This year will likely be a challenging one for both the capital markets and investors. Investors are facing one of the worst stock markets in sixty years as stock prices plunge on news of slowing growth in China and plunging oil prices. We believe the risks in the economy are skewed to the downside and expect to see growing problems in manufacturing and the consumer sector. However, at the same time, this will prove to be a year of opportunity as stock prices of quality companies decline to levels that are now attractive and investors are adequately compensated for taking risk.

The U.S. economy is the deepest, most diverse economy of the developed countries and it is the bright light among developed economies which are struggling to show any sign of growth. However, the domestic economic recovery, which is in its sixth year, is showing signs of weakening. The manufacturing sector is showing signs of slowing. The energy sector has experienced a massive contraction as oil and natural gas prices have plummeted. At the same time, credit deterioration has accelerated which is typical late in the cycle.

With all the Federal Reserve’s talk about continued increases in interest rates in 2016, we expect the Fed will sit on the sidelines for the first half of the year. Financial regulatory reform has not addressed the “too big to fail” problem and, as a result, the Fed is attentive to financial market stability in the face of increased market volatility. In other words, the Fed doesn’t want to cause the next financial crisis or recession through its poor policy choices.

The recent market gyrations and dramatic sell off of domestic equities is not a repeat of 2008. During the Financial Crisis, there was concern over the undercapitalized banking system compounded by excessive household debt levels. Our financial system is significantly stronger today and there has been marginal improvement in the deleveraging of the consumer.

As we look forward to 2016, three themes are resonating with us.

First, the structural problems embedded in the economy continue to impede growth. We see evidence in the Financial Regulatory environment, the healthcare pricing model, and the lack of meaningful loan growth to small business. Domestically, the manifestation of these structural problems is low capital investment, slow private capital expansion and a sustained low velocity of money. Weak business investment strains economic output. This late in the recovery we would expect to experience much broader capital investment. However, business investment reported by the Commerce Department has increased a meager 2.2% from a year earlier. Capital investment will not grow organically as long as corporate management hides behind the belief that buying back stock, rather than investing in their business, creates long term value for shareholders.

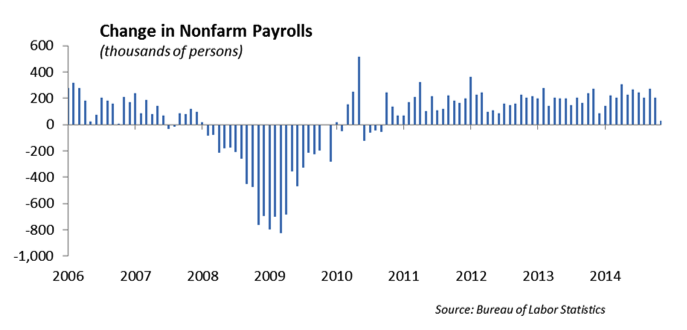

Second, job creation and wage growth are critical ingredients toward sustained economic growth. While the headline numbers are strong, the undercurrent reveals that much of the hiring appears both seasonal and part-time. At the same time, wage growth is stuck near 2%. Job growth is correlated with business formation, which in turn is a result of risk taking. The lack of business formation in our economy is a result of the inherently high risk to launch businesses. This takes the form of compliance, government regulations, capital raising, and infrastructure costs. Until we address these risks, we will not experience growth in business formations.

Third, we have talked about the ‘race to the bottom” as developed countries continue to weaken their currencies relative to the U.S. dollar. This will continue through 2016 as every developed country attempts to make their exports more competitive. A trade surplus helps domestic manufacturing which in turn helps sustain and create jobs. The U.S. economy will be marginally hurt by the stronger U.S. dollar.

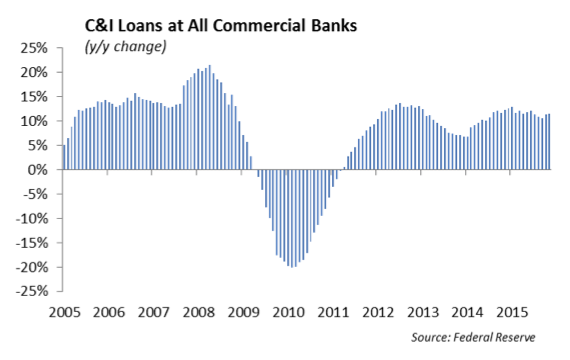

In order to move forward, our economy needs business formation. Small business creates jobs in our economy – not large business. Business formation will not happen until there is reasonable lending from banks to small businesses. There needs to be an adequate compensation for the risks assumed to start a business. And, therein lies the problem. The risks to start a business are still too high and financially the banks don’t need to make the loans to small businesses because they have many other places to go to earn a targeted rate of return on their capital. This is one of the main reasons that the Glass-Steagall Act is important to sustained economic growth – it focuses the banks on making loans.

The Economy

The U.S. economy is showing muddling growth near 2.1%. Domestic demand, which accounts for the majority of the economy, is still fairly stable, while activity in the manufacturing sector has deteriorated. We expect economic growth in 2016 to be challenged as the job market is pressured with increased lay-offs, manufacturers retrench, and global demand remains weak. The fourth quarter GDP number is going to show significant inventory adjustments and there is a growing likelihood that domestic economic growth will slow below 2% in 2016.

The decline in oil prices below $30 per barrel will ultimately provide a stimulus to the economy similar to a $2000 raise for any one driving a car or paying a heating bill. However, the rapid decline in oil prices will have a negative impact on local economies that are heavy in energy including Houston, Oklahoma, and the fracking regions in North Dakota. An estimated 145,000 jobs were lost last year due to the contraction in the oil industry. We believe the price of oil will settle in near $35 to $40 per barrel as global market share normalizes. The U.S. congress passed legislation that allows domestic shipments of oil which have been prohibited since 1975. At the same time, economic sanctions against Iran were lifted as part of a nuclear decommissioning agreement. It is expected that Iran will ultimately ship 500,000 barrels a day once their production capacity is back on line.

The ISM manufacturing survey declined again in December and is now showing its weakest level since the Financial Crisis. Our survey of small businesses reveals that smaller manufactures are seeing slowing in orders, while large manufactures are not showing any serious signs of revenue or volume declines. At the same time, auto sales are at record levels at 17 million units domestically. With auto loans out to 72 months and gas prices falling, we expect auto sales to continue to show strength.

The U.S. economy is less dependent on exports than other countries such as Germany, Spain and South Korea. Yet, exports as a percent of GDP have grown from 7% in 1990 to nearly 13% today. Exports have become an important engine in the domestic economy. As global growth slows, we will be exporting into economies that have declining demand which will likely hurt our exports. In addition, the decline in the U.S. dollar relative to other major currencies makes our exports more expensive on a relative basis, having a further negative impact on export growth.

Employment

The economy has added nearly 12 million jobs since the Financial Crisis pushing the unemployment rate down to 5.0% after peaking at 10% in October 2009. With the improvement in employment, we would expect to see gains in wages which have been slow to materialize. The Labor Department reported average hourly earnings rose 2.3% year over year in October. Wage gains will help push inflation up near the 2% threshold where the Federal Reserve is targeting.

While there is job growth in health care and construction, many of the jobs that are being created in the economy are lower level service sector jobs in retail and hospitality. The result is the income growth associated with those jobs is significantly lower, which ultimately impacts households by limiting consumption growth.

In addition, the labor force participation rate, which is the number of people eligible to work that are actively seeking employment is stuck down near 62.6%. At the same time, nearly 10% of the workforce is underemployed and over 6 million workers are still part time which is a disproportionally large number. We expect economic growth in 2016 to be challenged as the market for well-paying jobs contracts and labor participation continues to show weakness.

Federal Reserve

After curtailing its massive $4.5 trillion stimulus program in October of 2014, the Federal Reserve accomplished last December what it had set out to do at the beginning of last year - It finally raised short term interest rates. This was the first tightening move by the Fed in nine years and underscored its belief that the domestic economy was showing sufficient strength and inflation was rising back to its targeted threshold. With our fragile economic growth outlook and the increased volatility in the capital markets, we believe that the Fed will be hard pressed to raise rates in the first half of 2016.

The Fed is concerned that volatile capital markets and falling commodity prices will affect the outlook for inflation. The decline in oil prices, weakness in many emerging market economies and strong dollar are suppressing already low inflation expectations. Inflation has been running below the Fed’s targeted 2% level for the past three and a half years.

There are two types of inflation – price and wage inflation. Price inflation is the increase in prices of goods and services. As commodity prices continue to fall, it is more difficult for inflation to rise to the target levels since the raw materials that go into producing goods and services are declining. At this point in a recovery, we would expect to see pressure on wages; however, wage inflation is suppressed as well. With the low labor force participation rate, we are not experiencing wage growth in spite of the low unemployment rates. Evidence of the dismal rate of inflation, and some would argue deflation, are significant declines in the prices of commodities and financial assets.

With the increased volatility in the capital markets and the signs of economic slowing, we expect the Fed is on hold for most of 2016. Eventually the decline in oil prices will make its way through the consumer sector with lower oil and gas prices. This should be a catalyst for increased consumption which will ultimately spur growth. The Fed will likely be patient for fear of being the cause of any additional market turmoil. However, the Fed will be challenged to nudge inflation higher in the face of declining commodity prices and asset values. If the risk of deflation persists, we would not rule out anther quantitative easing program.

Does China Matter to Global Economic Growth?

The answer is yes. Over the past five years, the Chinese government helped to stoke its stock market to excessive valuation levels. Now, the government is putting up a chaotic effort to prove that there is a floor to how low stock prices will fall. China’s economy is slowing, its currency is falling, and the economy is experiencing capital outflows. At the same time the capital markets are stressed with too much leverage and still excessive valuations. In the absence of a turnaround in economic growth, we expect there will be more pain coming out of China this year.

While China is the second largest economy in the world measured by Gross Domestic Product (GDP), its economy and capital markets are managed through a centralized government. That is to say that China does not have capital markets where buyers and sellers come together that freely sets a price for a transaction. How much a business borrows, how much stock a Chinese citizen can sell, and the ability for a Chinese citizen to sell a stock short is controlled by the government through a seemingly arbitrary set of rules. China is paying for the excesses of its boom period, not unlike our build up in sub-prime housing which lead to our Financial Crisis in 2008.

As China built its economy in the last two decades, they were the marginal buyer for all commodities. The demand for steel, aluminum, copper and other commodities to build its roads, power plants and infrastructure, was a critical element to the increase in commodity prices. However, as their demand for commodities declines at the same time global growth slows, prices on commodities have fallen.

With China’s growing debt and excess housing and factory capacity, we expect China is on a path of continued weakening economic growth. In the past, China would ramp up its spending on infrastructure and provide easy credit during a slowdown. Today, it appears that it is attempting to weaken its currency, the Renminbi, in an effort to boost its exports as its traditional toolbox has been less effective at stimulating growth. The economic data reported by China is showing a growing service sector. This will ultimately provide balance to the economy as economic growth relies less on manufacturing output and more on consumption. However, we expect this transition will be hard given the high debt levels and lay-offs in the manufacturing sector.

Investment Strategy

Volatility creates opportunity. Over the past two years, the bright spot in the capital markets has been domestic large cap equities which have provided some of the best relative returns in publicly traded financial assets. Portfolio diversification into other asset classes seemingly has not worked as other sectors, including high yield, international, emerging market, and small cap stocks have underperformed.

Portfolio diversification is predicated on the mean reversion of investment returns. In today’s markets, we expect to be waiting a long time for investment returns to match the levels we’ve experienced over the past thirty years. Expected returns for financial assets, over the near term are low single digits at best and in some cases negative. This is a result of pushing valuations to excessive levels and this is most evident in the U.S. Treasury market.

So, then what does an investor do? How do you allocate your portfolio if expected returns are flat to negative? Portfolio diversification that ignores measures of valuation is irresponsible. Investment decisions must be based on underlying security valuations.

International

Global economic growth has been challenging since the Financial Crisis and the International Monetary Fund recently released projections which show expectations for the slowest rate of global growth since the Financial Crisis. The study highlights the erosion in growth particularly in the emerging economies.

The larger developed countries are in different stages of economic recovery. While the United States is showing the strongest growth, Japan and Europe are struggling under structural problems that are impeding massive stimulus efforts. Japan is the fourth largest economy measured by GDP and is struggling to show growth in its manufacturing sector and generate consumer demand under an aging population.

Europe has its own set of structural problems that are impeding economic progress. Last year, the European Union showed restraint toward austerity measures which allowed some relief to more indebted countries including Spain, Italy, Portugal and Cyprus. The European Central Bank initially embarked on a €1.1 trillion asset purchase program in March of last year and recently announced an expansion of that program which extends asset purchases into 2017. In addition, the Basel Committee recently announced a relaxation in capital rules which would have forced large banks to hold more capital against their trading business. While the rules are designed to discourage excessive risk taking, the freeing up of capital will allow for higher loan growth which will help private credit expansion in Europe.

Until the structural problems are addressed, we don’t expect either Japan or Europe to contribute materially to global growth. The monetary stimulus will help in the short term to prop up asset values; however, real economic growth is required to boost inflation expectations.

Increased debt levels in emerging economies following the end to quantitative easing has made it difficult for companies in these smaller economies to repay their debts. This is revealed in a reduced level of demand for goods and services and, ultimately slower growth in GDP in the emerging economies. We are nearing the end of the global credit expansion – for now.

Equity Strategy

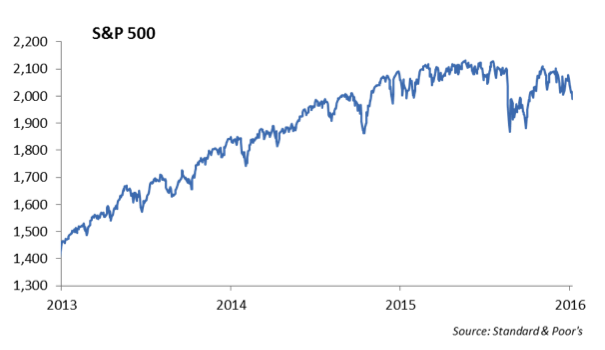

We expect performance in domestic equities to be challenged this year. Our thesis has been that the rally in stocks in the face of declining global demand and weak economic growth has been supported largely by aggressive monetary stimulus. The powerful rally from 2009 to 2014 has forced valuations to high levels from which significant positive rates of return will be difficult over the next few years.

While there is some downside risk at current valuations, there is still support for these high valuations given the large amount of money on the sidelines that is ready to come into the equity market. The earnings outlook is going to be challenged this year as margins compress and companies show little top line growth. Still, we expect near term support at the 1850 level on the S&P 500. Once investors recognize the buying power created by the decline in oil and gas prices, equity prices will reflect economists more optimistic growth prospects.

There have only been two times since the Financial Crisis that the S&P 500 has declined by 10% or more and each time there has been a strong rally. With the large amount of cash in the system, we believe there is a high probability for a similar market move in spite of the dismal global growth outlook. We would increase equity allocations below a 10% decline in value. At the same time, we would be reducing our equity exposure again if valuations returned to peak levels of last year.

There are solid companies that can be purchased at significantly cheaper prices today than a month ago based on the market movements. We are more constructive on the banking, industrial and technology sectors and we are underweight healthcare, retail and utilities.

We remain suspicious of both mid cap and small cap sectors. Without strong revenue growth and capital flowing into the small cap companies, the prospects for expanding revenues and businesses is reduced. We do not see lending to small cap companies increasing over the near term.

Fixed Income Strategy

We expect the general level of interest rates will remain low over the first half of the year given the volatility in the capital markets, low level of inflation and the challenges to domestic economic growth.

The volatility in the equity market will impact credit spreads in the bond market and we have seen spreads widen in general over the last six months. New issue corporate bonds will likely continue at last year’s pace with low interest rates and declining stock values.

In addition, we expect to see deterioration in credit quality, primarily in the energy and mining sectors. In turn, this will have a negative impact on banking and insurance which invest in the debt of these companies. There were more downgrades than upgrades by the rating agencies in 2015 and this trend will continue into 2016.

In investment grade credit, we believe there is value in integrated oil companies, high quality banks and diversified manufacturing. Long term, we generally are not favorable on issuers in the life insurance, exploration, oil drilling, and mining sectors.

With the recent weakness in the prices of high yield, we believe there is more value in the high yield space; however, investors must be careful around investing in energy credits. Assuming oil stays below $40 per barrel, we believe a significant portion of the debt rated below investment grade in the energy sector will need to be restructured this year. The sustained low level of the price of oil will reduce the asset values of these companies, which in turn will reduce the borrowing capacity the banks use to determine their liquidity facilities. Throughout the year, we expect to see announcements of reduced revolving loans as the value of collateral is reduced. In turn, this will pressure these energy companies to reduce leverage to comply with covenants.

With dealer inventories down 90% since 2007, liquidity in the bond markets is a concern. The bid-offer spread in general is widening and the ability to sell bonds requires a bit more patience today.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2016 Winthrop Capital Management