The price of oil has had a dramatic effect on markets since the start of the year. WTI was down over 9.0% in January and domestic markets followed oil downwards, returning approximately -5.0% the first month of this year. In an effort to break through the noise surrounding oil, HiddenLevers recently analyzed the commodities market and in this post will summarize the good, bad and ugly outcomes for oil and its broader effect on the global economy.

The Good – Commodities Bounce Back

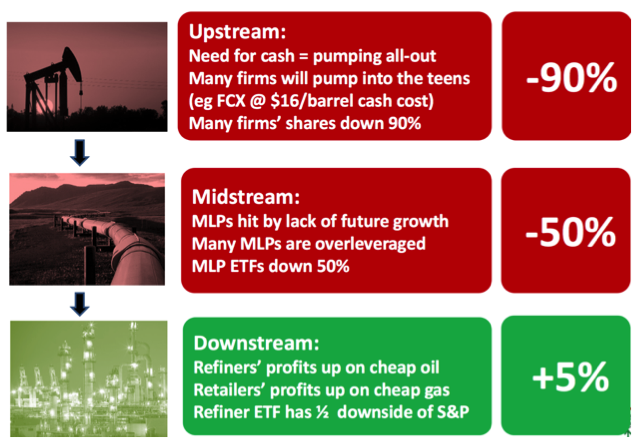

Evolving technologies like shale fracking have reduced the cost of new oil production, but oil at $30/barrel makes US production unprofitable for many suppliers (on a GAAP basis newer wells can’t profit below $60/barrel). If domestic producers cease operation, supply will decrease and the cost of oil will appreciate. A strong dollar and slowing growth in China has also played a huge role in the most recent decline in oil prices. A reversal of this trend would benefit oil producers.

The Bad – Isolated crash

As emerging market economies have begun to slow, their demand for oil has declined as well. Countries like China and India gobbled up oil and petrochemicals over the past decade. High oil prices encouraged high cost producers to drill more wells domestically and profit from triple digit crude prices. Unfortunately, waning demand in China and increasing efficiencies across the globe have decreased demand for crude. Meanwhile, supply has continued to balloon as high cost producers continue to pump oil to try and remain solvent. This scenario is now completely priced into the market as oil prices have fallen 70% since 2014 while equities have been relatively flat over the same time period.

The Ugly – Commodities Perfect Storm

The beginning of this year gave us a preview of a what a Commodities Perfect Storm might look like. Equities and oil moved in lockstep when both sold off over concerns of slowing global growth. If the Chinese market continues on its bearish path it will push demand for petroleum even lower. Additionally, if the Fed keeps its promise of multiple rate hikes the dollar may appreciate further – putting additional pressure on the price of crude. A rising dollar, weakness in China and Tehran’s return to the global oil market create the perfect storm for lower crude prices along with a bearish equity market.

Unlike 2014, Oil and domestic Equities have moved in lockstep since last November

What is next for oil?

While oil bulls point to impending US production declines, many US producers have hedges in place through 2016, making a short-term pull back in production unlikely. Additionally, any OPEC deal to cut production may be offset against Iran’s return to world markets (bringing up to 500k/bpd online this year). While these factors sound bearish, oil prices have changed rapidly over the last decade on the basis of small changes in the supply/demand balance. With the market only oversupplied by around 1% of global demand, oil prices could rebound quickly if the gap is closed. Advisors who want to guard against volatility in the energy sector need tools to stress test portfolios against commodity shocks and identify hedges in volatile markets.