“And in the lonely cool before dawn You hear their engines rolling on But when you get to the porch, they're gone on the wind So Mary, climb in It's a town full of losers, I'm pulling out of here to win”

- Bruce Springsteen, Thunder Road

The Grey Owl investment process starts and ends with robust risk management. Our goal with the Grey Owl Opportunity Strategy is to provide equity-like returns, but with lower drawdowns and volatility than the major equity indices. As such, we worry about the downside first. We do not want clients to fear opening their monthly statements, and we certainly do not want to put regular withdrawals at risk, regardless of what the indices are doing. Over the almost nine years we have run the Grey Owl Opportunity Strategy, we have achieved our goals as the table below illustrates.

|

GO Opportunity |

S&P 500 (SPY) |

MSCI All World (ACWI/MXWD) |

|

|

Annualized Return |

5.65% |

6.59% |

3.75% |

|

Largest Monthly Loss |

-8.10% |

-16.52% |

-18.41% |

|

Largest Drawdown1 |

-25.78% |

-50.78% |

-54.93% |

|

Beta2 |

0.51 |

1.00 |

1.11 |

|

Sharpe Ratio |

0.50 |

0.41 |

0.23 |

Grey Owl Opportunity Strategy Risk Statistics (Nov 1, 2006 – Dec 31, 2015)3

2015 was a volatile year for risky assets. In the current environment, investor concerns are rising and volatility is picking up with them. To this end, we began positioning accounts more conservatively late in 2015. This meant trimming some positions and selling others, all in an effort to raise cash. This activity continued as we entered the new year, with the goal of preserving capital in the short-term to better position for long term growth. In the letter that follows we describe the indicators we use to assess risk and the macro economic variables we believe are contributing most to a fragile environment. First, here is the performance table for the Grey Owl Opportunity Strategy as of December 31, 20154:

|

Q4 |

YTD |

Cumulative Since 11/06 Inception |

|

|

Grey Owl Opportunity Strategy (net fees) |

-1.41% |

-0.49% |

65.50% |

|

Spider Trust S&P 500 (SPY) |

7.03% |

1.25% |

79.41% |

|

iShares MSCI World (ACWI and MXWD) |

4.82% |

-2.22% |

40.07% |

2015 – Large Capitalization Index Returns Mask Underlying Equity Weakness

High yield credit sold off in December of 2014, rebounded in January of 2015, and then spent the remainder of 2015 trading lower and lower. The high yield market led other risky asset classes down. When the year was finished, few asset classes and indices were positive. The S&P 500 was barely positive, and only because the largest companies receive larger weightings (it is a “market capitalization weighted index”). Four highflying technology names – the “FANGs” helped quite a bit. For comparison, an equal weighted index of the exact same 500 companies was down 4.1% for the year. Emerging markets and commodities suffered the most. The table below further illustrates the point.

|

Asset Class or Index |

2015 Total Return |

|

FANG (Facebook, Amazon, Netflix, Google) |

83.2% |

|

S&P 500 – US Large Cap |

1.4% |

|

Barclays Capital US Aggregate Bond |

0.6% |

|

MSCI All Countries World |

-2.4% |

|

S&P 500 Equal Weighted |

-4.1% |

|

Russell 2000 – US Small Cap |

-4.4% |

|

Markit iBoxx USD Liquid High Yield Index |

-5.0% |

|

Gold (GLD) |

-10.7% |

|

MSCI Emerging Markets |

-14.9% |

|

S&P Global 1200 Energy |

-22.3% |

|

S&P GSCI Commodities |

-32.9% |

The Multi-Decade Backdrop and the Current Environment

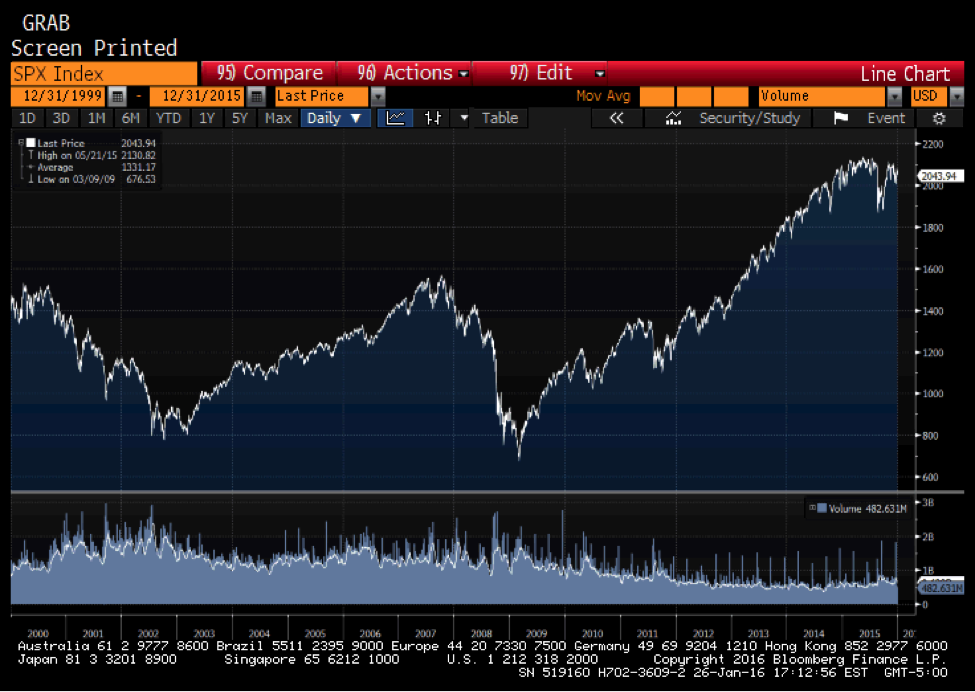

The 21st century began with US equities priced at extraordinarily high valuations. The Shiller PE ratio on January 1, 2000 was 44; today the ratio stands at 23. This compares to an average since 1900 of 17. The S&P 500’s meager returns – just 4.1% annualized, with TWO ~50% drawdowns – since the start of 2000 are largely a function of extended valuations reverting toward the historical mean.

Source: the Bloomberg

Despite this wild ride, today’s valuation is still high enough to portend another decade of weak returns – Research Affiliates currently forecasts 10-year real returns for the S&P 500 of just 1.1% per year.5

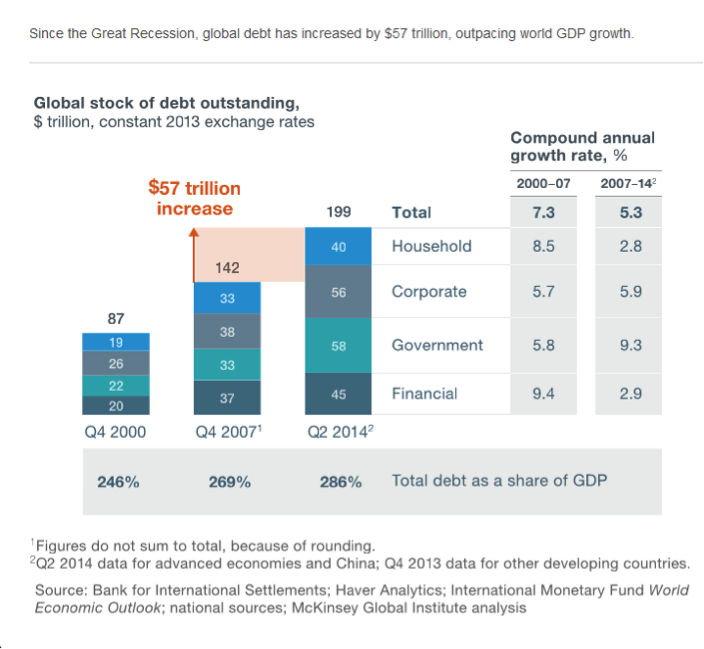

In addition, driven by central banks and profligate governments, global debt levels continue to increase dangerously beyond sustainable levels. Total debt in advanced economies has swelled to 286% of GDP in mid-2014 – up 40% since the end of 2000.

Debt is a drag on real economic growth and has a deflationary pull. US GDP has been growing at a decreasing rate for the past 65 years.

Source: St. Louis Fed's FRED

In addition, debt at these levels also introduces the risk of true debt monetization and commensurate inflation. Above all, high debt levels lead and have led to increasingly frequent booms and busts. (See the sixteen year S&P 500 above showing total return of the S&P 500 for the past sixteen years.)

High Valuations Meet Increasing Investor Risk Aversion

Equities valuations are stretched across numerous measures. Research Affiliates forecasts forward 10-year returns of just 1.1% annualized largely due to assumed mean reversion in valuations. The chart below shows a combination of four reliable valuation measures 69% above their historical average.

The macro-economic and valuation factors discussed above are important anchors, but their influence plays out over long periods. In the short-term, investor risk preference is far more important. Since the current cyclical bull market began in March 2009, investors have been highly risk-tolerant, even during four market corrections of 10% or more. In contrast, numerous signals are now telling us that investors are becoming increasingly risk averse.

What are the signs of increasing risk aversion today? At 1915, the S&P 500 trades below its 200-day moving average of 2022. The yield differential between low investment grade bonds (BAA rating) and the highest investment grade rating (AAA rating) – i.e. “credit spread” – has widened to 143bps from 100bps one year earlier, a clear sign that investors are becoming more risk averse.

Source: the Bloomberg

Stocks are also deteriorating below the surface of a market that is near its highs.

NYSE Advance Decline line failed to corroborate S&P 500 new high in July 2015 (Source: the Bloomberg)

In an early January 2016 commentary, Lowry Research wrote:

Historically, the deteriorating breadth that accompanies the formation of a major market top has been signaled by the failure of the market’s Adv-Dec Line to confirm new highs in the major price indexes. In fact, over Lowry’s 88 year history, there have been only three instances, in 1946, 1952 and 1976, when a major market top was not preceded by a divergence between prices and the Adv-Dec Line. During the first few months of 2015, Lowry’s OCO Adv-Dec Line confirmed each successive new bull market high in the S&P 500. That changed, though, in May, when the OCO Adv-Dec Line failed to confirm the May 21st high in the S&P Index. However, the divergence was minor and our report stated a more significant divergence would likely be needed to serve as a warning a major top was forming. And, in fact, just such a divergence occurred at the July 20th high when the S&P 500 virtually matched its May high, while the OCO Adv-Dec Line was significantly below its May peak. At the time, this divergence was noted as further evidence of the deteriorating breadth that typically occurs at the end of a bull market.

Current Opportunities

All of this calls for an increased focus on risk management. Importantly, it does not argue against owning individual securities with unique catalysts that can perform well despite the overall environment.

With the broadest possible mandate and a world with tens of thousands of securities, there are always attractive investments to own, even in a backdrop as challenging as described above. Properly hedged, we are optimistic about making money across our entire long portfolio, but particularly in the following five ideas with very distinct attributes.

- American Capital Agency Corp (AGNC) and Annaly Capital Management (NLY). Agency and Annaly are simple companies. Essentially banks, they borrow money short-term and buy (mostly) Federal Agency-backed mortgage bonds, earning a spread. Today, both trade at less than 80% of book value (i.e. one could liquidate today and earn an immediate 25%+ return) and yield over 12%. In addition, both act as a hedge we are paid to own. With a longer history, NLY has historically performed well in poor environments. In 2008, when the S&P 500 was down, NLY was flat, despite the fact that it began that year priced at 1.5x book value. (Compare that to far lower price to book value – 0.8x – today.)

- Priceline (PCLN). Priceline is the leader in the rapidly growing online travel agency (OTA) space. In the first quarter of 2015, partner hotels within the PCLN network grew 40% and gross bookings grew 26%. With OTAs commanding just 38% of the overall travel booking market, there is plenty of room to grow. The secular trend is so strong that PCLN should continue to do well even in a weak economic environment. In a strong economic environment, it should thrive.

- Wheeler REIT (WHLR). Wheeler is a microcap shopping center REIT with a 14% yield. Recently recapitalized, the firm fully deployed new capital to cover its dividend at year-end 2015. Recognition that this process is complete should provide a catalyst for the shares.

- Leucadia National Corporation (LUK). At $16/share, Leucadia is trading at just 72% of tangible book value of $22.30/share. Like Berkshire Hathaway, Leucadia is a diversified holding company with very opportunistic management. From 1990 through the Leucadia/Jefferies merger in October 2012, LUK shares provided investors a 13% compound annual growth rate. Jefferies (which now makes up about 50% of LUK) was even better at 16%. Both historical return profiles compare quite favorably to the S&P 500’s 8.5% annual return. Today, Leucadia is an orphan security with no coverage on Wall Street, but with an asset base and management team that bode well for the future.

Each of these securities has distinct attributes and risk factors that provide diversification among the five names6, as well as the rest of the Grey Owl Partners long portfolio. AGNC and NLY’s characteristics are particularly tuned to the current environment – the discount to book value offers a large margin of safety, a low-teen yield, and a business model that will do well should the global economy remain weak. Priceline is a growth stock with secular trends strong enough to continue through even weak economic times. Wheeler is a special situation microcap. Leucadia is just too cheap to ignore and management has a history of deal-making that could surprise the market with significant value creation at almost any moment.

Conclusion

Valuations remain high across asset classes and multiple indicators show increasing investor risk aversion. The Grey Owl Opportunity Strategy is conservatively positioned and holds significant cash balances. Our fixed income accounts have little credit risk and the largest position is in long-date US Treasury Bonds. Our partnership vehicle, Grey Owl Partners, has no net equity exposure. (Individual name shorts and market hedges offset sizable long positions, including those discussed above.) Finally, we have modest exposure to gold. All of these strategies are structured as all-weather portfolios tilted toward prevailing conditions.

From our perspective, most investors are still missing the significant paradigm shift that occurred around the turn of the century. Consequently, they remain ill prepared for the low return, high-volatility environment that has prevailed thus far in the 21st century - and which we believe will continue for the foreseeable future. It is hard to overstate how big a deal this is. With valuations high and increased government intervention, the old “buy-and-hold” approach is out of phase with the setting. We are optimistic regarding Agency, Annaly, Priceline, Wheeler, and Leucadia, but our confidence in owning these names is bolstered by our overall focus on capital preservation in the current environment.

As the Boss sang to Mary over forty years ago, sometimes you need to leave behind the conventional and embrace a new paradigm to win.

*****

If you know of an investor who cannot afford to sit in cash, but recognizes the systemic risk in the current global financial system, please ask him or her to give us a call. We believe our approach has the potential to allow investors to earn reasonable and consistent absolute returns while protecting against the time when the “stable disequilibrium” will eventually destabilize. With credit spreads widening, who wants to drive a fast car down a country road at night with no headlights?

*****

Sincerely,

Grey Owl Capital Management

Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The securities discussed above were holdings during the last quarter. The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

The performance information for the Grey Owl Opportunity Strategy presented in the table above is reflective of one account invested in our model and is not representative of all clients. While clients were invested in the same securities, this chart does not reflect a composite return. The returns presented are net of all adviser fees and include the reinvestment of dividends and income. Clients may also incur other transactions costs such as brokerage commissions, custodial costs, and other expenses. The net compounded impact of the deduction of such fees over time will be affected by the amount of the fees, the time period, and the investment performance. Grey Owl Capital Management registered as an investment adviser in May 2009. The performance results shown prior to May 2009 represent performance results of the account as managed by current Grey Owl investment adviser representatives during their employment with a prior firm. THE DATA SHOWN REPRESENTS PAST PERFORMANCE AND IS NO GUARANTEE OF FUTURE RESULTS. NO CURRENT OR PROSPECTIVE CLIENT SHOULD ASSUME THAT FUTURE PERFORMANCE RESULTS WILL BE PROFITABLE OR EQUAL THE PERFORMANCE PRESENTED HEREIN. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable. For additional performance data, please visit our website at www.greyowlcapital.com.

The indices used are for comparing performance of the Grey Owl Opportunity Strategy (“Strategy”) on a relative basis. Reference to the indices is provided for your information only. There are significant differences between the indices and the Strategy, which does not invest in all or necessarily any of the securities that comprise the indices. In addition, the Strategy may have different and higher levels of risk. Reference to the indices does not imply that the Strategy will achieve returns or other results similar to the indices. The performance shown for the iShares MSCI World Index Fund (“Fund”) includes performance of the MSCI World Index prior to March 26, 2008, inception date of the Fund.

1 On a monthly basis.

2 To the S&P 500.

3 All statistics are calculated based on the same representative account(s) used to calculate performance. They are calculated by GOCM using standard formulas.

4 For more information regarding performance, please refer to the performance disclosure at the end of this letter.

5 http://www.researchaffiliates.com/assetallocation/Pages/Core-Overview.aspx

6 December 31, 2015 percentage holdings in: Grey Owl Opportunity Strategy; AGNC 5.4%, LUK 3.4%, PCLN 6.9%, WHLR .4%; Tax-exempt accounts; NLY 5.4%.