Newsletter - Volume 9, No. 1 - January 2016

A belated Happy and Healthy New Year! Now for this NewsLetter’s musings…

BY THE NUMBERS

Some interesting statistics on Long-Term Care (LTC) from Rep. magazine:

Total Spending (2014)..........................................................................................$219.9 Billion

Percent of personal health care spending......................................................................... 9.3%

Lifetime probability of becoming disabled for those over 65............................................... 68%

Ratio of older Americans who will incur more than $25,000 in lifetime out-of-pocket LTC cost......................................................................................................1 in 5

Probability that if you buy a policy with a 90-day elimination period you will use it before you die ...................................................................................................................................... 35%

Probability that a man will need to spend more than one year in a nursing home.............. 22%

Probability that a woman will need to spend more than one year in a nursing home ......... 36%

Ratio of Americans turning 65 who will likely require some form of LTC.........................7 in 10

NOTHING TO ADD

…from my friend Marie.

PACK YOUR PASSPORT

Heads up from Money magazine. It seems that one element of the 2005 Real ID Act scheduled to go into effect in 2016 will result in those state’s driver licenses that fail to meet the Act’s standards no longer being accepted by TSA as proper identification. The article named New York, New Hampshire, Minnesota, and Louisiana as state licenses failing to make the grade. http://www.dhs.gov/secure-drivers-licenses

OUR FAVORITE COMMENT

Also from Money and also my favorite: “So glad the government upheld the Do Not Call Registry [“Stop Spam Texts and Robocalls,” August]. Before the law took effect in 2009 I would get only … five to 10 robocalls a day. Now I get only … five to 10 robocalls per day.”

GLOBAL REALITY

Continuing my soap box comments on the importance of International Investing, below are some statistics from a Fidelity ad.

• 100% of the time over the past 30 years, the top-performing equity market has been outside the U.S.

• 80% of global GDP comes from non-U.S. countries.

• Only 26% of the world’s publically-traded companies are based in the U.S.

SHE DOES IT AGAIN!

Deena has received many accolades over the years and they just keep coming — with good reason — she’s amazing (and I’m not prejudiced).

JUST IN CASE YOU MISSED IT

This is the title of my friend Bob Kronish’s blog. I’ve mentioned Bob’s blog in the past as it often provides a fun and interesting read. This time he has launched a four-part series on aspects of Jewish history. The first one, “What’s the Secret?––Part 1” addresses the extraordinary survival of a Jewish population over so many thousands of years. It’s a fascinating read @ bobkronish.blogspot.com.

WHILE I’M SHARING CONGRATULATIONS

I am happy and proud to say that five of my associates recently passed the grueling CFP Exam. This is pretty impressive, given that the average pass rate has been in the mid-60s.

Aldo Castaneda* Financial Analyst (Miami)

Katherine Sojo Financial Advisor (Miami)

Michael Hoeflinger Wealth Manager (Miami)

Michael Walsh* Financial Analyst (Miami)

Clay Ranck* Financial Analyst (Lubbock)

* Texas Tech Master’s graduates

MAYBE THEY REALLY ARE READY TO HELP …

Identity Theft Tax Tips Available: Special Series to Help Taxpayers Available through January. IRS YouTube Video: “Taxes. Security. Together.” The Internal Revenue Service, state revenue departments, and the tax industry today released the first in a series of special tax tips designed to provide people critical information to help protect their tax and financial data.

The first of the Security Awareness Tax Tip series provides seven ways people can protect their computers, which takes on added importance as people prepare for the holidays and the 2016 tax season approaches. A new tip will be available each Monday through the start of the tax season in January.

...AND WE NEED THE HELP

According to Businessweek, cybercrime costs business almost $450 billion globally each year and $100 billion in the U.S., and those figures are rising. Thanks to DB for the info.

REALLY PROUD

My partner Taylor Gang is chairman of Miami’s Make-a-Wish® Southern Florida. Here are the results of the organization’s recent extraordinary fundraising ball.

More than 850 VIPs attended the mythology-themed InterContinental Miami Make-AWish Ball, which raised over $2.25 million for Make-A-Wish® Southern Florida. The event was hosted by the InterContinental® Miami.

The glamorous celebration featured a special performance by six-time Grammy Award-winning entertainer Marc Anthony, and a return appearance by actress and filmmaker Gabrielle Anwar as celebrity emcee for the fifth consecutive year. The $2.25 million+ raised will grant the wishes of children with life-threatening medical conditions.

FUTURE SHOCK

In 1964 Isaac Asimov published a number of predictions for 2014; here are two of them:

• You will see as well as hear the person you telephone.

• The world population will be 6.5 billion and the U.S. [population] will be 350 million. (The actual figures were 7.1 billion and 317 million, respectively.)

Pretty impressive! Also from AARP The Magazine.

APHORISMS

From my friend Judy:

• A fool and his money can throw one heck of a party.

• If at first you don’t succeed, skydiving is not for you.

• Money isn’t everything, but it sure keeps the kids in touch.

• Artificial intelligence is no match for natural stupidity. “I think congressmen should wear uniforms, you know, like NASCAR drivers, so we could identify their corporate sponsors.”

• The reason politicians try so hard to get re-elected is that they would hate to have to make a living under the laws they’ve passed.

• The latest survey shows that three out of four people make up 75% of the population.

OLD? WHO’S OLD?

From AARP – At what age is a person old?

People in their:

40s said................... 63

50s said................... 68

60s said................... 73

70s said................... 75

I said........................ 95

Aging Gets Easier

Problems with my physical health do not hold me back from doing what I want.

I have more energy now than I expected for my age.

40s ....................58% .................................................24%

50s ....................39% .................................................47%

60s ....................54% .................................................54%

70s ....................69% .................................................64%

I LOVE COMPANY

From AARP The Magazine:

Henry Winkler................... Age 70

Goldie Hawn..................... Age 70

Julie Andrews................... Age 80

EVEN BETTER

GIVE ME A BREAK

From Financial Advisor IQ:

JPMorgan has landed in the crosshairs of the SEC and the CFTC for steering customers into its own proprietary products that often earned the bank higher fees,” the New York Times reports.

According to the SEC, JPMorgan earned $127 million in “ill-gotten gains” by automatically selling its own mutual funds in basic investment portfolios and its own hedge funds — and outside funds that brought the bank placement fees — to its wealthier clients in the company’s private bank business.

And an even more recent story from Reuters:

If you doubt that we need this regulation [the Department of Labor’s fiduciary proposal my Committee for the Fiduciary Standard has been fighting so hard in support of], consider the case of JPMorgan Chase & Co. Just before the holidays, the largest bank in the United States agreed to pay $307 million to settle accusations by the U.S. Securities and Exchange Commission (SEC) that brokers and advisers in several JPMorgan divisions steered clients into its own, more expensive investment products over other choices without making the required disclosures to clients about conflicts of interest.

JPMorgan also gave preference to third-party hedge fund managers who paid placement fees equal to 1 percent of the market value of invested client assets — so-called “retrocession” fees. While clients did not pay those fees directly, this type of arrangement ultimately hurts the investor because it puts a drag on performance.

Finally, the company chose mutual funds with more expensive retail fees over identical — but less expensive — institutional funds.

Even in this light, Congress can’t understand why there needs to be a legitimate fiduciary standard for ALL advisors who provide any form of investment advice? At the end of this NewsLetter I’ve attached a copy of our Committee for the Fiduciary Standard’s Oath. For your own protection, ask whoever your current or prospective financial advisor to sign it.

TO ADD INSULT TO INJURY

A major argument by the large financial services firms against the Department of Labor’s fiduciary proposal is that it would reduce access to advice for small clients; for example:

SIFMA agrees with the DOL that more can be done to help Americans save for retirement and that there should be a best interests standard in place. However, the rule as written completely misses the mark. SIFMA’s comments reflect our ongoing concerns that the DOL’s proposal would cause harm — particularly to low and middleincome retirement savers — by limiting investors’ access to choice and guidance, while raising the cost of saving.

This theme of “eliminate advice for small clients” is one of the core arguments by those objecting to the DOL’s efforts. For example, Congresswoman Wagner commented, “As a result, the ability of low and middle-income Americans to receive affordable financial advice for their retirement is now in jeopardy.”

Unfortunately, at least some of the member firms seem to have missed that objection.

From Financial Advisor IQ:

Wells Fargo is using carrots rather than sticks to get its brokers to shed smaller accounts, WealthManagement.com reports. The wirehouse is offering to pay bonuses to those who transfer their smaller clients to advisor trainees. Established producers who have larger ratios of accounts worth $250,000 or more can also receive bonuses.

Wells Fargo FAs will be paid 12-month trailing gross production or 40 basis points, whichever is greater, for transferring accounts with less than $65,000 in household assets to a Wells Fargo “financial relationship advisor,” a new designation for trainees looking to build their books with qualifying leads, the company tells WealthManagement.com.

Last year Reuters reported:

Three years ago Merrill eliminated pay for new households with less than $250,000 but “grandfathered” existing small accounts. It will now pay nothing on the grandfathered accounts, which comprised about 1 percent of client assets, or $20 billion, Merrill brokerage head John Thiel told Reuters last summer.

In fact, large brokerage firm rejection of “small” accounts is not new. Here’s a Forbes story from January 2012:

Brokerage firms like Merrill Lynch and Morgan Stanley Smith Barney tweak their compensation plans for their financial advisors about once a year. At Bank of America Merrill Lynch this year’s tweak increased the client account minimum $250,000 from $100,000. That means Merrill brokers won’t be paid to give financial advice to new clients who have less than $250,000 in assets. (The exception is on already existing clients that fall under $250k.)”

And six years ago from Financial Advisor:

“Broker Firms Getting Rid of ‘Little Guy’”

(Dow Jones) Size does matter when it comes to investors’ assets. And brokerage firms are implementing new programs that push their financial advisors to get rid of at least some small clients.

By reducing their concentration of small households by 1%, advisors can increase their production by $7,700, according to a study by PriceMetrix, a wealth management software provider.

The study looked at 15,000 advisor books at 15 of its brokerage firm clients and the ways in which the firms are attempting to decrease their percentage of client households with less than $100,000 in investable assets.

I might add, senior executives of all of these firms sit on the SIFMA Board.

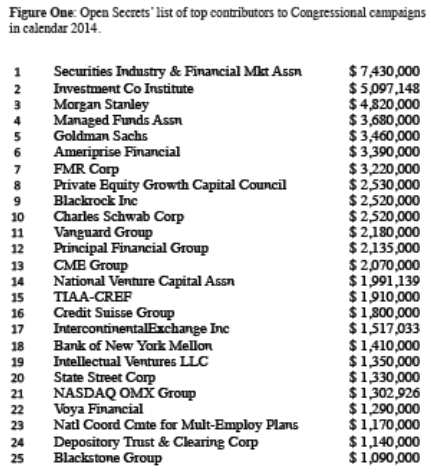

GOLLIATH KNOWS HOW TO SPEND ITS PROFITS

From my friend Bob Veres’ most excellent mock trial “The Case against Wall Street” http://www.advisorperspectives.com/articles/2015/12/22/the-case-against-wall-street:

AMERICANS ARE GIVING PEOPLE

From Investment Advisor:

Americans gave an estimate $358 billion(!!) to charity in 2014, breaking the record set before the Great Recession. Of this, 72% was from individuals, 15% was from foundations, 8% was from bequests, and 5% was from businesses.

• Religion $114.9 billion

• Education 54.6

• Foundations 41.6

• Human Services 42.1

• Health 30.4

• Public-Society Benefit 26.3

• Arts/Culture/Humanities 17.2

• International Affairs 15.1

• Environmental/Animals 10.5

WHAT EVER HAPPENED TO THESE PRODCTS?

From my friend Peter:

HOW DO INSTITUTIONS SELECT MUTUAL FUNDS FOR THEIR 401K PLANS?

From Planadviser, the top 20% criteria:

Top Criteria:

• 80.2% .....................Performance vs. Benchmark

• 61.2% .....................Performance (five-year returns)

• 41.5% .....................Fee structure for plan

• 36.0% .....................Sharpe ratio (Risk-adjusted return)

Bottom

• 8.9% .......................Brand

• 12.5% .....................Advisor support

• 16.7% .....................Performance (one-year return)

Interesting, but missing our primary criteria — philosophy, process, & people.

GOOD BYE 2015

February 2 10-Year Treasury yield hits a new low at 1.67%.

August 11 China abruptly devalues its currency to stimulate its slowing economy.

August 25 U.S. stocks bottom after a 12% correction sparked by fears about slowing global growth.

November 13 ISIS-linked terrorists kill 129 people in multiple attacks across Paris.

December 11 WTI crude oil hits a six-year low of $35.62 a barrel. The price plunged 33% in 2015.

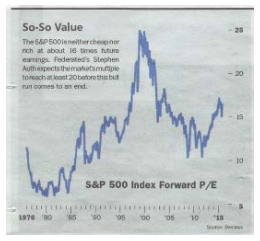

Looks a tad more rich than cheap to me.

Barron’s 12/14/15

HELLO 2016

“Bullish, but Cautious”: A few examples of 2016 Year-End S&P 500 estimates from Barron’s top strategist.

The Optimist Stephen Auth, Federated Investors 2500

The Pessimist David Kostin, Goldman Sachs 2100

In-Between

Jonathan Glionna, Barclays Capital 2200

Dubravko Lakos-Bujas, JPMorgan 2200

Savita Subramanian, BOA/Merrill Lynch 2200

Tobias Levkovich, Citi Research 2200

Adam Parker, Morgan Stanley 2175

Russ Koesterich, Blackrock 2175

Barron’s 12/14/2015

I LIKE IT!

Also from Planadviser:

According to an Allianz study, 92% of Americans working with a financial advisor say that person is helping them reach their financial goals and 86% say their advisor relieves the pressure of trying to plan their family’s financial future by themselves. Yes!

A STAR IS BORN

In case you missed it, here is my contribution as Mother Ginger to the Lubbock Ballet and Symphony’s Nutcracker Ballet:

I FEEL BETTER

Eight billion! According to AARP, this is the number of times Americans collectively check their phones EACH DAY! The average person takes a look 46 times per day. Turns out I’m a piker.

FINALLY!!!

The book everyone has been waiting for is here!!!

I’ve been talking about writing a book for the public for the last 20+ years. I finally got around to it. My book is titled Hello Harold and, as my intro explains…

Welcome to Hello Harold (that’s me, Harold Evensky). I’ve been a practicing financial planner for more than three decades; financial planning is my avocation as well as my vocation. I’ve had the privilege of participating in the growth of my profession, serving on the national Board of the International Association for Financial Planning, as Chair of the Certified Financial Planning Board, on the International Certified Financial Planning Board of Standards, as well as on advisory boards for Charles Schwab and TIAA-CREF.

In those three-plus decades, I’ve seen a great many changes, not only in the markets but also in how investors — and their advisors — respond to them. Some of those responses make very little sense. Financial planning is a powerful tool that can help you develop and maintain the quality of life you want. Unfortunately, there’s a ton of noise and nonsense foisted on investors that can undermine their financial success.

Maybe you’re one of the many unlucky folks who’ve tried using a broker or financial advisor and wound up with one of the few less than ethical ones who had you invest in easy-answer funds that did more for the advisor’s bottom line than yours. Maybe you decided to go it alone. Unfortunately, investing is not a simple task and without a grasp of the fundamentals many investors wind up making costly mistakes. Although there are innumerable books — many of them very good — designed to help you invest wisely, many are too long, too technical, too boring, too commercial, or too simplistic to hold the reader’s attention.

So it’s my turn. I decided my book would be just right — not too long, not too short, not too technical, not too simplistic, not commercial and, most important, fun to read. Hello Harold gives you the foundation you need to navigate the markets and plan your financial future. I take you along with me on phone calls and meetings, into conferences and classrooms, and let you eavesdrop on my thoughts, conversations, and brainstorming sessions with clients, colleagues, and students. I introduce you to actionable concepts that will make you a far better investor, with a sound plan for your future. You may even have some fun along the way.

Unlike most books you’re familiar with, don’t feel obligated to move from page one through to the end. Each chapter stands on its own, so you can skip and jump to your heart’s content, chasing subjects you find of interest in any order that appeals to you. No matter where you land, whether it’s cash flow, market timing, taxes, or any of myriad essential topics, you’re likely to find something you hadn’t considered before in quite that way. Each chapter is designed to give you insights that will improve your financial bottom line and your chances of achieving your financial goals.

My first draft is now on Amazon. The electronic version is priced at $3.99 in order to encourage as many readers as possible. I’ll have hard copies in late January. If you’d like a copy, please drop me a note.

Again, Happy and Healthy New Year and all my best,

Harold R. Evensky, CFP®, AIF®

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management