In a classic 1984 film, “Revenge of the Nerds,” a group of out-of-favor college students (“nerds”) assert themselves at the expense of highly-esteemed fraternity athletes and popular sorority girls. Here is how imdb.com describes the movie on their website:

“At a big campus, a group of bullied outcasts and misfits resolve to fight back for their peace and self respect.”

As stock pickers and long-duration common stock owners, we at Smead Capital Management believe in some very “nerdy” truths in our discipline. One of those truths is that valuation matters dearly. We believe that truth could reassert itself in the stock market in 2016.

The history of the U.S. stock market follows very closely with the classic 1984 film. Academic studies show that cheap, out-of-favor stocks typically outperform more expensive ones over both one-year and longer holding periods based on P/E ratios, price-to-book ratios, price-to-sales, price-to-cash flow and price-to-dividends. The chart below shows David Dreman’s long-term P/E ratio study (on an annual rebalancing basis):

Cheap stocks are the outcasts and misfits of the S&P 500 Index and had an abnormally rough time in 2015. The S&P 500 is a capitalization-weighted index. This means that the index got an unusually big price performance boost from highly esteemed and popular futuristic companies. Super popular stocks like Facebook (FB), Amazon (AMZN), Netflix (NFLX) and Google (GOOG), the so called “FANG” stocks, drastically outperformed the S&P 500 in 2015. Since these were already sizably weighted in the index at the end of 2014, they had an inordinate effect on the final numbers. The New York Post explained the situation this way in a January 2nd website article:

“For starters, not one of the FANGs pays a dividend. Sure, dividends are nice, but who wouldn’t prefer a stock that is up 37 percent in a year like Facebook? Or an Amazon, soaring a 123 percent? Or Netflix, catapulting 144 percent, or Google, up 48 percent?”

We can answer their question. Everyone who invests in U.S. stocks would have preferred to have had their portfolio over-weighted in them last year. Why do we have to resist the temptation to own highly esteemed and popularly priced high-P/E ratio stocks on a historical basis? Secondarily, why do the studies show that cheap stocks outperform over time?

The laws of economics dictate that high profit margins invite competition. Fat profit margins and explosive sales growth draws new players and economic theory says that new competitors will keep coming until marginal profit moves to zero. If competition doesn’t rear its ugly head at some point, the anti-trust department of the U.S. will judge the company to be a monopolist and ask for it to be broken up. Just ask Microsoft about what happened back in 1998. It is no fun to be accused by the U.S. government of being a monopolist.

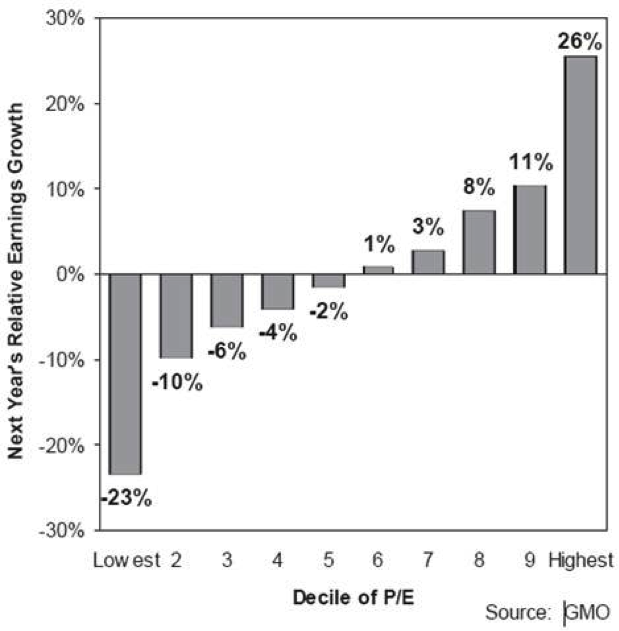

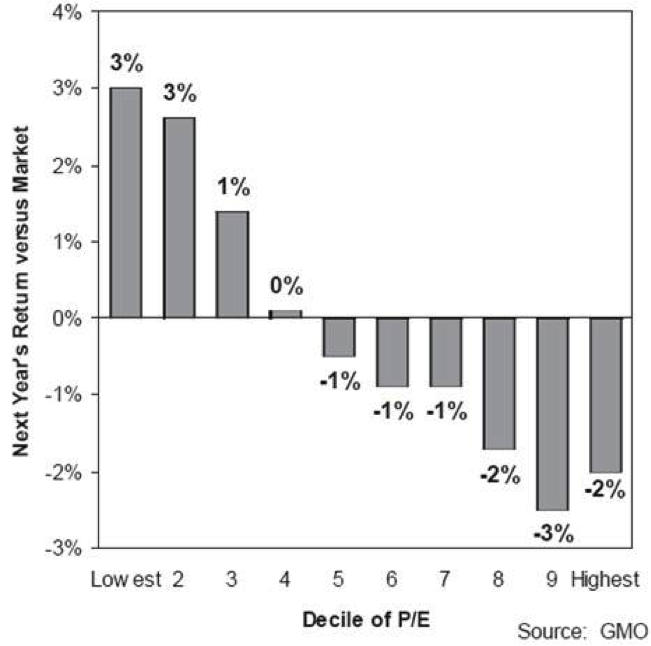

Cheap stocks outperform because the expectations attached to them are very low and nobody is anxious to get into the business with them. See the charts below:

Wall Street analysts are very good at deciding whose earnings are going to grow the most. The lowest P/E stocks see significant average earnings contraction, while the glam stocks with the highest P/E ratios see very high and above-average growth. On to the next chart:

Stocks with the highest earnings expectations underperform the averages in the next 12 months and those which had the lowest expectations for earnings growth gained a big return advantage on the index.

A review of history shows that most of yesterday’s highly-esteemed and popular favorites didn’t stand the long-duration test of time. Conglomerates like LTV and Gulf & Western were hot stocks in the mid-1960s. Levitz Furniture (with their warehouse stores) was the Amazon of 1968. Polaroid had the highest P/E ratio (90x) and was the most favored of the Nifty-Fifty stocks at the end of 1972. They went bankrupt in the early 2000s.

In 1980, Fluor and MCI Communications were “the bomb,” and in 1992, Wal-Mart had a very high relative P/E ratio and appeared unstoppable. Finally, Yahoo and AOL were big favorites and the envy of the “misfits and outcasts” which were on the low P/E ratio list in 1999.

We have been emphasizing the lowest P/E ratio and price-to-free cash flow stocks in our portfolio and continue to avoid stocks which have a high degree of popularity. We believe that these “nerds” could outperform in 2016. Below is the list of our cheapest portfolio stocks based on consensus 2016 First Call estimates:

- Gilead Sciences (GILD)

- AFLAC (AFL)

- Gannett (GCI)

- JP Morgan (JPM)

- Bank of America (BAC)

We have confidence that these “nerds” offer above-average return potential and have very low expectations attached to them. Popularity is fleeting at college and it has been historically in the U.S. stock market as well.

Warm Regards,

William Smead

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

This Missive and others are available at www.smeadcap.com.

Follow us on Twitter @SmeadCap