KEY TAKEAWAYS

· EMD valuations have cheapened notably to start 2016, matching the lows set in August 2015, but fundamental issues such as falling commodity prices and Chinese economic concerns remain headwinds.

· Though potential trouble spots, such as Venezuela, exist, markets are not expecting a widespread increase in emerging markets defaults, based on the change in CDS cost over the past year.

Emerging markets debt (EMD) valuations have cheapened in recent weeks, as weaker Chinese economic data and lower oil prices pushed prices lower and yield spreads higher. The average yield spread closed at 4.6% on Friday, January 15, 2016, essentially matching the post-recession peak of August 2015 [Figure 1]; and the average yield to maturity rose to 6.25%, the highest since mid-2011 and the height of European debt fears. The 4% yield spread level has been an indicator of value since the end of the recession, as the average yield spread has rarely remained higher than 4% for long. This level has tended to be an inflection point during the post-crisis area, where buying interest has generally started to emerge. But is now the time to buy, or are wider spreads an indication that markets are concerned about recession and default risks?

Many countries are grouped under the emerging markets heading, but differences in size, growth rates, major exports, and financial conditions are significant. A closer look at three common headwinds for emerging markets countries—commodities exposure, China economic linkages, and dollar-denominated debt levels—may help assess true underlying risks.

COMMODITY EXPOSURE

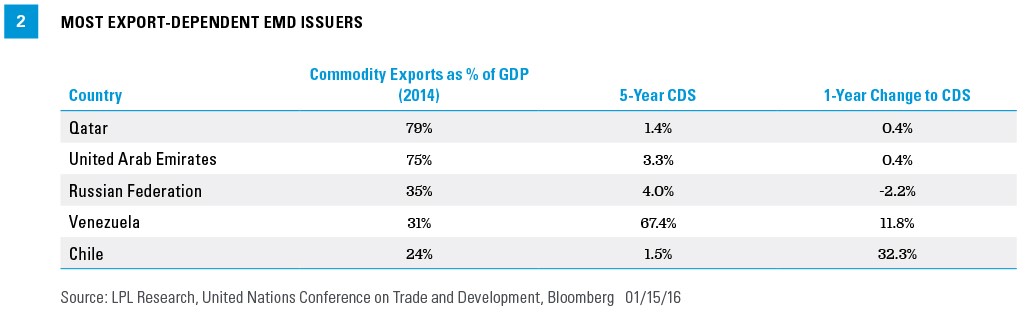

The sharp drop in commodity prices has pressured EMD, and countries that have heavy exposure to oil and mining-related exports (such as Chile) have been among the most impacted. Figure 2 shows the most export-dependent countries as of the end of 2014. The numbers are reported as a percentage of gross domestic product (GDP) to correct for size differences. The change in the cost to insure against default, measured by credit default swaps (CDS), is also shown to reflect changing market risk expectations.

Most countries have seen some increase in CDS cost over the past year; but only one country, Venezuela, which was already troubled, has seen a significant increase, meaning the market is pricing in a higher potential for default. Note that Russian risks increased substantially over the past few weeks, but the change over the prior year is a bit deceiving. A year ago, peak tensions in the Russia-Ukraine conflict led to a spike in Russian CDS spreads, which subsequently settled down leading to a decline for the past 12 months. Still, the absolute level of 4%, although higher over the past few weeks, is modest.

A credit default swap (CDS) is designed to transfer the credit exposure of fixed income products between parties. The buyer of a credit swap receives credit protection, whereas the seller of the swap guarantees the credit worthiness of the product. By doing this, the risk of default is transferred from the holder of the fixed income security to the seller of the swap.

Commodity prices are certainly a headwind for some nations, but on their own are not likely enough to significantly increase the broad default risk. With the exception of Venezuela, many EM countries have financial strength to withstand lower commodity prices. This is especially true of Qatar and the United Arab Emirates, rich countries where 18 months of low oil prices are unlikely to create significant default risks. The cost to insure Saudi Arabia against sovereign default increased from a trivial 0.6% in mid-2015 to 2.0% at the end of last week, which remains low on a stand-alone basis.

Still, the five countries below represent roughly 20% of EMD issuers and reflect how broadly lower commodity prices are impacting EM issuers.

EXPOSURE TO CHINA

China’s economic slowdown poses a potential threat due to its sheer size and economic ties with many EM nations. Those countries with the most exposure to China are shown in Figure 3, and all have seen an increase in CDS spreads—though only one, South Africa, has seen an increase of more than 1%.

DOLLAR-DENOMINATED DEBT

The vast majority of EM countries have debt burdens that are more manageable than their developed counterparts, but because the bulk of EMD is issued in U.S. dollars, lower commodity prices and a stronger dollar present a double whammy for some EM countries. Commodity exporters are not only suffering from lower commodity prices, but their debt burden—denominated in U.S. dollars—is increasing. Figure 4 identifies the five countries with the largest government dollar-denominated debt burdens, local currency performance versus the dollar in 2015, as well as the most recently reported foreign reserves, which provide one snapshot of a country’s financial resources.

Venezuela stands out again with a high level of dollar-denominated debt and limited resources (via a low level of foreign exchange reserves) to weather current conditions. Most other countries have seen limited change in their market perceived risk simply due to dollar strength but, excluding Venezuela, the other four countries in Figure 4 represent an additional 9% of EMD issuers, reflecting the breadth of this headwind.

BRINGING IT ALL TOGETHER

With the exception of Venezuela, most EM countries are financially able to withstand current challenges, and market perceived risk, as measured by CDS, remains controlled for now. However, the challenges posed by lower commodity prices, China’s economic slowdown, and dollar-denominated debt levels affect a significant portion of the EMD market. Add in China, representing roughly 15% of the EMD market, and Brazil (8%), which is dealing with its own severe recession, and the breadth of the EMD challenge is noteworthy—even amid resilience from stronger issuers from South Korea, Indonesia, and India. While markets may not be pricing in widespread default, lower commodity prices, China, and U.S. dollar strength may remain headwinds for EM countries in the near future, meaning that it may be a little early to call the all clear on EMD, even though valuations are more attractive.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Investing in foreign fixed income securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with foreign market settlement. Investing in emerging markets may accentuate these risks.

Credit default swaps (CDS) are not suitable for all investors, and involves the risk of loss. CDS are leveraged investments, and because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money initially deposited for a swap position.

INDEX DESCRIPTIONS

The JP Morgan Emerging Market Bond Index is a benchmark index for measuring the total return performance of international government bonds issued by emerging markets countries that are considered sovereign (issued in something other than local currency) and that meet specific liquidity and structural requirements.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5348 0116 | Tracking #1-458479 (Exp. 01/17)