International Economic Week in Review: Data Points To Continued Weak Growth, Not Recession, Edition

The market sell-off that started at the beginning of the year has led to increased talk of recession. But the underlying data of most major economies does not point to that potential outcome (at least, not yet). The EU continues to grow slowly, as does the UK. Australia is making the transition from a raw materials exporter to a more balanced economy while Japan meanders slightly forward. Most importantly, China continues to post solid GDP gains (I take an in-depth look at the US in this week’s equity column and conclude there is sufficient underlying strength to maintain a positive rate of growth).

The ECB released their latest Economic Bulletin, which contained the following assessment of the EU economy:

The economic recovery in the euro area is continuing, largely on the back of dynamic private consumption. More recently, however, the recovery has been partly held back by a slowdown in export growth. The latest indicators are consistent with a broadly unchanged pace of economic growth in the fourth quarter of 2015. Looking ahead, domestic demand should be further supported by the ECB’s monetary policy measures and their favourable impact on financial conditions, as well as by the earlier progress made with fiscal consolidation and structural reforms. Moreover, the renewed fall in the price of oil should provide additional support for households’ real disposable income and corporate profitability and, therefore, private consumption and investment. In addition, the fiscal stance in the euro area is becoming slightly expansionary, reflecting inter alia measures in support of refugees. However, the recovery in the euro area is dampened by subdued growth prospects in emerging markets, volatile financial markets, the necessary balance sheet adjustments in a number of sectors and the sluggish pace of implementation of structural reforms. The risks to the euro area growth outlook remain on the downside and relate in particular to the heightened uncertainties regarding developments in the global economy as well as to broader geopolitical risks.

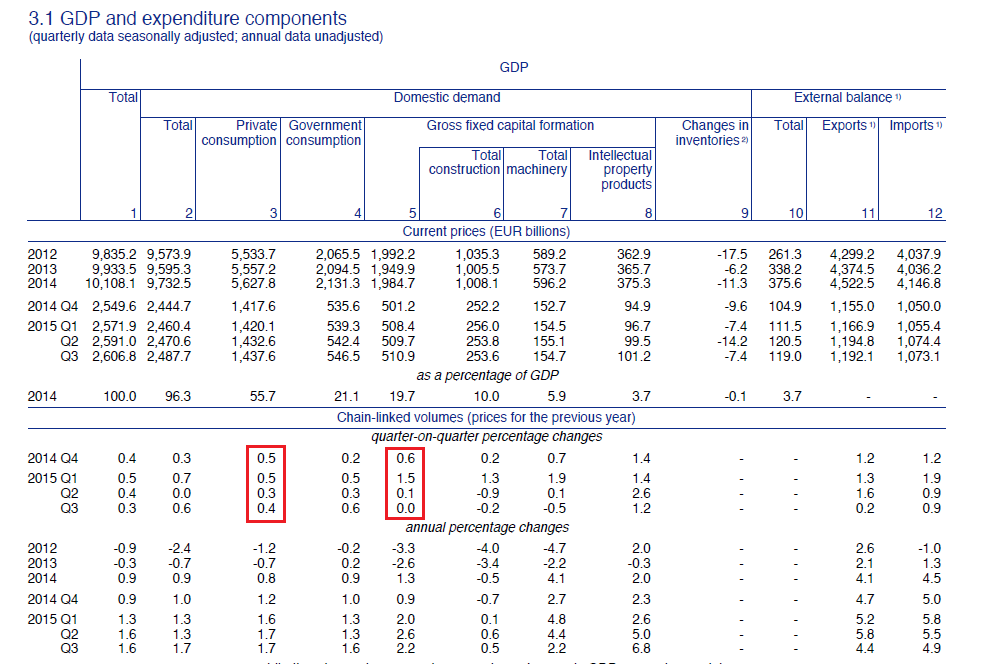

Here is the accompanying GDP table from the report:

Consumer spending increased between .3%-.5% Q/Q between 4Q14 and 1Q15. Consumer loan growth – which consistently increased over 2015 – supported this growth:

But while investment rose a strong 1.5% in 1Q15, 2Q-3Q growth was far more subdued, with readings of .1% and 0%, respectively. However, weak business spending hasn’t slowed overall GDP growth which consistently increased over the last 8 quarters:

Looking ahead, the ECB places a great deal of emphasis on the oil dividend not only aiding consumers but businesses profit margins. And there’s no reason to think this won’t eventually happen. But, it will take time for this dividend to be spent. Exports are the one potential weakness. The EUs current account has been positive since 2013; this is a big reason why the region didn’t fall into recession during the Greek crisis. But with emerging markets weakening, the EU export machine could take an additional hit. But there is no reason to think these factors will lead to a contraction, only weaker growth.

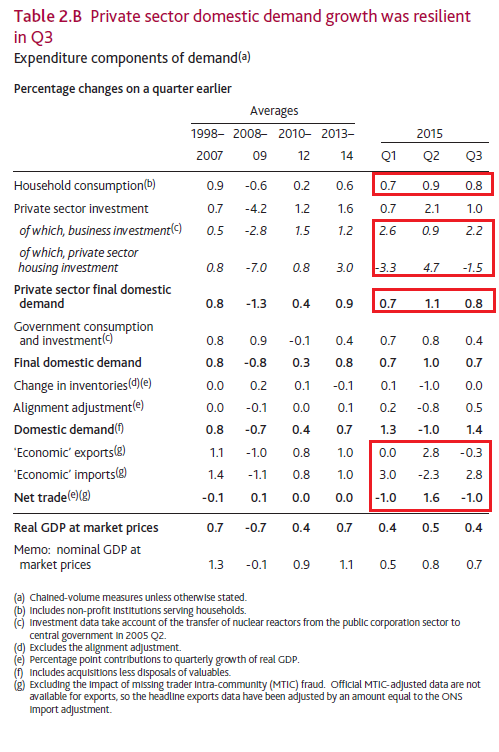

The UK’s inflation report contained the following table of GDP growth:

Personal spending grew between .7%-.9% Q/Q for the first three quarters of 2015. The BOE attributed it to improved confidence and increased income. Business investment was also positive (with the exception of an oil/gas slowdown) thanks to solid credit growth. The bank offered the following explanation of trade:

While the output data suggest that weaker external demand may have contributed to the slowing in GDP growth since 2013 (Section 2.1), net trade was only a small drag on growth over 2015 (Table 2.B). In particular, despite weak world demand growth and the past appreciation in sterling, exports are estimated to have increased by 6% in the four quarters to Q3. Since the November Report, sterling has depreciated by around 3½%, which might be expected to boost demand for UK exports to some extent. But sterling remains around 13% above its trough in early 2013 and any boost from the recent depreciation is likely to be offset by the weaker outlook for world trade (Section 1). Export growth is expected to moderate slightly in the near term, consistent with the recent falls in survey indicators of goods exports (Chart 2.10).

Overall, the report was generally positive. However, the latest production and manufacturing report was weak, with both production and manufacturing declining (both, however, are still positive):

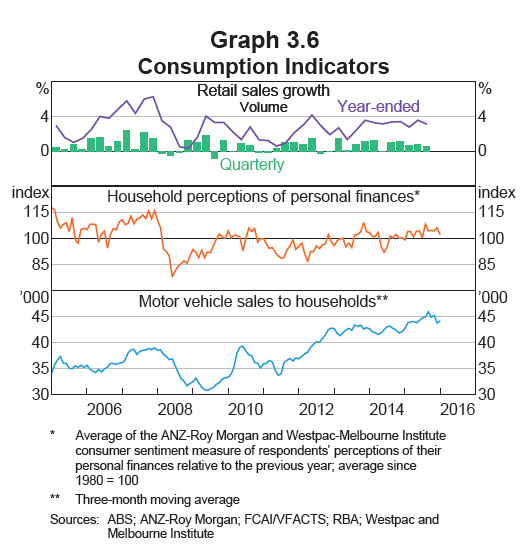

The RBA released its statement on monetary policy, which included a positive picture. Household consumption and investment are increasing. Fairly strong employment growth supports these expenses. Retail sales, consumer sentiment and auto sales support this observation:

But business investment is weak, largely due to a contraction in raw material investment:

In the above chart, engineering investment dropped sharply over the last few years while machinery investment moved sideways. These points coincide with the recent completion of several large raw material projects and the lack of any new investments on the horizon. As a result, most business growth is coming from the service sector:

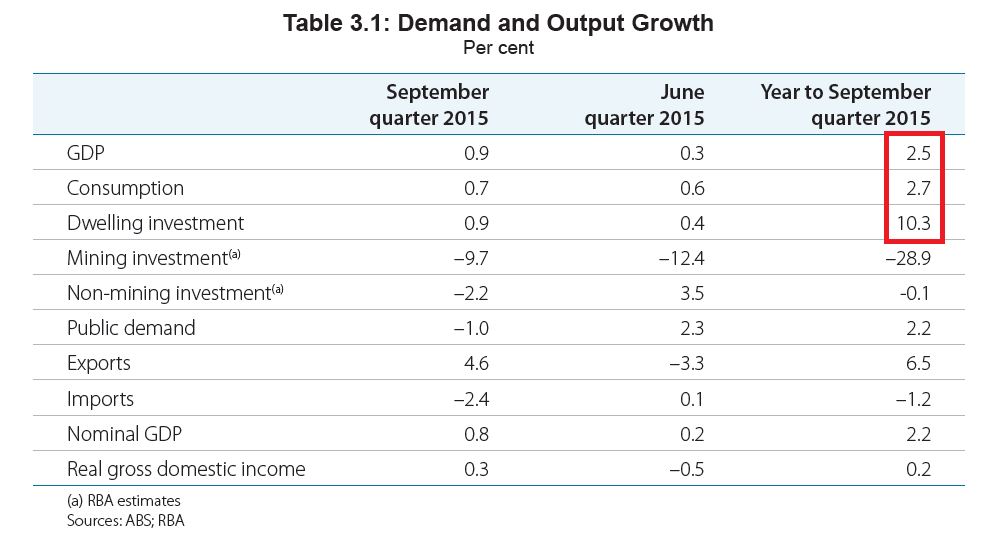

But as this table shows, with the exception of business investment, the Australian economy appears to be in fairly decent shape:

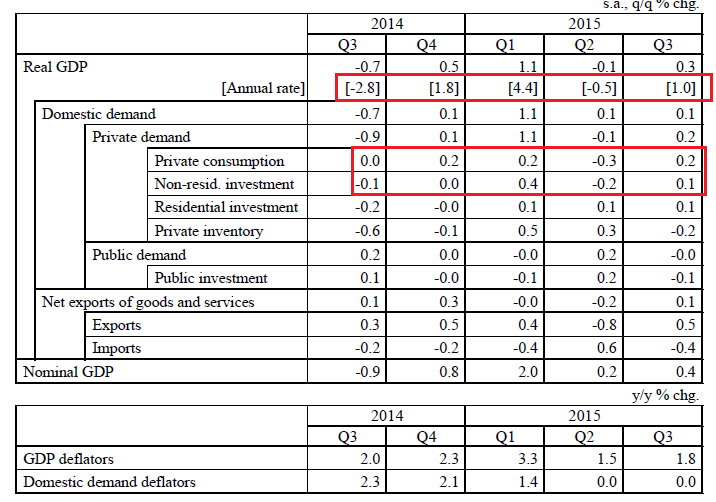

Now let’s turn to Japan, by first focusing on this table from the latest BOJ report:

Over the last 5 quarters, overall growth fluctuated between -2.8% and +4.4%. These are fairly extreme fluctuations and indicate the economy is clearing in a “two steps forward, one step back” position. More importantly, take a look at private consumption and non-residential investment. As I noted last week, the BOJ believes the economy is about to enter a virtuous cycle with rising incomes leading to increased consumer spending and rising business profits leading to increased investment. But the table above indicates the economy isn’t at that point yet. And here’s the central reason the weak growth:

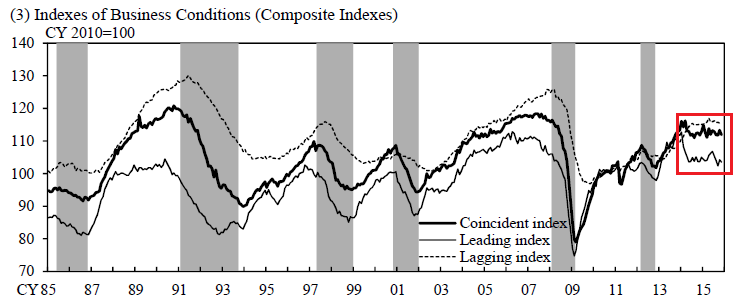

The leadings and coincident indicators moved sideways for the last two years, indicating a meandering economy. Japan continues to grow, but in a unsettling, sputtering manner. But, it nonetheless continues making slight forward progress.

And finally we have China, which started the global sell-off. First, remember the country is still growing at a solid rate:

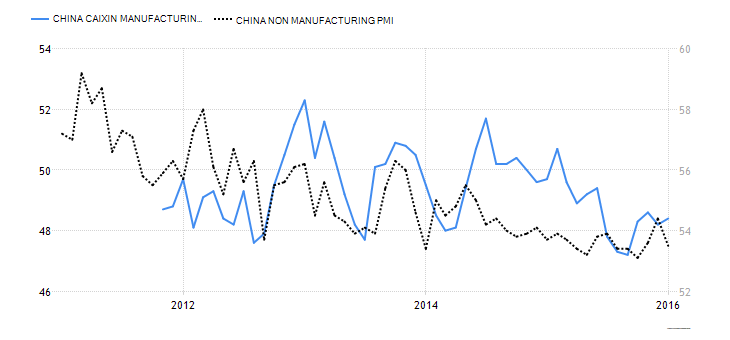

And while the manufacturing sector is contracting (blue line, left scale) the service sector continues to expand (dotted black line, right scale):

Yes, there are potential issues with debt and real estate. But the real issue is how China responded to market and economic instability. At various times, the financial market regulatory authorities have banned short-selling or instructed state investment funds to act as sops for share purchases. The PBOC has engaged in back-door currency devaluations to increase export competitiveness. These actions illustrate the real problem; the Chinese authorities are clearly very uncomfortable with the market volatility associated with economic corrections. As a rule, Chinese authorities are deeply concerned about social order. They are fundamentally obsessed with preventing any event that might lead to instability. But what they’re forgetting is market gyrations occur in capitalism. And if you want the benefits of a capitalist economy (largely because it increases wealth and thereby promotes stability) you also have to accept the messiness associated with market adjustments.

The above data shows that must major economies are OK. Yes, there are potential issues related to emerging market weakness bleeding into larger, advanced economies. But, as of this writing, we’re still in a slow, grinding growth.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis/