KEY TAKEAWAYS

· The latest Beige Book suggests that the U.S. economy is still growing near its long-term trend.

· However, Main Street’s latest assessment suggests that the manufacturing sector continues to be affected by oil and energy prices.

· Main Street has remained broadly optimistic despite recent equity market volatility and negative headlines.

BEIGE BOOK SUGGESTS CONTINUED MODEST ECONOMIC GROWTH

During periods of economic volatility, investors sometimes abandon the tools for evaluating markets and the economy that had been serving them well before the volatility started. Good tools, however, should continue to provide insight, which is why we are turning, once again, to the latest Beige Book from the Federal Reserve (Fed) as we gauge the health of the broad U.S. economy as 2015 ended and 2016 began.

The latest Beige Book suggests that the U.S. economy is still growing near its long-term trend, but that the drag from a stronger dollar, weaker energy prices, along with the slowdown in emerging market (EM) economies — most notably China — are still having a major impact on the manufacturing sector. Comments in the Beige Book also continue to indicate that some upward pressure on wages is beginning to emerge; but the wage pressures are not accelerating, which should keep the Fed from raising interest rates aggressively this year. Overall, the Beige Book described the economy as expanding at a “modest or moderate” pace in 9 of the 12 districts. In general, optimism regarding the economic outlook far outweighed pessimism throughout the Beige Book, as it has for the past two years or so.

The Beige Book is a qualitative assessment of the U.S. economy and each of the 12 Fed districts individually. We believe the Beige Book is best interpreted by measuring how the descriptors change over time. The latest edition of the Fed’s Beige Book was released Wednesday, January 13, 2016, ahead of the January 26 – 27, 2016 Federal Open Market Committee (FOMC) meeting, the first Fed policy meeting of 2016. The qualitative inputs for the January 2016 Beige Book were collected from late November 2015 through January 4, 2016. Thus, they captured Main Street’s reaction to:

· A 20%+ drop in the price of oil

· The first Fed rate hike in nine years

· A much warmer (and drier) than usual December that likely impacted holiday shopping

· The terror-inspired shootings in San Bernardino, CA, in early December

· Economic and inflation data for October, November, and December 2015 that were generally softer than expected, especially in the manufacturing sector

· Another bout of equity market volatility in December with several swings of nearly 5%

· Heightened fears of a “hard landing” in the Chinese economy

SENTIMENT SNAPSHOT

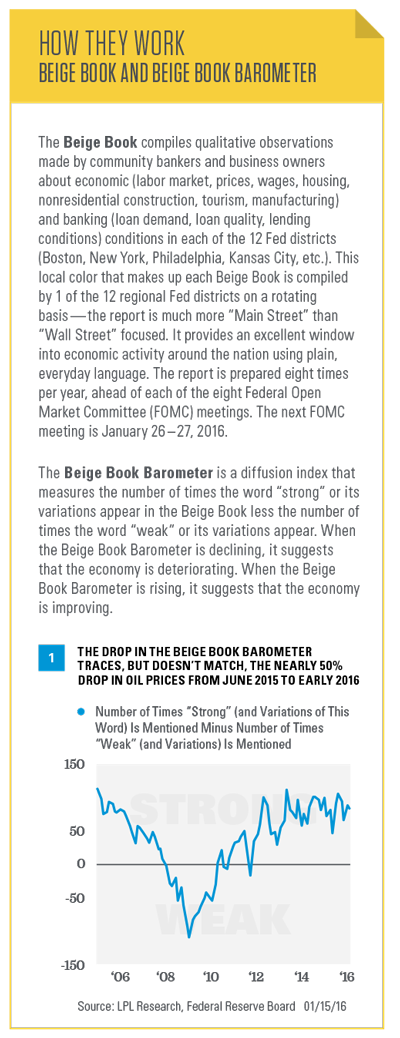

To evaluate the sentiment behind the entire Beige Book collage of data, we created our proprietary Beige Book Barometer (BBB) [Figure 1]. In January 2016, the barometer ticked down to +84 from +89 in October 2015. The BBB is remains below its mid-2015 peak, which followed a 40% bounce in oil prices from March to June 2015. The BBB hit +106 in July 2015, the highest reading since April 2013, and the second-highest reading in over 10 years. The downshift in the BBB from +106 in July to +84 in January 2016 traces, but doesn’t match, the nearly 50% drop in oil prices from June 2015 to early 2016. The +84 reading in January 2016 has been matched just a handful of times in the past 11 years or so, and if sustained, suggests that the U.S. economy is growing at or just above its long-term trend.

WATCHING WAGES & INFLATION

Now that the Fed has initiated its first rate hike cycle since 2006, FOMC members, and, of course, market participants trying to gauge what the Fed may do next, will be watching inflation closely. Each Beige Book provides an economy-wide assessment of wages and prices. Although the January 2016 Beige Book noted that 4 of the 12 districts saw tighter labor markets, they reported “little overall change in wage and price pressures, with wage increases running from flat to moderate, while price increases tended to be minimal.”

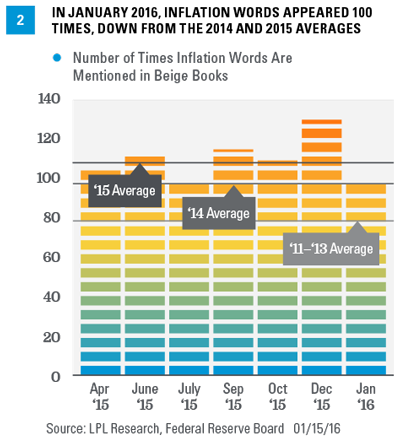

We monitor wage pressures via the data in Figure 2, which shows the recent trend in the number of wage/inflation words in the Beige Book. We counted the number of times the words “wage,” “skilled,” “shortage,” “widespread,” and “rising” appeared in recent editions of the Beige Book. In January 2016, these words appeared 100 times, down from the 120 seen, on average in the final three Beige Books of 2015, and below the 109 average seen in all 8 Beige Books in 2015. In all of 2014 — when deflation, not inflation, was a concern — those words appeared, on average, 98 times per Beige Book; so a drift back toward deflation worries can be seen in the latest Beige Book, and markets are already asking if FOMC members are taking notice. For reference, during 2011 – 13, also a period when heightened risk of deflation was evident, inflation words appeared, on average, 80 times per Beige Book.

COMMENTS ON OIL & ENERGY STABILIZE AT A HIGH LEVEL

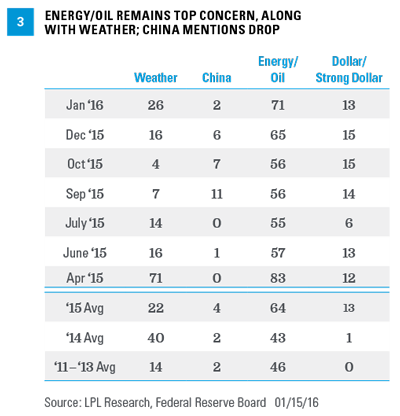

Oil and energy received a total of 71 mentions in the January 2016 Beige Book, the highest reading since the April 2015 Beige Book, which was released at the start of the 40% increase in oil prices between mid-March and mid-June 2015. For context, energy and oil got around 40 – 45 mentions per Beige Book in 2011 – 14 [Figure 3]. Guidance from corporate management in the manufacturing sector, surveys of manufacturing activity, and data on manufacturing orders and shipments continue to be downbeat, and oil has dropped another 20% since data collection for this Beige Book wrapped up on January 4, 2016; thus, absent a sharp rebound in oil prices in the next few weeks, the next few Beige Books are likely to see elevated mentions of oil and energy.

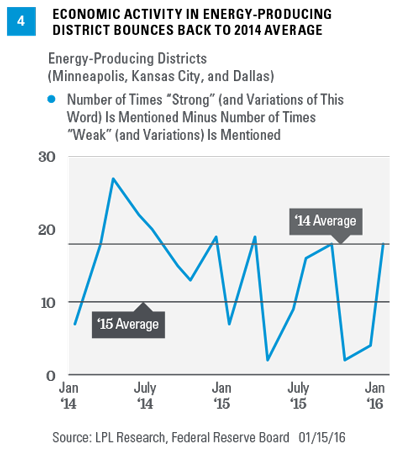

To better gauge the impact of lower oil prices on the economy, we recently constructed a separate Beige Book Barometer [Figure 4] for the three Fed districts with the most energy-related economic activity (Minneapolis, Kansas City, and Dallas). During 2014, the Beige Book Barometer in the energy-related Fed districts averaged +18. In the 8 Beige Books released in 2015, the barometer in the energy-related districts was just +10, a clear deceleration in activity. In January 2016, the reading bounced back up to +18, suggesting more robust activity outside of the energy sector in these districts. Oil prices averaged around $49 per barrel in 2015 — 48% below the 2014 average price of $92 per barrel — so perhaps companies in the oil and gas sector may be throwing in the towel, but it may be too soon to tell. Anecdotes from the Beige Book on energy include contacts in Dallas noting that on the labor front, “the second round of layoffs in the energy sector continued,” and that “there have been some layoffs at companies two to three degrees separated from the oil and gas sector.” Still, we point out that even in places like Texas, Louisiana, and Oklahoma, energy accounts for less than 20% of gross domestic product (GDP). However, in the final four Beige Books of 2015 (July, September, October, and December), the number of weak words in the energy-related Fed districts (72) alone accounted for nearly half of all weak words (164) in the entire Beige Book, indicating that the economic weakness related to the oil and gas sector is still significant.

As was the case in the Beige Books released in 2015, the January 2016 Beige Book provided many comments from all 12 Fed districts about how lower fuel and energy prices were benefiting multiple industries. In short, comments on the impact of falling oil prices are consistent with our view that falling oil prices may be a net plus for the U.S. economy as a whole, but economies in certain states could see a significant impact from the additional slowdown in drilling activity that is likely to occur over the next 6 – 9 months or so.

FADING CONCERNS/RISING CONCERNS

Uncertainty around fiscal policy and the Affordable Care Act has continued to fade as a concern; however, in some cases it has been replaced by uncertainty surrounding China, the drop in oil and other commodity prices, the stronger dollar, and the implications for global growth. There was also an uptick in mentions of weather in the latest Beige Book, with 75% of the 26 mentions of weather in the January Beige Book saying that the warmer than usual weather had a negative impact on activity. Warm weather in the winter hurts holiday sales and winter-related leisure activities like skiing.

Despite the widespread concern in financial markets around the potential impact the equity market and economic turmoil in China may have on the U.S. economy, Beige Book respondents remain largely unconcerned. China had just 2 mentions in the latest Beige Book, well below the 8 China mentions per Beige Book in the late summer and fall of 2015. China averaged only 2 mentions per Beige Book from 2011 – 14. As we noted in the Weekly Economic Commentary, “China Challenge,” while the Chinese economy has been slowing for more than 5 years, the news media and U.S. financial markets have only recently seemed to have taken note. Ironically, both mentions of China in the latest Beige Book were in a positive context

The concerns about a stronger dollar moderated somewhat in the latest Beige Book, but remain elevated relative recent history. There were 18 mentions of the dollar in the January 2016 Beige Book [Figure 3], 13 of which were specifically about the “strong dollar,” below the 25 mentions (15 of them “strong dollar”) in the December 2015 Beige Book.

To put these readings in context, the strong dollar was mentioned, on average, just once per Beige Book in 2014 and in the first few Beige Books of 2015, and got virtually no mentions in 2011 – 13. But since the big run-up in the dollar between late 2014 and early 2015, the dollar has received, on average, 20 mentions per Beige Book. While strong dollar concerns mainly came from manufacturers, retailers who cater to overseas customers and tourism contacts in areas that traditionally attract overseas tourists (New York, Florida, Nevada, and California) also cited the strong dollar as a drag on business.

OPTIMISM STILL RULES

Of the major transitory factors that impacted the economy and the Beige Book in early 2015 (dollar, oil, port strike, bad weather), only oil and the strong dollar remain as concerns. However, neither the dollar nor the other headlines has dampened optimism on the economy, which has picked up strength in the past year or so.

In the January 2016 Beige Book, the word “optimism” (or its related words) appeared 17 times, whereas the word “pessimism” appeared just three times [Figure 5]. In the 9 Beige Books released since early 2015, optimism appeared, on average, 21 times per Beige Book, while the word pessimism has appeared a total of just 8 times, with 5 of the 8 mentions coming in the Dallas and Kansas City districts, who were commenting on the outlook for the oil and gas sector.

As reassuring as it is to see that Main Street can remain optimistic despite the flow of bad news, the large number of optimistic comments in the Beige Book is not the start of a new trend: In the 8 Beige Books released in 2014, the word “optimism” appeared, on average, 30 times. In 2013, “optimism” appeared, on average, 25 times per Beige Book. In the 8 Beige Books released in 2009, during some of the worst of the financial crisis and Great Recession, the word “optimism” appeared, on average, just 9 times.

Concerns that today’s economic and market environment is similar to the onset of the Great Recession and the stock market peak in late 2007 also appear to be misplaced. In the 8 Beige Books released in 2007, the word “optimism” appeared, on average, just 10 times per edition — a far cry from the 30 times per edition in the 8 Beige Books released in all of 2014 and the 21 times per edition in 2015.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful. Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market. Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies. Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.