The drop in global oil prices to their lowest levels in more than 10 years might seem like good news for consumers, but the markets have been spooked because the reasons behind the decline—and the potential implications—are not so clear. Three investment professionals at Templeton Global Equity Group, Cindy Sweeting, Tony Docal and Chris Peel, explain what they see happening in oil, whether they think oil prices will recover and what a lower-oil-price environment might mean for investors. They note that oil prices tend to be self-stabilizing, and when drilling down to the company level, lower prices could prove a boon for the stronger players—and for investors looking for value plays.

Clearly, collapsing oil prices have caused financial disruptions and there will likely be bankruptcies and credit events among overleveraged and high-cost producers. However, this can actually be a boon for the better-capitalized oil companies which can then buy distressed competitors and the reserve assets rather than having to shell out on exploring greenfield sites for new sources of oil.

Investors are now almost unanimously assuming a vicious circle, whereby collapsing oil prices cause a global slowdown, which leads to even weaker energy demand and further oil price declines. But history and economic analysis both point to a self-stabilizing process as cheap oil supports economic activity and modestly boosts energy demand. Lower oil prices and their restraining impact on inflation also signal that global central banks will likely remain accommodative, in our view. So the sharp fall in oil prices has certainly been disruptive, but stabilization from distressed trough levels should be good for economic growth even if the price of oil doesn’t rebound back to peak levels of above $100 a barrel in 2014.

Oil prices are a symptom of the markets’ continuing worry that manufacturing trade and capital spending are stagnant despite massive liquidity injections from the developed-world central banks. The reality—at least as we see it—is that the global economy is still slowly working through the deflationary impact of the unwinding of excess capacity and excess supply. This is not new news; too much productive capacity was built globally to serve the unsustainable demand that was bolstered by excessive leverage, and the pain of retrenchment is working its way gradually through the global economy. We expect this to continue.

So with the modest-at-best global recovery after the still front-of-mind global financial crisis trauma from 2008-2009, markets are understandably preoccupied with the scope for unpleasant shocks, particularly given that expansion in the developed economies is now approaching a seventh year. These shocks range from a hard and bumpy landing in China to a potential recession in the United States as the oil and manufacturing sectors face some duress and as the unsubsidized price of money again enters into the equation.

Geopolitical Impacts

Geopolitical risks are also clearly mounting as the Middle East is certainly in a fragile state right now. If we think about what’s going on in the region today, the list is certainly long—from the conflicts we see in Syria, Yemen and Libya, to the rise in terrorism and more recently the increasing tensions between Iran and Saudi Arabia. The oil price collapse puts significant pressure on Middle Eastern geopolitics. Lower oil revenues in exporting nations have prompted governments to take actions to protect their fiscal positions. Currencies pegged to the US dollar are also starting to come into focus, with speculation that some of these pegs may break should we see persistent downward weakness in oil prices. For the most part, though, the large oil-exporting countries in the Middle East built significant financial reserves when oil prices were high and have little debt in relation to gross domestic product (GDP), so we think they should be able to withstand a period of lower oil prices, although not indefinitely.

Iraq, Iran, Libya and Saudi Arabia together produce roughly 20% of the world’s crude oil. Yet, there seems to be little if any geopolitical premium built into oil prices at the moment. Should tensions escalate further and lead to any other oil outage, the current buffer of global oversupply could be reversed pretty quickly. This is not our base-case expectation; however, it certainly remains an upside risk for oil, which we think currently is not being priced in.

How Low Could Oil Go?

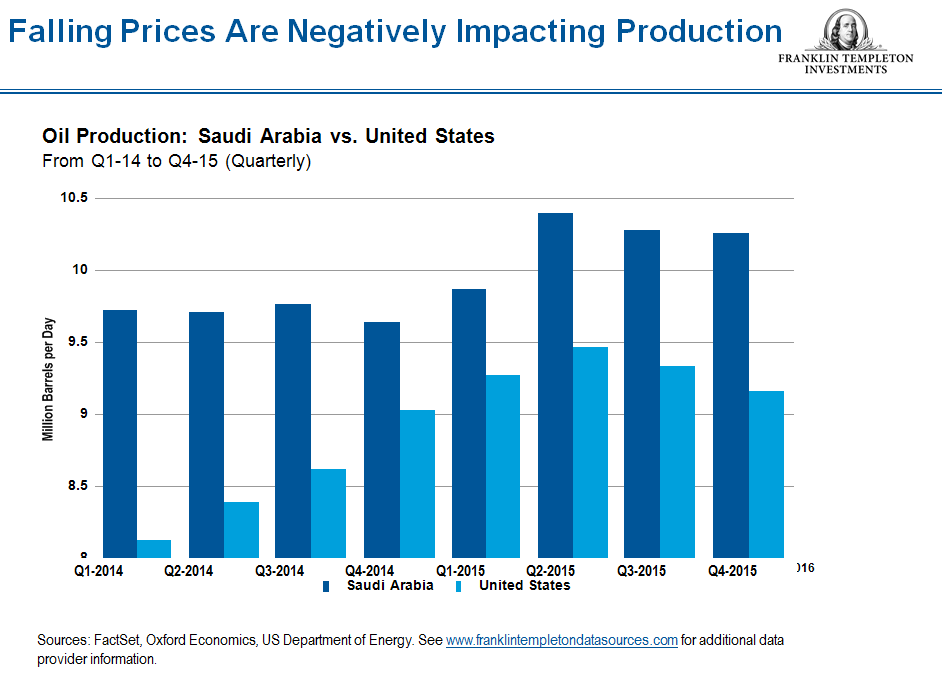

We know there are a number of factors contributing to the oversupply of oil currently. Successful US shale production over the last few years combined with the decision of the Organization of the Petroleum Exporting Countries (OPEC) and Saudi Arabia in particular not to cut production has added to an already oversupplied market. And, there’s more potential supply pending Iran’s return to the market following the lifting of sanctions. For oil prices to normalize, this excess production needs to be removed from the market somehow.

Still, we think the oversupply situation needs to be put into context. Various estimates today show a global oversupply of somewhere between 1 million to 1.5 million barrels a day of oil. Considering roughly 94 million barrels a day are consumed around the world, that oversupply is roughly 1%–2%,1 or just one year of demand growth at current rates. This is far lower than where the market was in the 1980s when OPEC and Saudi Arabia adopted a similar market share strategy.

With managed decline rates of roughly 4%–5% in the existing oil wells and declining industry investment, we think it’s inevitable that oil supply and demand will come back into balance at some point in the future. But in the short term, we believe the price of oil may need to fall to a level that forces excess supply off the market. This is happening today, although it’s taking longer than many have expected. Many investors wonder how low prices can go. In our view, the lower the price of oil goes in the short term, the quicker the rebalancing process should happen because it becomes uneconomical for some producers to even keep current oil production online. There are forecasts of oil prices falling to $20 a barrel, which is certainly possible, but at that level a decent amount of crude oil is losing money on a cash basis, so we would likely see a stronger supply response than we have seen so far.

In terms of overall industry investment, according to our analysis, global exploration and production capital expenditure (capex) likely fell in 2015 and is expected to decline again in 2016. That would mark the first time in at least three decades that the oil industry has registered two consecutive years of investment decline.

As previously noted, major sovereign producers do not have the financial resources to tolerate low oil prices indefinitely. Saudi Arabia, Russia, Brazil and Venezuela (key oil exporters) are all experiencing significant budgetary shortfalls attributed to lower oil prices. Although some countries have more financial reserves than others, stresses are already being felt in the market.

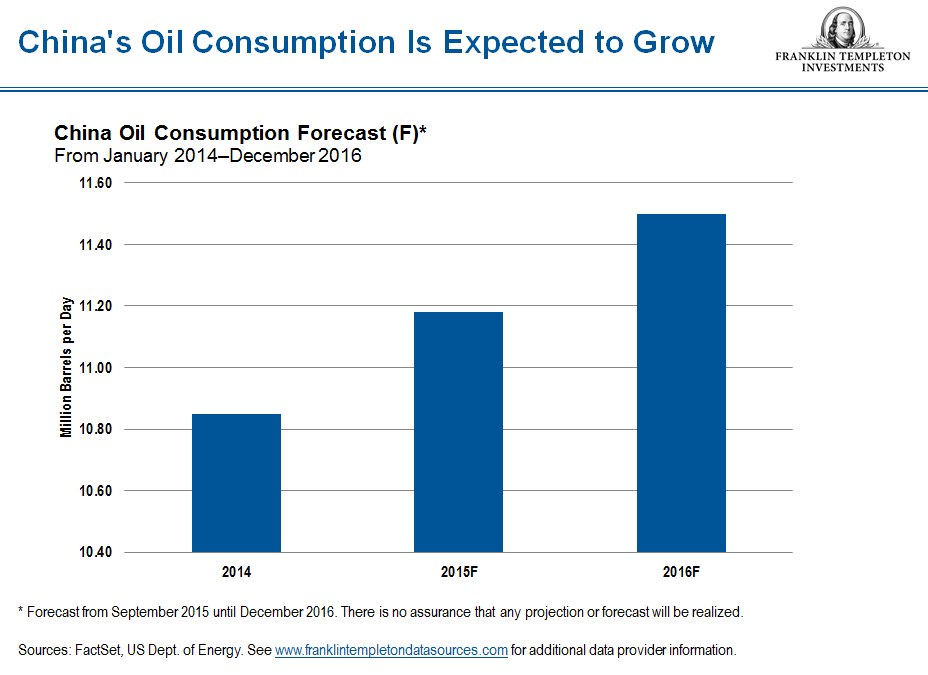

So over time, we see the market re-adjusting from a world of oversupply to balanced and then potentially undersupplied farther out. At this point the oil price will need to rise to a level that will promote additional production to come back online in order to replace the natural decline rate and satisfy future demand growth. When might this happen? Our expectation as we move through 2016 and into 2017 is that the supply and demand imbalance will slowly erode through a combination of reduced production and increased demand growth.

Finding Values in the Energy Sector

Given the stress we have seen on oil prices in the market, we have also seen a similar stress on oil-industry companies. We have been finding decent value within the energy space, and in some cases we have been presented with valuation levels that we have not witnessed in decades. We have found major integrated oil companies with solid balance sheets and sizable dividends that we believe should be able to navigate the market uncertainty and also potentially benefit from the cost deflation and capital discipline over time. On the other end of the spectrum are the US exploration and production companies and the service companies that are highly correlated to the oil price and should benefit greatly once supply and demand normalizes—and the US shale industry is one we think could recover first. That said, we are very selective right now, because of course we want to be positioned in what we believe will be the survivors.

We’ve certainly witnessed a good dose of New Year gloom fueled by the many proximate risks that seem imminent to some market participants. However, sentiment swings drive the short-term voting machine of the market. The ongoing challenge is to stay unemotional, balanced and objective, remaining focused on the longer-term fundamentals and waiting for the time positive surprises come and sentiment shifts.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered Individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Cindy L. Sweeting, CFA

Director of Portfolio Management

Templeton Global Equity Group®

Antonio (Tony) Docal, CFA

Deputy Director of Research

Templeton Global Equity Group®

Chris Peel, CFA

Portfolio Manager, Research Analyst

Templeton Global Equity Group®

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Value securities may not increase in price as anticipated, or may decline further in value. To the extent a portfolio focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a portfolio that invests in a wider variety of countries, regions, industries, sectors or investments. Investing in the natural resources sector involves special risks, including increased susceptibility to adverse economic and regulatory developments affecting the sector. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors.

____________________________________________________________________

1 Source: US Energy Information Administration, data as of fourth quarter 2015.

© Franklin Templeton Investments

© Franklin Templeton Investments