals (or equivalent) and is not to be distributed to or passed onto any other person (such as persons who would be classified as Retail clients under MiFID).

Robert W. Baird & Co. Incorporated and RWBL have in place organizational and administrative arrangements for the disclosure and avoidance of conflicts of interest with respect to research recommendations.

This material is not intended for persons in jurisdictions where the distribution or publication of this research report is not permitted under the applicable laws or regulations of such jurisdiction.

Investment involves risk. The price of securities may fluctuate and past performance is not indicative of future results. Any recommendation contained in the research report does not have regard to the specific investment objectives, financial situation and the particular needs of any individuals. You are advised to exercise caution in relation to the research report. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

RWBL is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the FCA under UK laws, which may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.