Chairperson Yellen gave her bi-annual Congressional testimony this week, which contained the following two key paragraphs:

Financial conditions in the United States have recently become less supportive of growth, with declines in broad measures of equity prices, higher borrowing rates for riskier borrowers, and a further appreciation of the dollar. These developments, if they prove persistent, could weigh on the outlook for economic activity and the labor market, although declines in longer-term interest rates and oil prices provide some offset.

.....

As is always the case, the economic outlook is uncertain. Foreign economic developments, in particular, pose risks to U.S. economic growth. Most notably, although recent economic indicators do not suggest a sharp slowdown in Chinese growth, declines in the foreign exchange value of the renminbi have intensified uncertainty about China's exchange rate policy and the prospects for its economy. This uncertainty led to increased volatility in global financial markets and, against the background of persistent weakness abroad, exacerbated concerns about the outlook for global growth. These growth concerns, along with strong supply conditions and high inventories, contributed to the recent fall in the prices of oil and other commodities. In turn, low commodity prices could trigger financial stresses in commodity-exporting economies, particularly in vulnerable emerging market economies, and for commodity-producing firms in many countries. Should any of these downside risks materialize, foreign activity and demand for U.S. exports could weaken and financial market conditions could tighten further.

Central banks have a far longer time horizon than the markets. And while the recent weakness feels like forever, it’s only been six weeks – a pittance in central bank time. But markets were wondering if the recent financial market sell-off would make it onto the Fed’s radar screen. It did. And the markets should breath a sign of relief for this inclusion in the Fed statement.

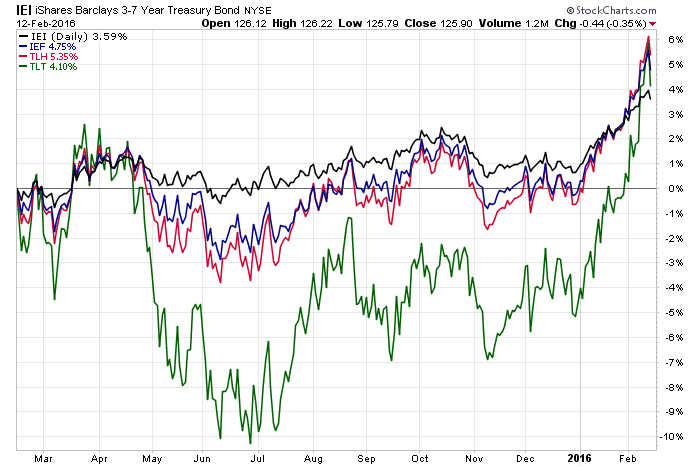

The treasury market has rallied strongly since the first of the year:

The entire curve has rallied between 1.75% and 6.5% (see last week's column). In addition, the yield curve has narrowed:

The “yield curve” — the slope made up of the yields of Treasury bonds of various maturities — is a popular gauge for the health of economies, and historically the most accurate market gauge for a recession. While the stock market has a patchy record of predicting economic downturns, the US yield curve has “inverted”, when short-term borrowing costs are higher than longer term ones, ahead of every recession since the second world war.

The yield curve is still far from inverting, but the difference between the 2 and 10-year Treasury yield, a popular measure of its shape, on Wednesday slipped just below 100 basis points (or 1 percentage point) for the first time since January 2 2008.

.....

While the yield curve is not inverting, some analysts argue that its flattening may still be a recession omen. The shape of the slope should be adjusted for the fact that short-term interest rates are still extremely low, according to Ruslan Bikbov, an analyst at Bank of America Merrill Lynch.

There are a number of reasons for this rally and narrowing, starting with an overall concern the world economy is slipping towards a recession:

If major government bond markets are right, the global economy is sliding towards recession and central bank easing policies will pull borrowing rates deeper into negative territory.

Some noted this was a pure flight to safety:

Investors sought top-tier sovereign debt and shunned eurozone periphery bonds on Monday as equity markets tumbled and oil prices declined.

Benchmark 10-year yields in Germany, the UK and US fell as bond prices rose on haven demand, while the cost of Italian, Spanish and Portuguese debt climbed back towards their highest levels this year.

“The fall in core government yields is mostly the result of the move in other assets,” said rates strategist Nishay Patel of UBS.

Some argued this was pure panic:

There’s now $7 trillion of government debt with yields below zero globally, with the average yield on the Bank of America Merrill Lynch World Sovereign Bond Index at 1.29 percent, the lowest in data going back to 2005. Futures traders pared the odds the Federal Reserve will raise interest rates this year to 27 percent before Chair Janet Yellen begins her two-day testimony to Congress on Wednesday.

“Global risk aversion is being driven by underlying concerns about banks, energy prices and equity markets, and that is one part of what is driving Treasury yields lower,” said Guy LeBas, chief fixed-income strategist at Janney Montgomery Scott LLC in Philadelphia. The other “is genuine expectations of weaker U.S. inflation and economic growth. So Yellen will be huge for the markets this week.”

All of these stories paint part of the overall picture. But the sum total is clear: the Treasury market sees weak growth over the next 6-12 months.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis