US Equity and Economic Review: The Data Points To A Slowdown, Not A Recession, Edition

Recent market and statistical weakness has led to increased discussion of a possible US recession. In this column, I will argue that instead of a recession, we’re facing a situation similar to the mid-1980s, where the economy also experienced slowdown caused by high oil prices, a strong dollar slowdown and weak oil sector. But there is insufficient weakness – largely thanks to continued housing market strength and recent wage growth – for a recession to occur.

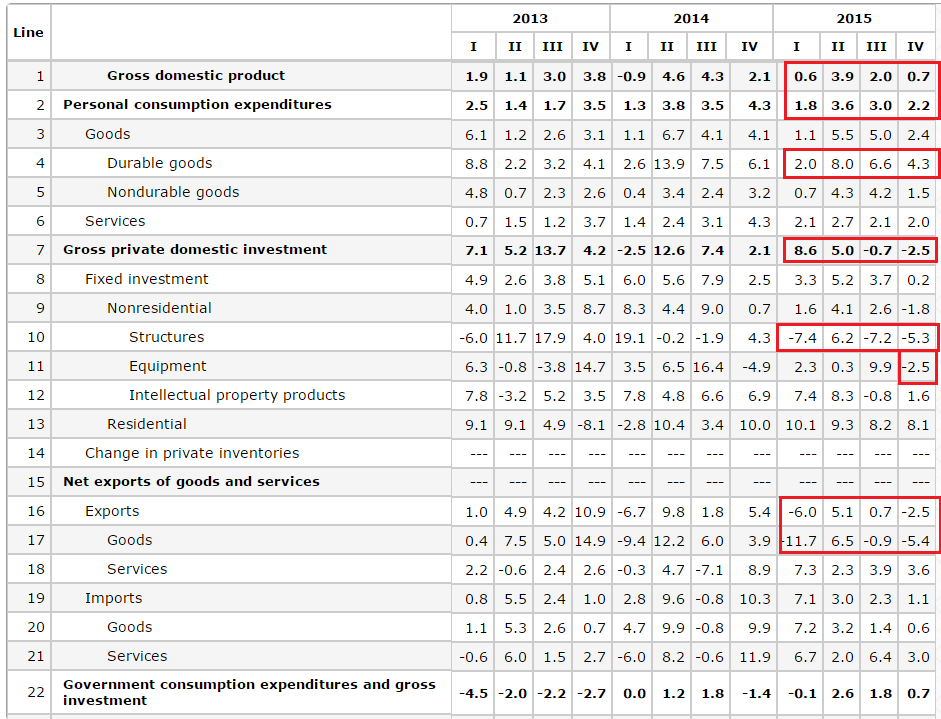

Let’s start with the Q/Q growth numbers:

Between 1Q15-4Q15, personal consumption expenditures (PCEs) fluctuated between .6% and 3.9% Q/Q growth. Durable goods purchases varied between 2%-8% growth – an encouraging pace. And service spending was constant, with numbers seesawing between 2%-2.7%. Investment is where problems emerge. Non-residential structural spending contracted in 3 of the last 4 quarters; spending on equipment was weak in 2Q14 (.3% increase) and contracted in 4Q15. But residential investment grew strongly in all four quarters. And finally, we have exports, which contracted in 2 of the last four quarters. The Q/Q numbers show modest growth, with the weak oil/gas extraction market and strong dollar hurting growth.

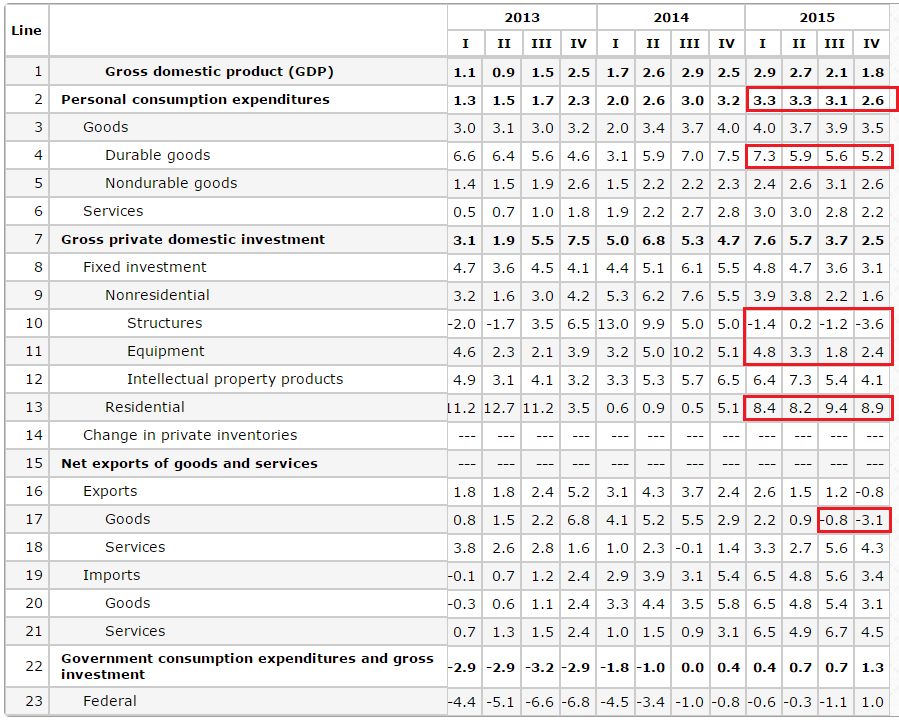

Let’s turn to the Y/Y numbers for the same figures:

Topline PCE growth recorded levels between 2.6%-3.3% for the last 4 quarters – a decent pace of growth. Consumer durable goods expenditures were very strong, vacillating between 5.2% and 7.3%. As with the Q/Q figures, Y/Y business investment numbers were weak; non-residential structural investment declined in 3 of the last 4 quarters. But residential spending increased at a solid pace. And exports declined in the 2H15. So, like the Q/Q numbers, we again see evidence of industrial and export weakness.

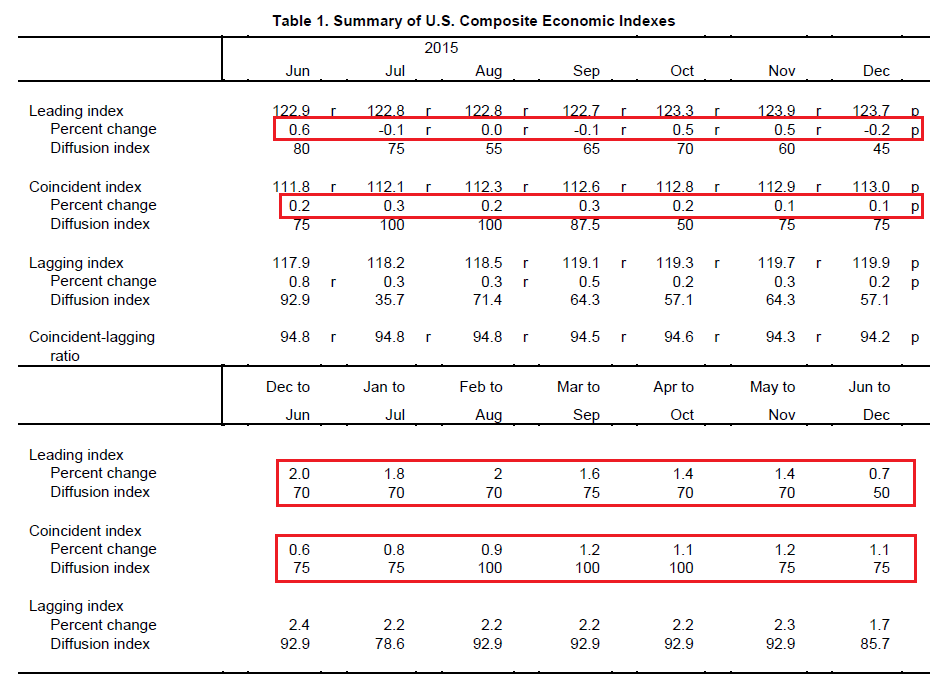

The US LEIs and CEIs help to place this information in business cycle context. First is this observation of the LEIs from the latest release:

The Conference Board LEI for the U.S. decreased in December, with large negative contributions from the ISM® new orders index and building permits more than offsetting the large positive contribution from the yield spread. In the second half of 2015, the leading economic index increased 0.7 percent (about a 1.3 percent annual rate), much slower than the growth of 2.0 percent (about a 4.0 percent annual rate) during the first half of the year. In addition, the strengths among the leading indicators have become less widespread and are now only balanced with the weaknesses.

So the pace is slowing and the breadth of advances is decreasing. But the data is far from clear:

The LEIs have printed either 0 or negative readings in 4 of the last 7 months while the CEIs have printed between .1 and .3 (top table). But while the lower table shows a slowdown in the LEIs 6 month rate of change, the CEIs increased. Here is the conclusion reached by the Conference Board’s economists

The Conference Board LEI for the U.S. declined in the final month of 2015, with its six-month growth rate decelerating. In addition, the strengths among the leading indicators are now balanced with the weaknesses. Meanwhile, the CEI has continued rising slowly, and as a result its six-month growth rate is higher than in the first half of 2015. Taken together, the current behavior of the composite indexes and their components suggest that while risks to growth have increased, although not significantly, the expansion in economic activity should continue at a moderate pace in the near term.

In theory, LEI weakness should translate into CEI weakness. When that doesn’t happen, it is more likely than not that a recession isn’t likely.

The reason for the current slowdown is a combination of weak international growth, a strong dollar and weak oil prices. The economy faced the exact same set of facts in the mid-1980s – a fact observed by the blog, The Money Illusion:

See if this sounds familiar. Halfway through a long expansion, industrial production levels off, after years of rapid growth. This is blamed on two factors, declining oil prices and a strong dollar. I could be describing the past year, or I could be describing 1985-86:

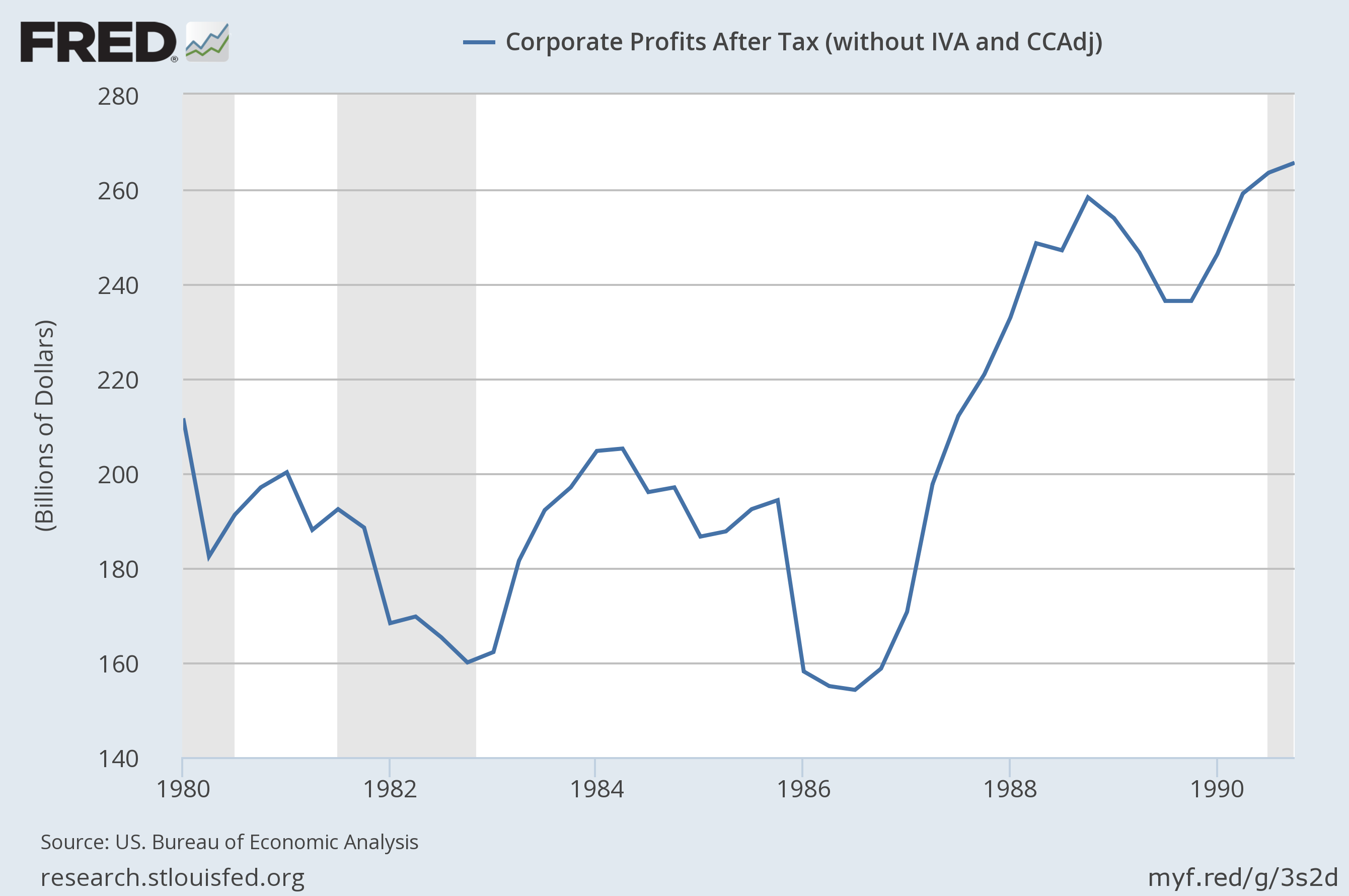

In addition, we’re seeing weakness in corporate profits. But this isn’t a collapse; instead, it’s a measured downward shift caused by a stronger dollar and weaker overseas economies. This also occurred between 1984-1986:

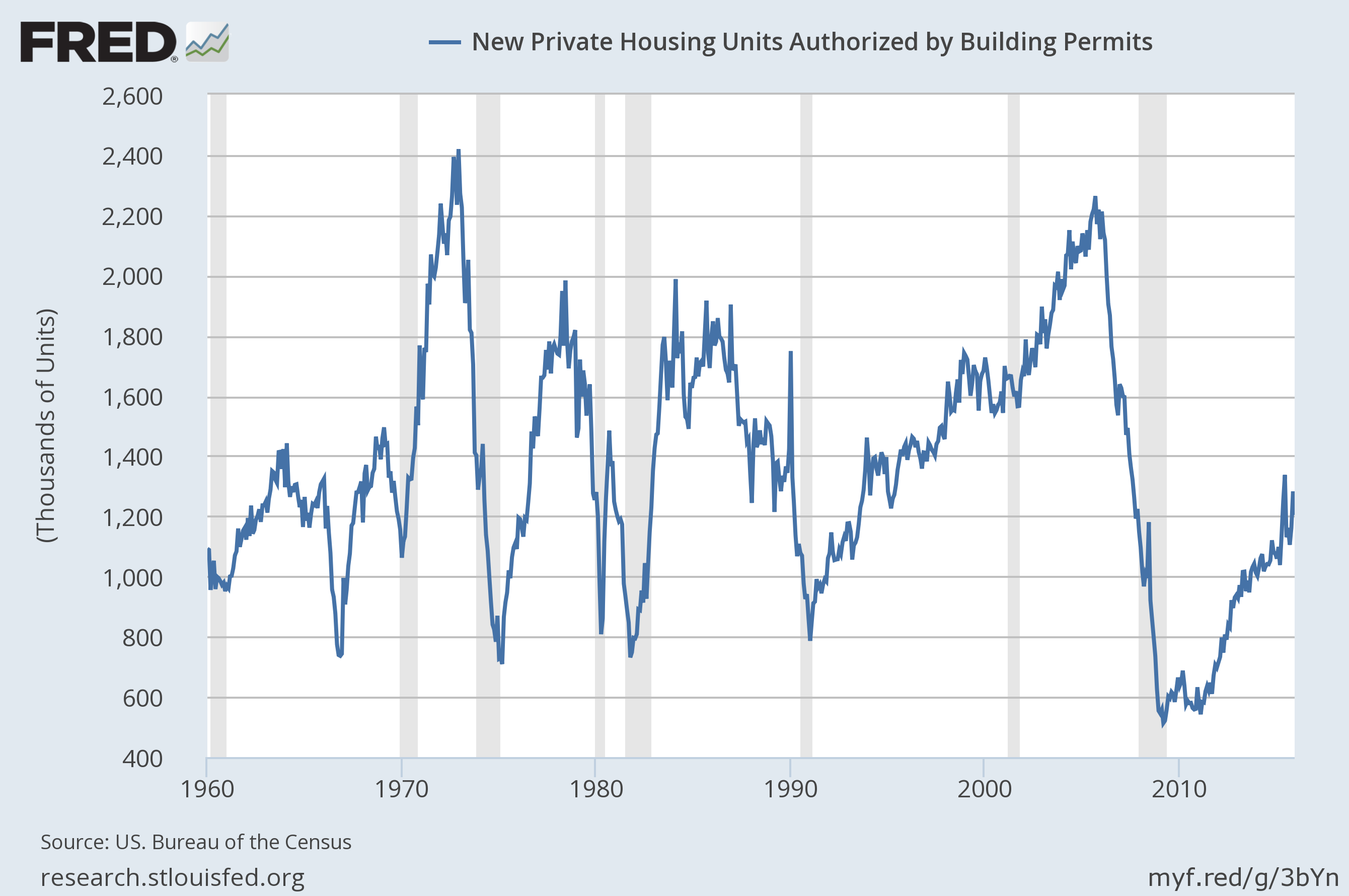

Two other data points show very important pockets of strength. Let’s start with the housing market. In the above tables, both the Q/Q and Y/Y residential investment numbers show consistently strong gains. Best of all, building permits continue to increase, meaning we should continue to see these strong paces of residential investment continue:

And the rate of new and existing home sales continues to slowly increase:

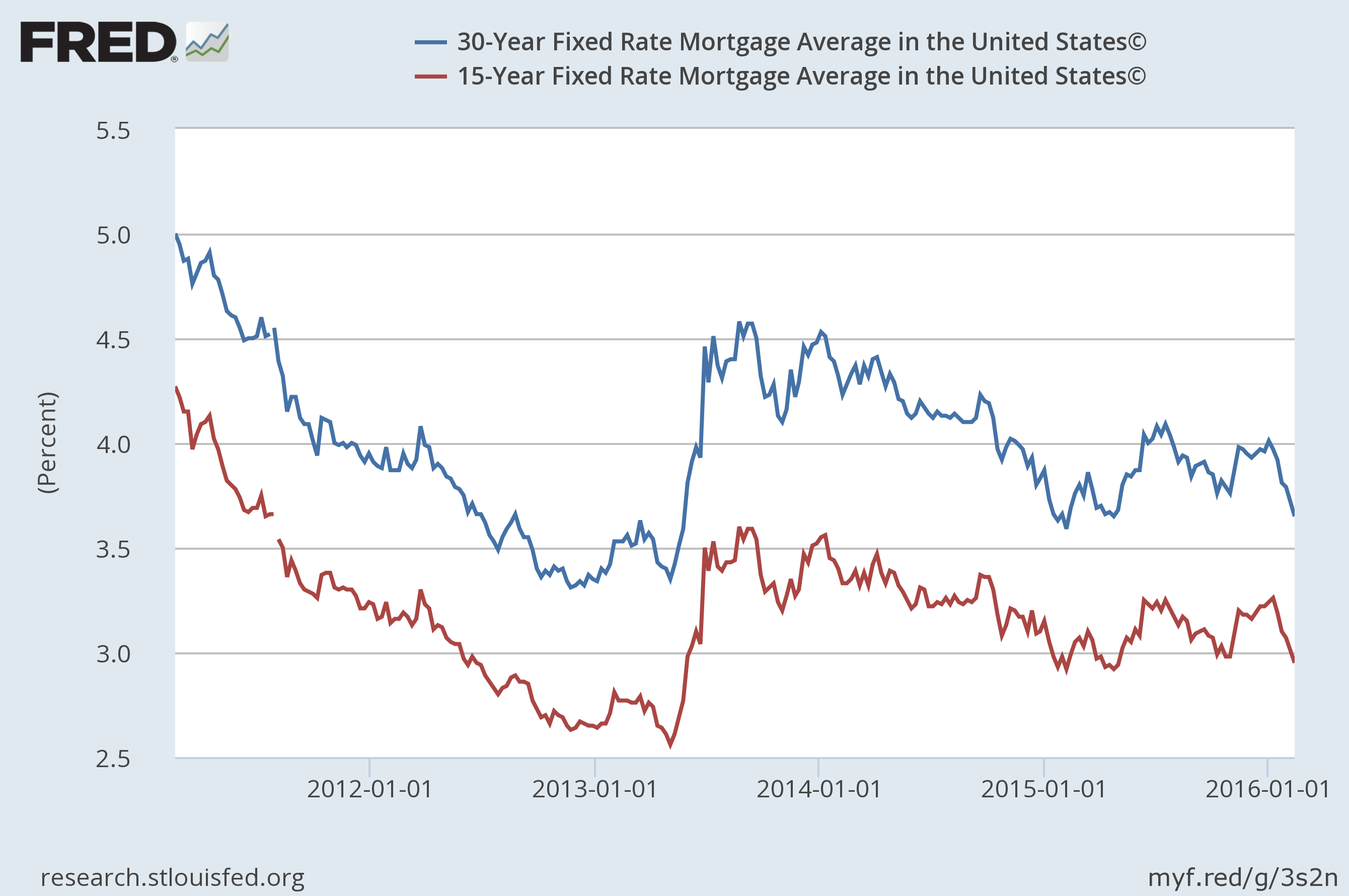

The graph above shows new and existing home sales since the end of the recession. The top chart shows the data in a long, historical context, highlighting that current levels are still low. The lower graph shows a consistent upward movement. The recent treasury market rally has pushed mortgage rates lower:

The 30 mortgage is ~3.75 while the 15 is ~3% -- both very affordable levels.

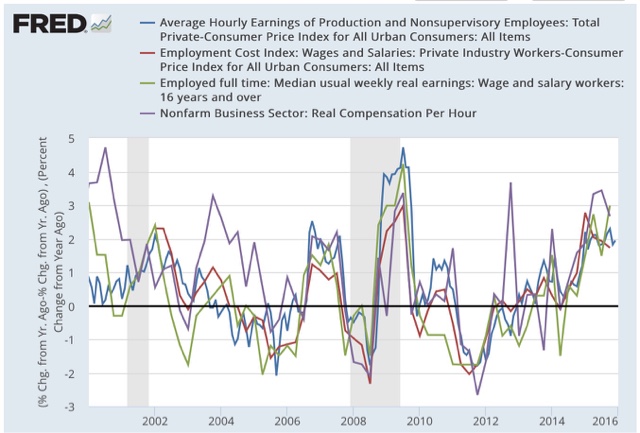

And wages are finally increasing. Here are two charts from my co-blogger that show both Q/Q and Y/Y increases in several wage measures:

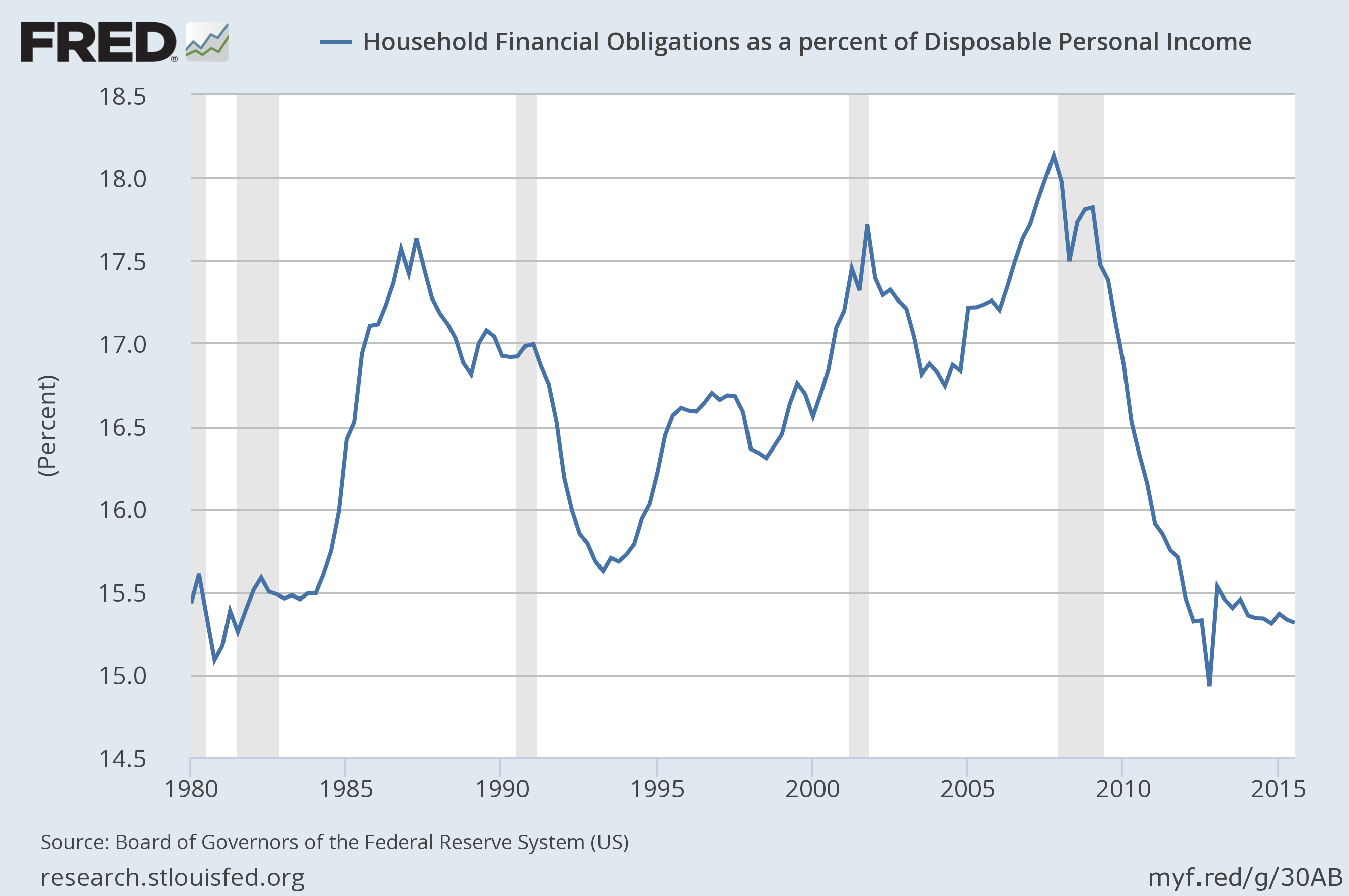

And households are in far better financial shape:

The top chart shows the financial services obligation ration, which is near a 30 year low. The bottom chart shows the personal savings rate, which, while low by historical standards, has ticked up in the latest expansion. Taking these two charts together, we see a consumer who has lowered his debt exposure and has an increased capability of surviving a downturn.

To conclude: the economy experienced a similar slowdown in the mid-1980s, which did not prove fatal to continued growth. Currently, there are two reasons why the current slowdown will not lead to a recession: the housing market is still improving and consumers not only are in better financial shape but are also (finally) seeing a pick-up in earnings.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis