Investors who had a hard time finding returns in 2015 might do well to heed the lessons of two other challenging years—1937 and 1987.

Chart 1. For Investors, 2015 Was the Point of Low, or No, Returns

Investment categories with the largest annual return, 1987–2015

Source: Morningstar. Chart depicts the best annual return (calendar year) among the listed groups for the period 1987-2015.

The investment categories listed in this chart are represented by the following indexes: Large Cap Stocks, Russell 1000 Index; Small Cap Stocks, Russell 2000 Index; International Stocks, MSCI EAFE Index; Barclays Agg. (Core Bonds), Barclays Capital U.S. Aggregate Bond Index; High-Yield Bonds, BofA Merrill Lynch U.S. High Yield Master II Constrained Index; Commodities, S&P GSCI Precious Metals Index; Cash, Citigroup 3-Month Treasury Bill Index.

Past performance is not a reliable indicator or a guarantee of future results. The historical data are for illustrative purposes only, do not represent the performance of any specific portfolio managed by Lord Abbett or any particular investment, and are not intended to predict or depict future results.

Indexes are unmanaged, do not reflect deduction of fees and expenses and are not available for direct investment.

As we discussed in the December 31, 2015, Market View, 2015 was a tough year for investors. Many of the major, widely owned asset classes produced flat or negative returns, frustrating investors looking for growth and income. Coupled with a fresh round of market volatility to start 2016 (including a more than 390-point drop in the Dow Jones Industrial Average [DJIA] on January 15), the seeming dearth of reliable sources of investment return is an understandable concern.

Indeed, 2015 was indeed an extremely difficult year when put into historical context. In surveying the performance of major asset classes, a recent cnbc.com article concluded that 2015 was “the hardest year to make money” since 1937.1 This is borne out by an examination of 78 years of data on broad stock, bond, and cash indexes from Ibbotson.

But challenging years like 1937 (and 2015) have been the exception, not the rule. Just because it was hard to make money in 1937 doesn’t mean that you couldn’t make money after 1937. For thisMarket View, we decided to put 2015 into perspective by looking at how the market has responded to past periods of tough times, including how have investors fared since 1937, the previous “worst year.”

First, though, we thought it would be instructive to mount a historical survey from another notable year exactly one half-century later. That would be 1987, which in many respects can be viewed as a defining year for modern financial markets. That was the year of the October 19 Black Monday stock-market crash, the largest ever one-day percentage decline in the DJIA, and arguably when the impact of high-yield bonds, leveraged buyouts, and program trading truly began to be felt in the markets. Using 1987 as a starting point is useful, since the emergence of the high-yield bond market in that decade provides a more direct comparison to the actual investment possibilities available today.

Amid the market turmoil of 1987, was it possible to find decent returns? Yes. Take a look at Chart 1, which features the best performers among major asset classes for the past 29 calendar years. An investment in international stocks in 1987 (as represented by the MSCI EAFE Index) would have provided a return of nearly 25% (after all the volatility, large-cap U.S. stocks, as represented by the Russell 1000 Index, actually gained 2.9%.) As illustrated in Chart 1, 2015 was indeed the worst year for investors during the past 29 years, with none of the listed categories clearing the 1% mark. The next worst year was 2008; but even in that crisis-wracked year, an investment in high-quality bonds (as represented by the Barclays U.S. Aggregate Bond Index) returned more than 5%.

In fact, there were only three years in the survey period (other than 2015 and 2008) in which investors were limited to single-digit returns in even the best-performing investment category. Other than those five total years, investors had the opportunity to realize double-digit returns in some major asset class every year. [Although there is no guarantee that the market will perform in a similar manner under similar conditions in the future.]

Will 2015 prove to be an outlier, with more traditional levels of return once again available to investors in the years ahead? Time will tell, but Chart 1 suggests an important lesson for investors, one that we consider especially important amid the market volatility we’ve seen thus far in 2016. As each traditional category on the chart (other than cash) had a turn at the top of the leaderboard, it becomes clear that amid such historical rotation, the key to positioning a portfolio for strong returns year after year is proper diversification. That way, investors are more likely to have exposure to the best-performing assets in a given year—whatever the category.

Now, let’s return to 1937, the previous return-challenged year cited in the cnbc.com article. There, we’ll find a second lesson regarding the long-term nature of investing and the power of returns over time. What would have happened to the long-term investor who stayed the course after one of the worst-ever years for returns? We’ll illustrate this through a $10,000 investment in a portfolio of 50% large-cap stocks and 50% long-term bonds, two of the few categories for which long-term index data exist. Table 1 shows what happened to that investment over the course of the next five, 10, 20, 40, and 78 years.

Table 1. 1937 Was a Tough Year—What Happened if You Invested Anyway?

Growth of $10,000 for a 50% large-cap stock/50% long-term bond portfolio for indicated periods

Source: Ibbotson. Sample portfolio is composed of 50% Ibbotson SBBI U.S. Large Stock Index and 50% Ibbotson SBBI U.S. Long-Term Government Bond Index. Indexes are unmanaged, do not reflect deduction of fees and expenses and are not available for direct investment.

*Starting 01/01/1938.

Past performance is not a reliable indicator or a guarantee of future results. The historical data are for illustrative purposes only, do not represent the performance of any specific portfolio managed by Lord Abbett or any particular investment, and are not intended to predict or depict future results.

Neither diversification nor asset allocation can guarantee a profit or protect against loss in declining markets.

As eye-popping as the growth is of the original $10,000 for the various intervals shown, the performance is even more impressive in the broader historical context. In 1937, the United States was still struggling to shake off the Great Depression. Five years later, the United States had entered World War II. Ten years later, with the world still rebuilding from the conflagration, America was locking horns with the Soviet Union during the Cold War, with the tension increasing over the ensuing decades.

Forty years later, the U.S. economy was still recovering from the nasty recession of 1973–75, with inflation and unemployment rates remaining stubbornly high. Investors who have been willing to look beyond the negative headlines of past decades to focus on the economy’s longer-run prospects and historical growth trends were handsomely rewarded. That’s a point that should resonate with investors in today’s world.

Using 1987 as a starting point would tell a similar story. An investment of $10,000 would have grown to $32,803 over 10 years, $75,021 over 20 years, and $142,341 as of the end of 2015. [With regard to the historical return data starting in 1937 and 1987 cited above, however, there is no guarantee that markets will perform in a similar manner under similar conditions in the future.]

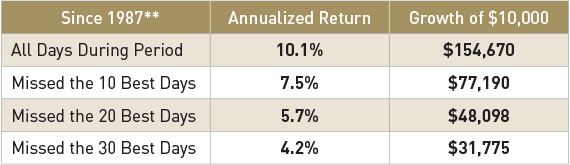

The volatility of 1987 offers us another very important lesson, one that is quite relevant to today’s market: Some of the worst investment decisions are made during difficult times, especially when investors bail out of equities after periods of market downturns. Table 2 provides a clear example of this. Those who stayed fully invested in the market following the 1987 crash benefited from being present for the best-performing days during the following years. Those who were along for only some of those days, or who missed them entirely, realized far lower returns.

Table 2. After 1987, Stock Investors Who Didn’t Stay In Lost Out

Annualized return and growth of $10,000 for indicated periods

Source: Standard & Poor’s and Lord Abbett. Returns are measured based on the S&P 500® Index. The “best” days to be invested are defined as those on which the S&P 500 Index delivered its highest returns for the given periods based on historical data. Annualized return and total return assumes the reinvestment of all dividends and/or capital gains.

**01/01/1988–12/31/2015.

Past performance is not a reliable indicator or a guarantee of future results. The historical data are for illustrative purposes only, do not represent the performance of any specific portfolio managed by Lord Abbett or any particular investment, and are not intended to predict or depict future results.

Indexes are unmanaged, do not reflect deduction of fees and expenses and are not available for direct investment.

In closing, we’ll throw in another lesson: When confronted with a generalization, ask for specifics. The cnbc.com article cited earlier was certainly correct about the lack of return in 2015 in broad, big-picture asset classes. But in narrower areas of the market, solid returns were still available—if you knew where to look. For example, international small-cap stocks (as represented by the S&P Developed ex-U.S. SmallCap Index) returned 5.9%, mega- and large-cap growth stocks (as represented by Russell 1000® Growth Index) returned 5.67%, and municipal bonds (as represented by the Barclays Capital Municipal Index) returned 3.30%. (We’ll spotlight munis in the next Market View.) Active managers who have expertise in a range of investment categories may be uniquely positioned to identify, and capitalize on, specific areas of the market that may provide solid returns in otherwise challenging times.

1 Stephanie Yang, “2015 Was the Hardest Year to Make Money in 78 Years,” cnbc.com, December 31, 2015.

IMPORTANT INFORMATION

The value of investments in equity securities will fluctuate in response to general economic conditions and to changes in the prospects of particular companies and/or sectors in the economy. No investing strategy can overcome all market volatility or guarantee future results. Market forecasts and projections are based on current market conditions and are subject to change without notice. Due to market volatility, the market may not perform in a similar manner in the future. No investing strategy can overcome all market volatility or guarantee future results.

The BofA Merrill Lynch High Yield Master II Constrained Index is a market value-weighted index of all domestic and Yankee high-yield bonds, including deferred interest bonds and payment-in-kind securities. Issues included in the index have maturities of one year or more and have a credit rating lower than BB-/Baa3, but are not in default. The BofA Merrill Lynch U.S. High Yield Master II Constrained Index limits any individual issuer to a maximum of 2% benchmark exposure.

The Barclays Capital Municipal Index is a broad measure of the municipal bond market with maturities of at least one year. To be included in this index, bonds must have a minimum credit rating of at least Baa, an outstanding par value of at least $3 million, and be issued as part of a transaction of at least $50 million. Includes both zero coupon bonds and bonds subject to the alternative minimum tax.

The Barclays Capital U.S. Aggregate Bond Index is an unmanaged index composed of securities from the Barclays Government/Corporate Bond Index, Mortgage-Backed Securities Index and the Asset-Backed Securities Index. Total return comprises price appreciation/depreciation and income as a percentage of the original investment. Indexes are rebalanced monthly by market capitalization.

The Citigroup 3-Month Treasury Bill Index measures monthly return equivalents of yield averages that are not marked to market, utilizing the last three three-month Treasury bill issues.

The Ibbotson SBBI U.S. Large Stock Index is represented by the S&P 500 Composite Index (S&P 500) from 1957 to present, and the S&P 90 from1926 to 1956..

The Ibbotson SBBI U.S. Long-term Government Bond Index is an unweighted index that measures the performance of 20-year maturity U.S. Treasury Bonds.

The MSCI EAFE Index (Europe, Australasia, Far East)is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada. The MSCI EAFE Index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The Russell 1000® Growth Index is an unmanaged index that measures the performance of companies in the Russell 1000 Index considered to have a greater than average growth orientation.

The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

The S&P Developed ex-U.S. SmallCap Index is a geography-specific subset of the S&P Developed SmallCap Index, which comprises the stocks representing the lowest 15% of float-adjusted market cap in each developed country. The S&P Developed SmallCap Index is a subset of the S&P Global BMI, a comprehensive, rules-based index measuring global stock market performance.

The S&P GSCI® is recognized as a leading measure of general price movements and inflation in the world economy. The index representing market beta is world-production weighted. It is designed to be investable by including the most liquid commodity futures, and provides diversification with low correlations to other asset classes.

Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

The opinions in Market View are as of the date of publication, are subject to change based on subsequent developments, and may not reflect the views of the firm as a whole. The material is not intended to be relied upon as a forecast, research, or investment advice, is not a recommendation or offer to buy or sell any securities or to adopt any investment strategy, and is not intended to predict or depict the performance of any investment. Readers should not assume that investments in companies, securities, sectors, and/or markets described were or will be profitable. Investing involves risk, including possible loss of principal. This document is prepared based on the information Lord Abbett deems reliable; however, Lord Abbett does not warrant the accuracy and completeness of the information. Investors should consult with a financial advisor prior to making an investment decision.