Monetary Policy is Only Part of the Solution

In response to the 2008 Financial Crisis, governments around the world led by the U.S. Federal Reserve adopted zero interest rate policy (ZIRP) and quantitative easing (QE) monetary policy tools to try to stabilize the financial system. We believe that these policies have created a high-risk paradigm for investors around the globe who have come to believe that easy monetary policy can drive asset prices higher forever. By failing to understand the growing gap between fundamental value and current market prices, we are concerned investors are at risk of buying high and selling low once again. With the Fed reversing monetary policy for the first time since December of 2008 by raising rates, investors need a reality check. We suggest investors take a quick inventory of where markets are so they can review their assumptions about asset prices before the bubbles start bursting.

“ZIRP and QE”: Not a Panacea

The main ideas behind these policies were to provide excess liquidity to the banking system to foster loan growth and to encourage investors to move into riskier assets, including corporate bonds, high-yield bonds, and stocks with higher yields. The Fed has argued that these policies would create a “wealth effect”, increasing asset prices that would increase consumption and economic growth. With the “ZIRP and QE” monetary policy prescription the Fed has been trying to spur inflation, promote full employment, and generate sustained economic activity.

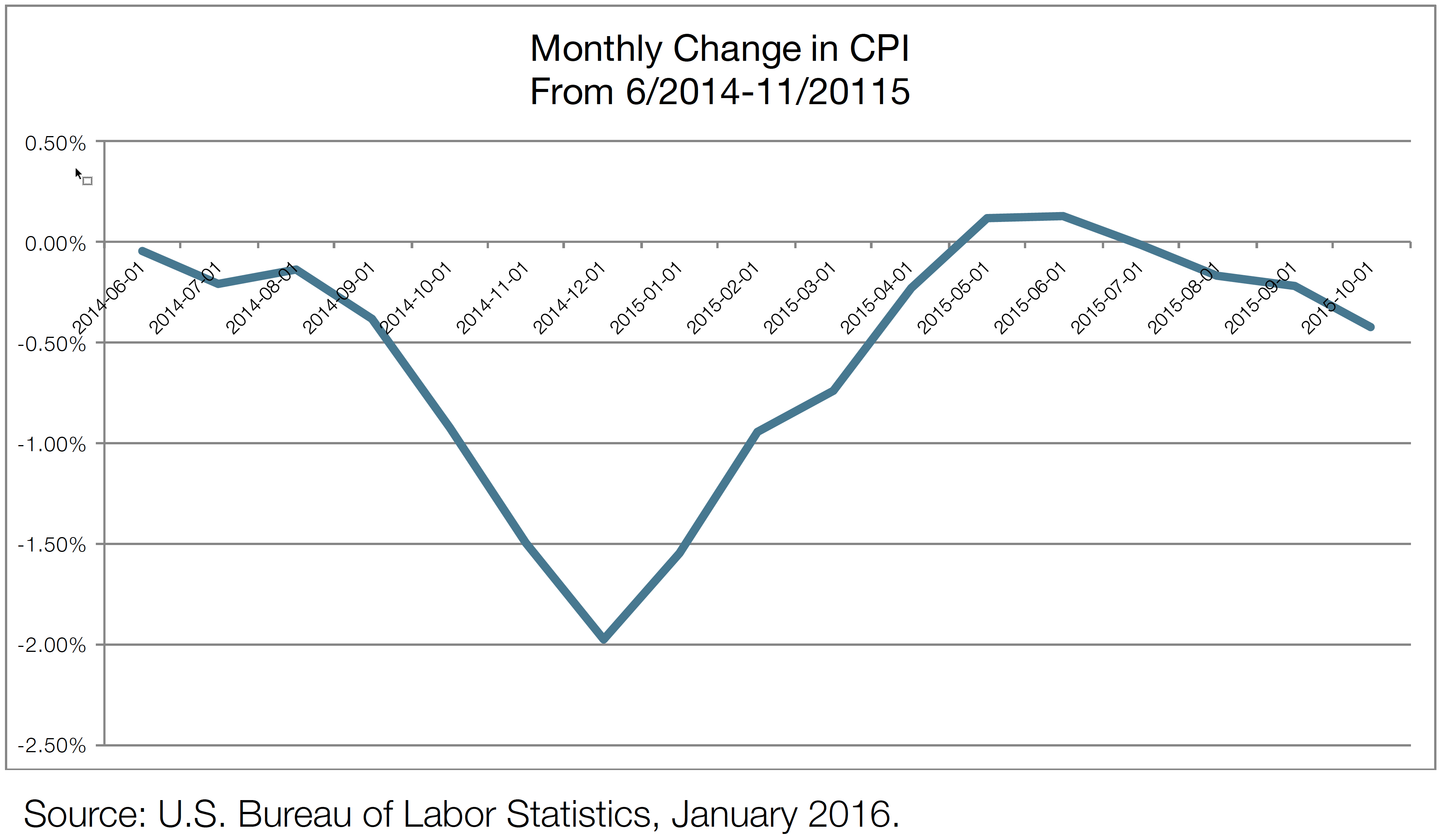

• So far the results seem mixed at best. It’s tough to find inflation, and we seem to be getting farther away from achieving the Fed’s 2% inflation target. The chart shows that inflation over the past 18 months has not been present.1

• While the headline employment statistics have improved dramatically and the “unemployment rate” has fallen nicely, low workforce participation statistics and the low quality of employment continue to create concern over the value of the low 5% unemployment rate.

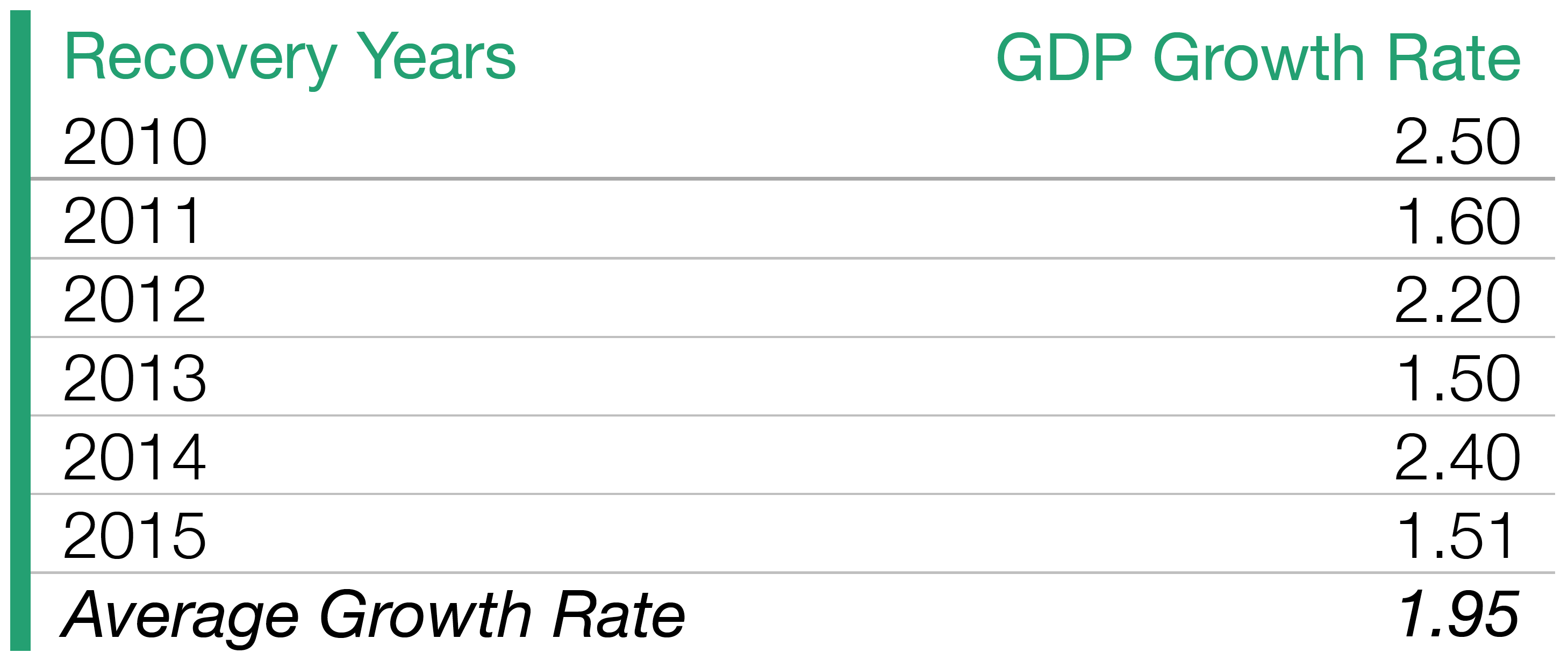

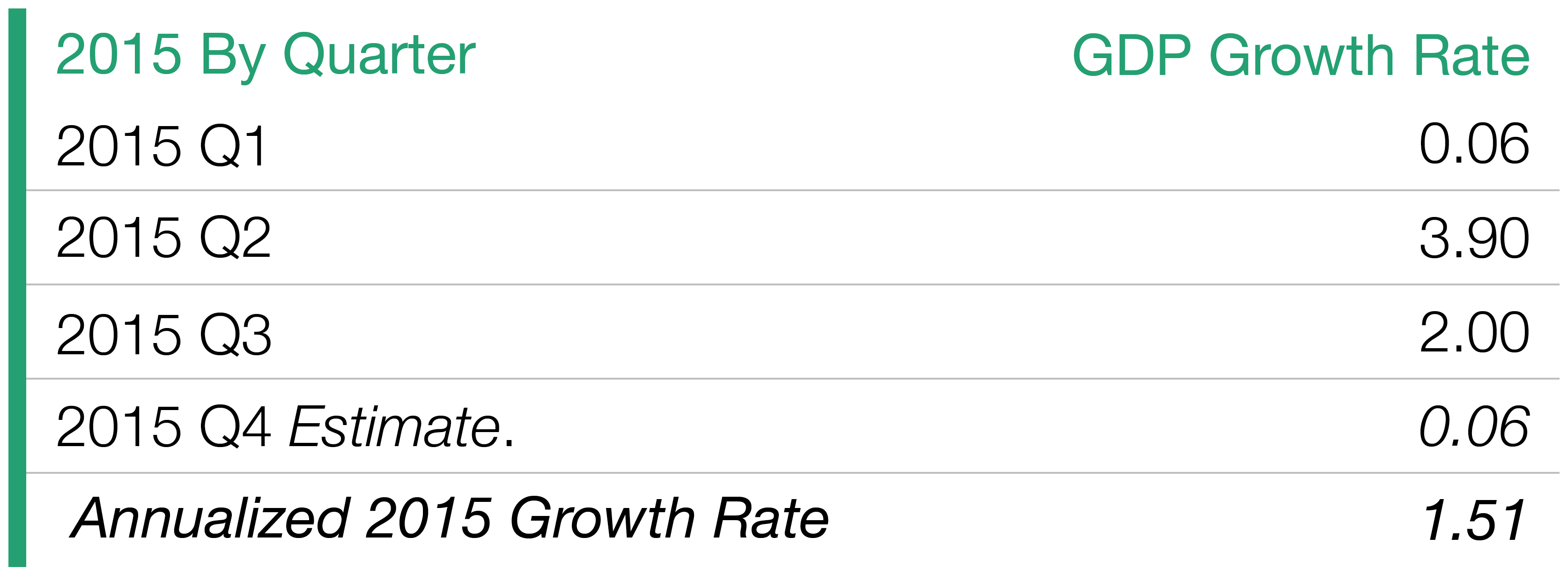

• Economic growth as measured by growth in Gross Domestic Product (GDP) has yet to achieve the 3.00% annualized threshold that many economists believe is the minimum growth rate required to promote a sustained recovery.2 Already the weakest recovery since WWII, growth in GDP has failed to eclipse 2.5% in any calendar year.3 While pundits keep calling for GDP growth to accelerate to 3% and beyond, we fail to see any improvement. In fact, 2015 GDP growth seems to suggest that economic growth may be getting weaker — not stronger — and we believe it is likely to fall below 2%.

Faulty Policy and Decisions at the Fed?

Why would the Fed start raising interest rates now? The Fed has only raised rates to slow down economic growth and inflation when a recovery started overheating. Even though the Fed knows growth is anemic and inflation is low, they have decided to focus on positive, yet we feel misleading, employment statistics to justify raising rates. Do you know the last time the Fed raised rates in a 2% GDP growth environment? Never. And instead of doing their job, we believe they are yielding to political and populace pressure. We believe this policy shift to systematically raise rates not just once but a series of as many as four hikes is not justified by the data, and unless reversed, will ultimately push the U.S. economy into recession.4

The Rest of the World is Struggling5,6

With tepid economic growth, the U.S. economy is still posting the best performance among developed economies, indicating the economic picture outside the U.S. is far less sanguine. China, once the engine of global growth, has slowed dramatically. While it’s tough to get valid economic growth statistics because the economy is centrally controlled by the communist party, their market and currency turmoil is a good indication that the economy has significantly slowed and may be on the verge of entering into recession.

The Euro Zone is trying to stimulate their collective economies to prevent them from falling back into recession and deflation by using the same monetary policies, ZIRP and QE, that have provided the U.S. with some questionable results. Germany, once the growth leader of the region, is experiencing slowing growth which is not good news for the Zone’s prospects. After mounting the best recovery in Europe, the UK has begun to show signs of weakness, especially in its overheated property sector that provided much of its growth impetus.

Japan is making a last-ditch effort to foster growth with “Abenomics” — a massive stimulus program that combines low interest rates, QE initiatives, and fiscal spending. While the jury is still out, the early results look questionable, showing just how difficult it is to reverse a deflationary trend. Japan’s deflationary problems started when their massively overvalued market bubble burst 27 years ago in 1989. With China and Japan struggling to find growth, other Asian economies’ growth rates have been impacted because demand is being curtailed from their biggest trading partners.

Emerging market economies are dependent on natural resources to generate economic growth and have contracted at an alarming rate. Commodity prices have collapsed over the past five years as global growth has slowed. The double whammy of lower demand and lower prices have created nearly depression-like conditions for many emerging economies.

What’s the Big Deal about GDP Growth?

Historically, revenue and earnings trends for corporations are directly tied to growth in GDP. The growth in corporate revenue and earnings will approximate the long-run growth rate of GDP. The U.S. had a collapse in revenue and earnings during the recession in 2008 and early 2009 as GDP contracted -0.3% and -2.8%, respectively.7 As the economy started to recover, corporate revenue and earnings also recovered dramatically, but as GDP growth rates have slowed failing to achieve higher levels of annualized growth of 3%, corporate revenue and earnings have contracted. In Q4 of 2014, earnings declined year-over-prior-year quarter by -5.31%, in Q1 2015 by -5.53%, in Q2 2015 by -10.91%, and in Q3 2015 by -14.05% according to Dow Jones S&P 500 Earnings and Estimates Report.5 After four consecutive quarters of negative earnings, investors would normally start to adjust their holdings causing stock prices to fall. But not in 2015 — the S&P 500 Index finished up marginally, including dividends posting a positive return of 1.4%.

A Fundamental Disconnect

We are highly concerned that the disconnect between corporate earnings performance and stock price fundamentals could be reconciled by a significant market correction. By historical measures, this P/E looks extremely overvalued and is counterintuitive against a backdrop of falling earnings and revenue. We believe that investors who have turned a blind eye to the deterioration in the fundamentals and the valuation warning they provide should wake up and reevaluate the risk they are taking. Based on historical stock valuation statistics, we believe price-to-earnings multiples (P/E) on stocks in the U.S. are overvalued by 40-50%.

What’s the Solution?

In an election year, it bears mentioning that adding meaningful fiscal stimulus to our current extremely accommodative monetary base could be the prescription for unleashing the higher rates of growth needed to build a sustainable recovery and the foundation for the next bull market. Unfortunately, political gridlock and dysfunction have prevented the development of the much needed fiscal response to the 2008 Financial Crisis. After seven years of anemic growth, it is becoming clear that we can’t afford to wait any longer. We feel growth in a capitalist economic financial system is the solution to providing a better standard of living and more social benefits to all of its citizens. But without the necessary level of growth, the benefits will fade.

Summing it Up

Sometimes the markets make investing look easy, and that fundamentals don’t matter. We believe that disciplined investing requires strict attention to the fundamental value of the markets and securities you invest in so you don’t get caught up in the insanity of emotionally-biased decision making. We strongly feel that now is the time investors need to reevaluate how much risk they're taking and how willing they are to take another significant loss. Be careful where you invest, find value, and make sure a company’s revenue and earnings trends are positive and support taking a risk. We believe when good value dynamics are not readily available, cash can be a safe haven as market trends turn bearish. Protecting capital from large losses is of paramount importance, but it’s also critical to have a process to reallocate cash to get fully invested when good value fundamentals reappear.

1 US. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items [CPIAUCSL], retrieved from FRED, Federal Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/CPIAUCSL/, January 10, 2016.

2 Lim, Diane. “The Economy is Almost Fully Recovered, but the Federal Budget is Far from Cured.” Committee for Economic Development of The Conference Board. 03 Feb. 2015. Web. 11 Jan. 2016.

3 Rainey, Michael. "The Weakest Economic Recovery Since World War II Putters Along." The Fiscal Times. 30 July 2015. Web. 11 Jan. 2016.

4 Lange, Jason. "Fed May Need to Hike Rates More than Four times This Year: Lacker."Reuters. Thomson Reuters, 07 Jan. 2016. Web. 12 Jan. 2016.

5 Evans-Pritchard, Ambrose. "US Interest Rate Rise Could Trigger Global Debt Crisis." The Telegraph. Telegraph Media Group, 14 Sept. 2015. Web. 12 Jan. 2016.

6 Pettinger, Tejvan. "Emerging Markets Crisis." Economics Help. 28 Jan. 2014. Web. 12 Jan. 2016.

7 U.S. Bureau of Economic Analysis, “National Income and Product Accounts, Third Quarter 2015” news release (December 22, 2015), http://www.bea.gov/newsreleases/national/gdp/2015/pdf/gdp3q15_3rd.pdf.

8 Silverblatt, Howard. “S&P 500 Earnings and Estimate Report." S&P Dow Jones Indices. McGraw Hill Financial, 17 Dec. 2015. Web. 11 Jan. 2016.