An effective strategy for judging stock market psychology comes from looking to see which outstanding stock pickers are being singled out for criticism. This happens when they underperform the S&P 500 Index and are invested in out-of-favor parts of the stock market. This also happens when the stock market is limiting its favor to a narrow group of futuristic companies and the historically smart stock picker is not willing to bend their will to the current trend.

Bill Miller beat the stock market for 15 straight years and became admired for what we believe he is: a great stock picker. He reached his low point in 2011 when his bets on economically-sensitive home builders, banks and airlines caused him to temporarily lose sizable money in the U.S. stock market. Here is a quote from an article in the Wall Street Journal on November 18th of 2011, titled “The Long Climb and Steep Descent of Legg Mason’s Top Stock Picker”;

In a business that thrived for decades by nurturing the cult of the star stock picker, no star had sparkled more brightly than Mr. Miller's—or fell to earth with such a thud.

His difficult circumstance and media criticism in late 2011 was one of many clues for us that we were reaching a point of maximum pessimism in U.S. stocks. Along with favorable fundamental factors, we plugged our nose as lonely contrarians and bought banks and looked for ways to participate in home building through companies which fit our eight criteria for stock selection. Bill Miller’s portfolio doubled in value from the beginning of 2012 to the end of 2013, no surprise given the level of criticism.

Warren Buffett is arguably the best stock picker of all time. He has compounded the investment of his and fellow shareholders in Berkshire Hathaway at 20% per year on average since he took it over in 1965. In our view, he is the best stock picker and business analyzer in U.S. history. Despite this deserved respect and the high regard he is held in, here are recent (Q4 2015) headlines which describe his current portfolio of common stocks:

- “Buffett’s Really Bad Week”

- “3 of Warren Buffett's Top Holdings Trading Near 1-Year Lows”

- “Warren Buffett's top stocks are dogs this year”

For those who haven’t followed his career, some important background would be helpful. This is not the first time that Buffett has been criticized and appeared out of step with prevailing wisdom on Wall Street. In 1969, he closed his partnership (hedge fund) because the U.S. stock market appeared out of kilter and he wasn’t finding the kind of bargains he believed could produce outstanding long-term returns. The 1973-1974 bear market in stocks proved him prescient and laid bargains like the Washington Post and See’s Candy in front of him.

In 1999, Buffett spoke at the Sun Valley-based Allen and Co. conference amid big concerns that he had completely lost his stock-picking touch. Everything internet-related had gone wild and stock market pundits felt that the kinds of “old economy” companies which Buffett liked were ill-prepared to succeed in a tech-dominated world. Ironically, his talk in Idaho explained why all those riding high from the tech bubble were going to get their head handed to them. They soon did, and Buffett’s portfolio rallied against the indexes and put him back in the usual high esteem.

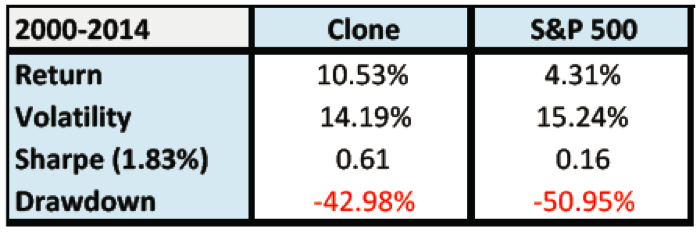

The months surrounding the peak of the tech bubble in 1999-2000, when Buffett was getting filleted in the press, was a great time to invest in Berkshire Hathaway and buy Buffett’s stock portfolio. A recent MarketWatch article analyzed how Buffett’s stocks did from 2000-2014:

Source: http://www.marketwatch.com/story/how-to-piggyback-on-warrenbuffett-and-other-legendary-money-managers-2016-01-06. Data from 1/1/2000 - 12/31/2014. Past performance is no guarantee of future results.

Source: http://www.marketwatch.com/story/how-to-piggyback-on-warrenbuffett-and-other-legendary-money-managers-2016-01-06. Data from 1/1/2000 - 12/31/2014. Past performance is no guarantee of future results.

Why is Smead Capital Management telling you this story and doing so at this time? First, we own Berkshire Hathaway shares in our portfolio. The stock underperformed the S&P 500 in 2015 and trades very close to 1.2 times book value. Buffett has said, and Vice Chairman Charlie Munger has reiterated, that Berkshire Hathaway would buy back shares at 1.2 times book and in some ways put a floor underneath the stock if it fell that far.

We believe that Berkshire Hathaway is undervalued and symptomatic of recent criticism Buffett has received. Buffett has positioned the company to benefit from the rebound in the U.S. housing market. Berkshire Hathaway owns the second-largest residential real estate brokerage firm, two of the three largest banks, the largest manufactured home builder (Clayton Homes), Shaw Carpet, Benjamin Moore Paint, Acme Brick, Burlington Northern Railroad, Mid-American Energy, Marmon Group and many other companies which would thrive if housing makes a big comeback in the U.S.

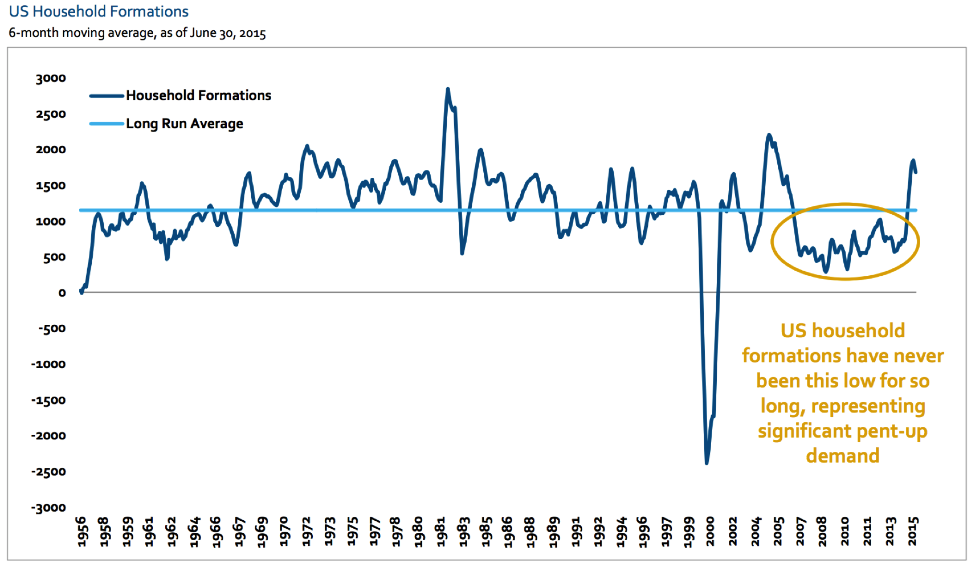

Most portfolio managers and indexes are poorly positioned to make money from a rebound in housing and a much stronger U.S. economy. Look at the chart below:

Source: Bloomberg. Past performance is no guarantee of future results.

Source: Bloomberg. Past performance is no guarantee of future results.

Buffett can see that household formation was worse from 2007-2013 than it had been in nominal terms since the early 1960’s when the U.S. population was only 180 million people. We have 325 million people today (unless Donald Trump orders a large number to leave in 2017) and our largest population group happens to be at the age that households are formed. We view this as a five-standard deviation statistical anomaly because in the early 1960s the greatest generation was about done having kids and the baby boomers weren’t yet old enough to do so. Hence, the dearth of nominal households back then made complete sense. The paucity of household formations this time came from the perfect storm of the worst financial meltdown since the 1930s combined with a secular change in the age of marriage and first children in the U.S.

Second, the fact that Buffett’s stocks are deeply out of favor speaks volumes to the psychology of the stock market as we enter 2016. Buffett is getting hit hard with criticism on American Express, IBM and Bank of America. Sounds very much like the same ridicule Bill Miller got in 2011. American Express has had some of its own issues with Costco, IBM has had severe currency headwinds and is changing the mix of their business, and Bank of America continues to be dragged down by regulatory issues and historically-depressed interest rates. In the late 1960s, Buffett was faced with the development of the Nifty-Fifty. This was a group of seemingly invincible companies whose earnings growth looked uninterruptible, which had ultra-high P/E ratios and Buffett wasn’t willing to own. Almost nothing else in the U.S. stock market besides them worked between 1970 and the beginning of 1973. In 1998 and 1999, nothing seemed to work except for tech stocks and Buffett didn’t find anything there that interested him.

Today, we have a narrow market like those two previous junctures. A recent report shows that you lost money in the S&P in 2015 if you didn’t own 10 glamour stocks which had stunningly good years. Among them were Facebook, Amazon, Netflix and Google, affectionately called the “FANG” stocks. Much like the previous times when Buffett’s approach fell out of favor, high P/E ratios and massive faith in the future are invested in these glamour favorites.

Value investors need to buy inexpensive and meritorious companies which do much better than the low business expectations attached to them. Academic studies have proven that buying inexpensive common stocks with low expectations outperform over one- to seven-year holding periods. Buffett has made a career out of doing this.

Low business expectations are attached to companies which appear to be losers from Amazon taking everyone else’s business in online commerce. Netflix is supposed to kill everyone in the cable and network TV business. Facebook and Google are supposed to be grabbing the advertising dollars which used to go to “old economy” newspapers, magazines and TV channels. Therefore, as of December 31st 2015, you paid an average of 350 times last twelve month earnings for these glamour stocks and 10-15 times earnings for the companies which they are supposed to destroy.

History has been cruel when the maniacal affection for expensive stocks with bright futures gets broken. Many of the Nifty-Fifty stocks lost 60-90% of their value in the 1973-1974 bear market and tech stocks lost 80% of their value on average from March of 2000 to March of 2003. Buffett didn’t look like he’d lost his touch once the high-priced favorites got their comeuppance.

Where does that put us as we look out into 2016? Buffett’s privately-owned and publicly-traded businesses are clearly out of favor and could remain that way until the infatuation with glamour stocks is hitting the wall. We choose to prepare well ahead of time, especially when it comes to undo risk in expensive common stocks. Our old adage is, “If there’s going to be a hurricane in Miami, we don’t want to be in Palm Beach!”

As long-duration common stock investors, we like Buffett’s American Express, which could return to favor later on and reward us for getting involved. They are having very high acceptance from 25-35 year old credit card users and dominate households in the U.S. with over $100,000 annual income. Their balance sheet is powerful, return on equity is excellent even in the middle of the current difficulties and their P/E ratio is nearly half that of Visa and MasterCard.

We like eBay and Nordstrom, whose businesses are supposed to get severely damaged by Amazon. Both are very reasonably priced with very-addicted customer bases and a growth strategy where the expenses are frontloaded and the benefits can go on for years.

We like Tegna, Gannett and Comcast, which Netflix, Alphabet (Google) and Facebook are supposed to be terrorizing. These businesses gush free-cash flow and a recent study has shown that TV/newspaper advertising is proving to be much stickier than internet-related ads.

Lastly, we like betting alongside Warren Buffett on housing making a big comeback over the next five years. We see it benefitting NVR, the fifth-largest home builder and a builder of starter homes in 15 states. We like mortgage loans and the pickup in velocity of money that housing demand could cause, which would benefit Bank of America, JP Morgan and Berkshire Hathaway. Thank you for your confidence and trust in our investment discipline.

Smead Capital Management, Inc. (“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Washington. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the Publications.

For additional information about SCM, including fees and services, send for our disclosure statement as set forth on Form ADV from SCM using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

This Missive and others are available at www.smeadcap.com.

Follow us on Twitter @SmeadCap