US Bond Market Week in Review: A Detailed Look at the Long-Leading, Leading and Coincident Indicator

2016 certainly opened with a bang. It started with a massive sell-off in the Chinese market that sent ripples throughout the world. Oil and other commodities continued to plumb new lows. Treasury yields dropped and volatility increased. The combined impact of these events led to an increase in bearish calls for the US economy, which is bolstered by the drop in the Atlanta Fed’s GDP Now and Moody’s High Frequency GDP models. In this article, I’ll take a look at the long-leading, leading and coincident indicators, which will show some weakness exists. But, so far, that weakness is contained within the manufacturing sector, and is caused by the strong dollar, weak oil and weakening emerging economies. In contrast, the US consumer continues to spend on big-ticket items. So long as this behavior continues, we should see at worst, a slight contraction lasting a quarter or two.

The Long Leading Indicators

There are four long-leading indicators: two (corporate profits and Baa bond yields) are showing some weakness but not contraction while the other two (building permits and M2 Y/Y growth are still positive.

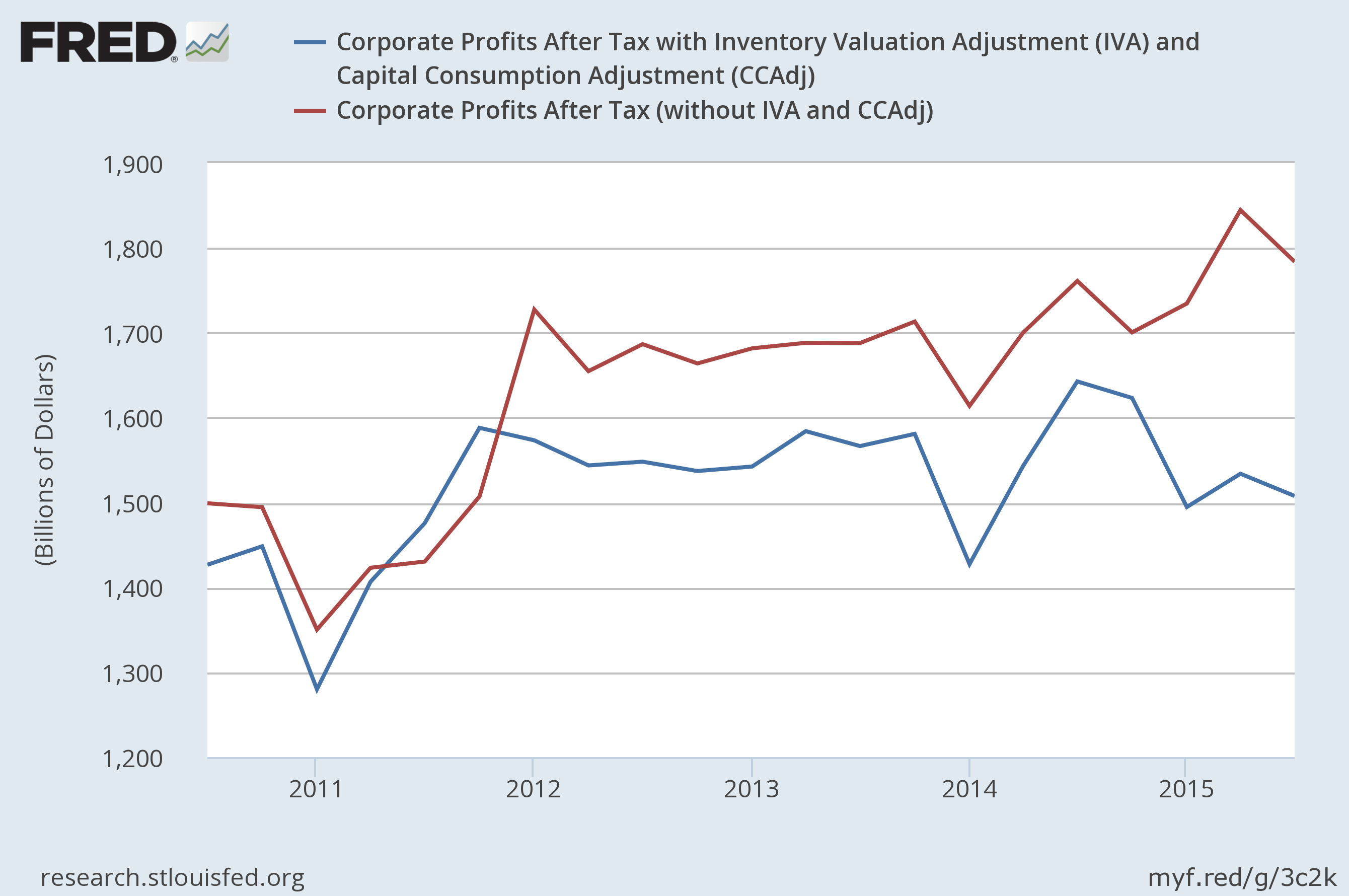

Corporate Earnings

The two charts above contains two data sets: corporate profits after tax with inventory and capital consumption adjustments (in blue) and corporate profits after tax without inventory and capital consumption (in red). The top chart shows the data for the last five years while the bottom shows the last 25 years. Unadjusted numbers increased slightly over the last year while adjusted earnings have not meaningfully increased since approximately 3Q11. Regardless, neither is moving lower yet, which the lower chart shows is required for this data to point towards a recession.

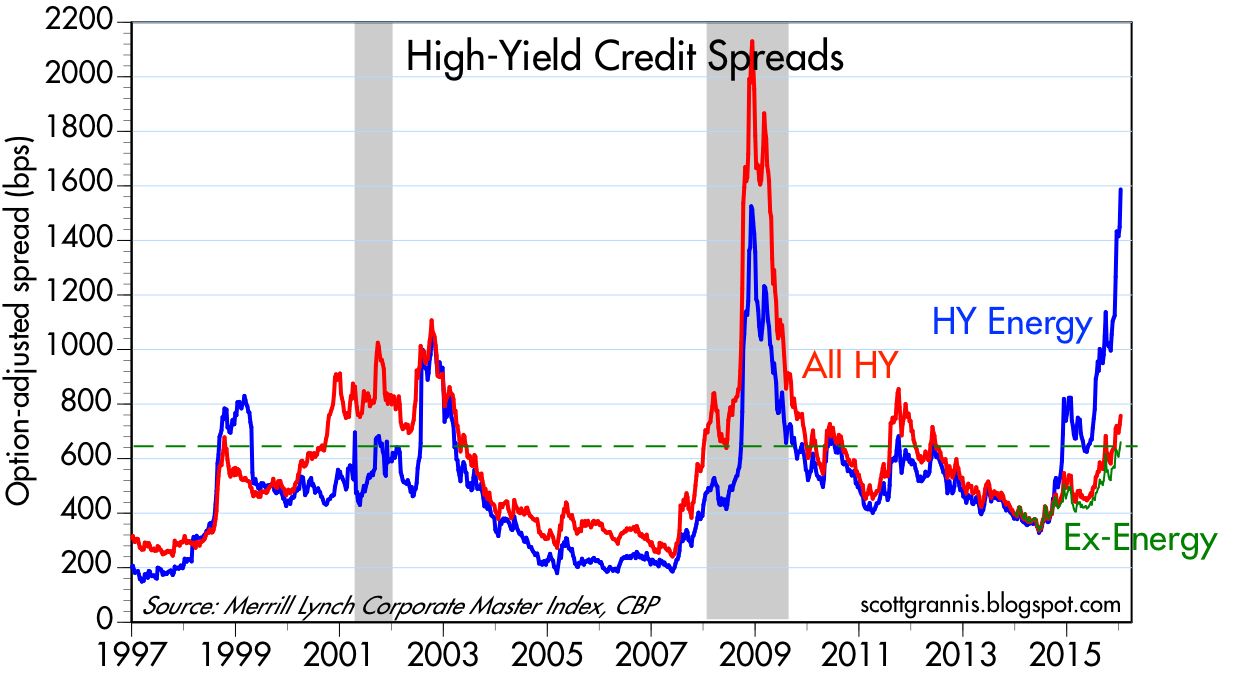

Baa Bond Yields

The top chart shows Baa yields while the bottom (from Scott Grannis) shows not only the entire high yield bond market’s yield, but also the yields for high-yield energy companies. Although many people argue the large increase in junk bond yields will lead to a recession, the bottom chart shows that, so far, the risk is contained within one sector. Additionally, the top chart demonstrates that while the Baa market – which is a bit less risky than junk bonds – has widened a bit, it’s nowhere near recessionary levels. Combined, the two charts denote a market under some stress, but largely due to the impact of one market area (energy).

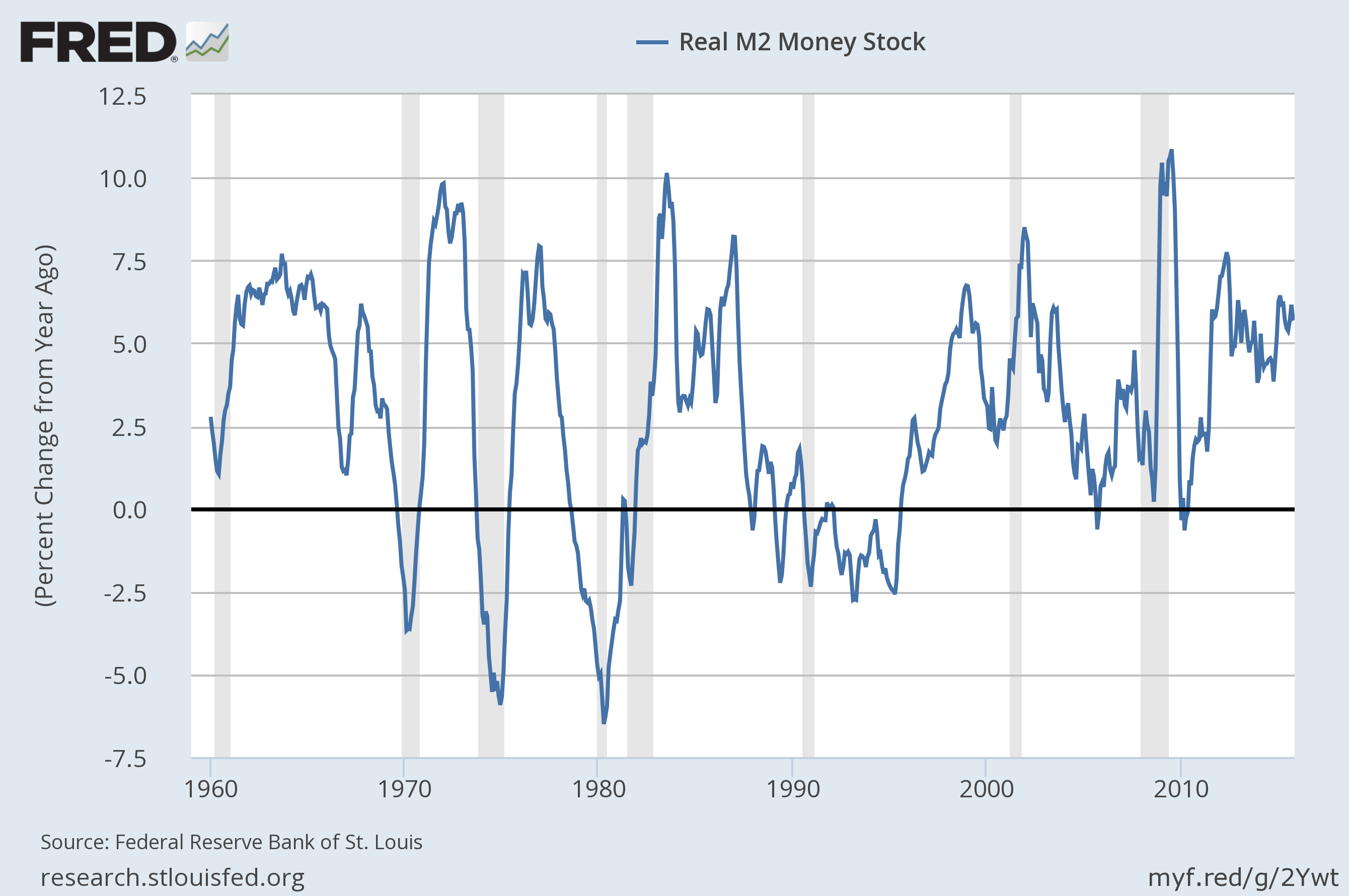

M2

Money growth remains strong. Only when M2 starts to move near 0% Y/Y growth does the economy move closer to a recession.

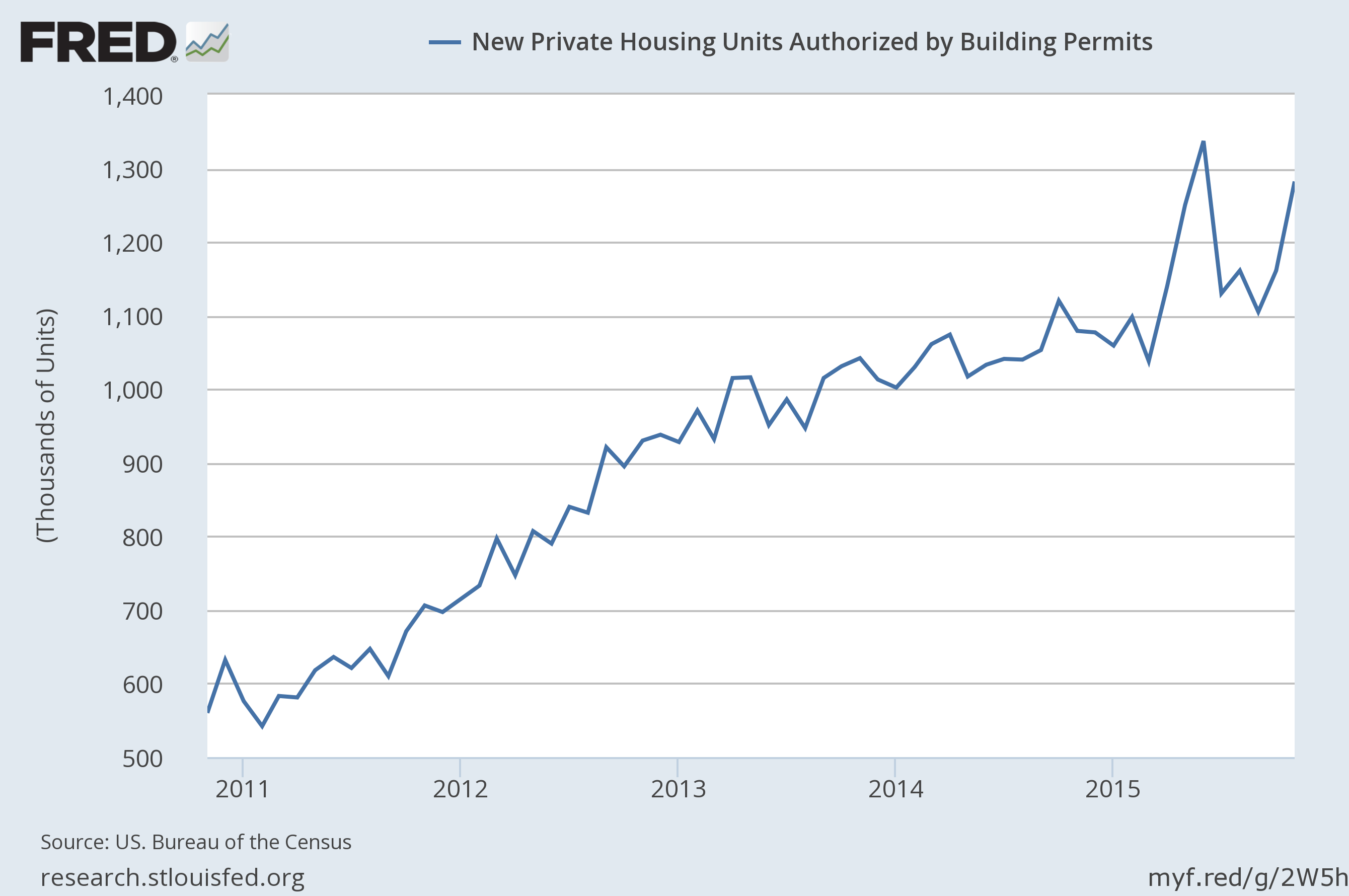

Building Permits

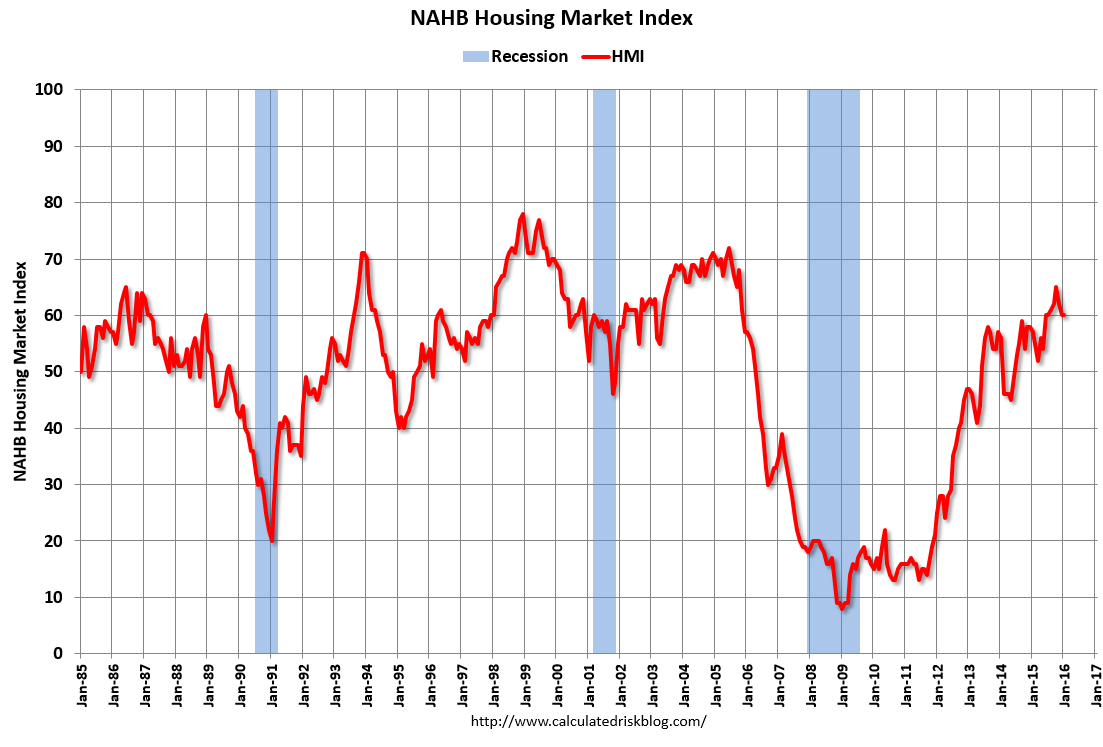

Ed Leamer famously argued that housing is the business cycle; it leads the economy not only into expansion but also into recession. The above chart of building permits shows the home building market continues to grow. The bottom chart (from Calculated Risk) shows homebuilder confidence. Although this index is not a long-leading indicator, it does show the industry is bullish.

Long-leading indicator conclusion: Corporate profits, while stalling, aren’t moving lower. Although energy company junk yields have widened, other segments of the market are still contained. And there is still ample liquidity and housing activity. However, the weakness in two indicators indicates not all is well.

Leading Indicator

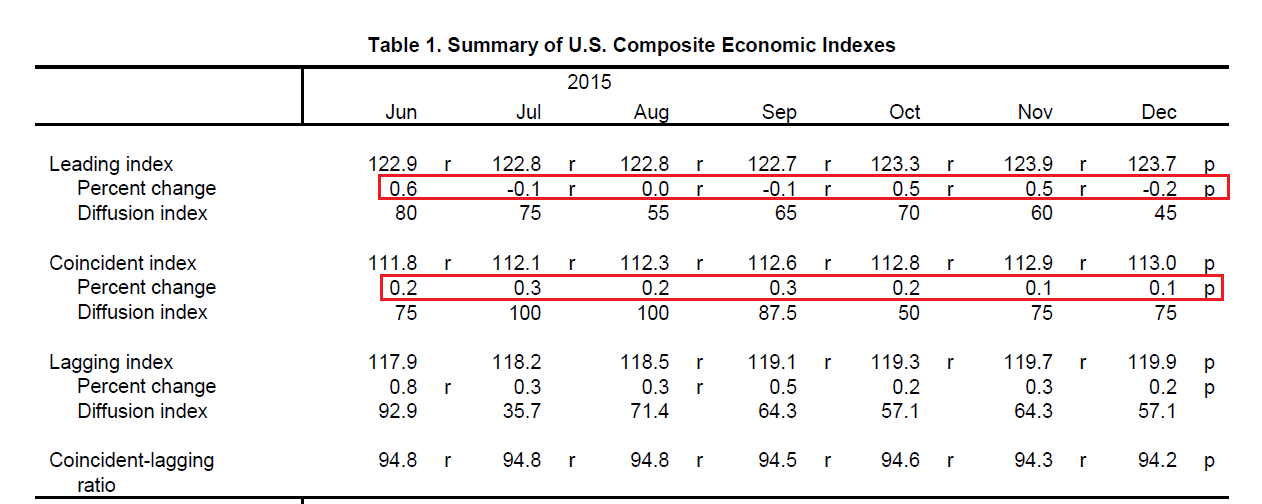

As this table from the latest LEI report shows, the LEIs and CEIs are weakening:

The LEIs have been negative in 3 of the last 7 months and registered a “0” in a fourth. The CEIs, which printed .2%-.3% increases in the June-October period are now printing .1%.

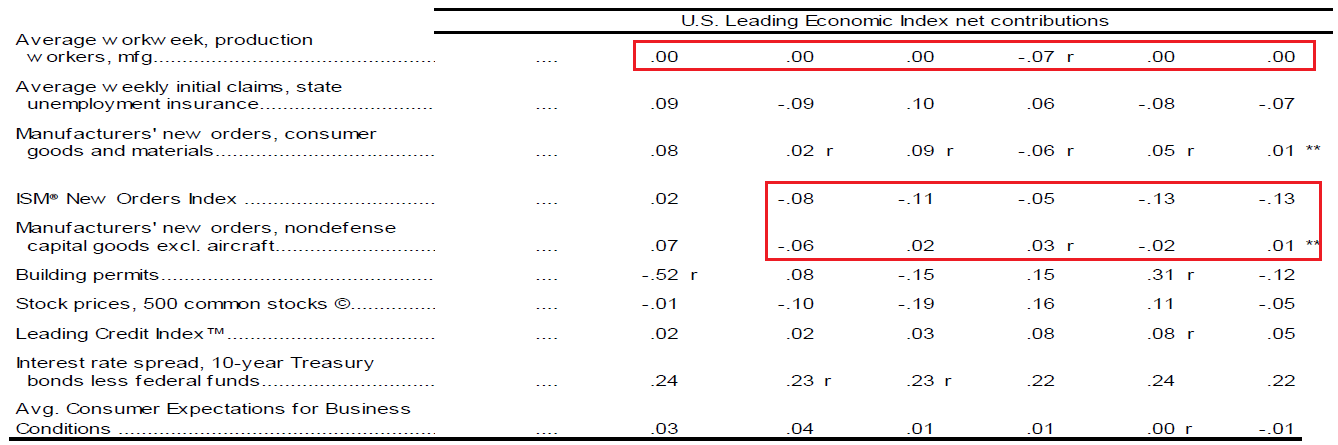

A closer look at the LEIs components shows the negative impact of the recent industrial slowdown:

The average workweek of production workers has printed either “0” or -.7 over the last 7 months. The ISM new orders index and new orders for non-defense goods are also some of the largest contributors.

The CEI components show a similar causation for their weakness:

Industrial and trade sales have been weak for the last six months.

Conclusion: Three things are causing weakness in the economic numbers:

- Oil price declines are lowering demand for oil field equipment as well as increasing the yields on energy sector bonds.

- The strong dollar is lowering demand for US exports

- Weak emerging economies are also lowering export demand.

The US economy experienced a growth recession in the mid-1980s which was caused by a hollowing out of the US mid-west (which later became known as the rust belt). Between the 1Q86 – 1Q87, nonresidential structural investment (CRE) contracted for four quarters while investment in equipment contracted for three. While the economy continued to grow (largely as a result of consumer spending), that expansion was one of the strongest on record. In contrast, the current expansion is one of the weakest.

As with the 1980s expansion, the lynchpin to the current expansion’s growth potential once again rests with the US consumer. And here we have a mixed picture. The Y/Y retail sales growth rate is weak; the latest figures were disappointing. However, auto sales are very strong and the real estate market, while still operating at low levels, continues to recover (see here, here and here). And at some time, people will start to spend at least some of the oil dividend. So long as job growth remains to be strong, consumers should continue buying big ticket items, which may provide just enough growth to keep the economy from experiencing a mild contraction.