U.S. economic growth appears to have shifted to a lower gear in the final months of 2015. It has left many concerned about the well-being of the economy and raised questions about the Federal Reserve’s recent hike of the policy rate. In this context, it is important to note that the recent slowing reflects a lopsided development not a widespread deceleration of economic activity.

Mixed signals are visible in recent economic reports. For example, payroll employment rose 292,000 in December and jobless claims are close to the cycle low, while the Institute of Supply Management’s (ISM) manufacturing barometer indicates a contraction in factory activity. An inventory correction is also underway in the midst of these varied economic messages.

Favorable domestic fundamentals support hiring and consumer spending trends. At the same time, a strong dollar and economic weakness abroad underpin soft factory production numbers and exports. The fourth-quarter deceleration is most likely a passing event, with growth predicted to pick up in 2016.

Key Elements of Forecast

- Consumer spending grew at a modest pace in the fourth quarter after averaging 3.3% in the six months ended September. Auto sales were robust in October and November (averaging 18.2 million units) but slipped in December. Early reports suggest that retail sales this holiday season matched last year’s tally. Online sales appear to have accounted for a large percentage of purchases.

- The ISM factory survey slumped below 50 (readings above 50 denote expanding activity while those below 50 denote a contraction) in both November and December. The weakness reflects the impact of the strong dollar and weak demand from trading partners. History is marked with several occasions when this report signaled a drop in factory activity during non-recessionary periods. Markets will be watching these surveys closely.

- Factory-sector data must be interpreted within the broader framework of the U.S. economy. The manufacturing sector constitutes about 12% of gross domestic product and accounts for 9% of total employment. The U.S. economy is mostly a service economy, and the ISM service sector survey points to an expansion in activity, albeit at a decelerating pace.

- Housing news has been mixed. Sales of new homes advanced in October and November, but the November and December decline in sales of existing homes is disappointing. The Mortgage Purchase Index advanced in October and November, and employment remains strong; both factors support expectations of a better performance for housing.

- U.S. exports fell in October and November, and a near-term turnaround is not expected. Imports have also showed weakness in four of the last five months. Although this is related partly to a smaller oil import bill, imports of non-petroleum goods fell in November. Given the economy’s strength, it should not be surprising to see imports regain some momentum.

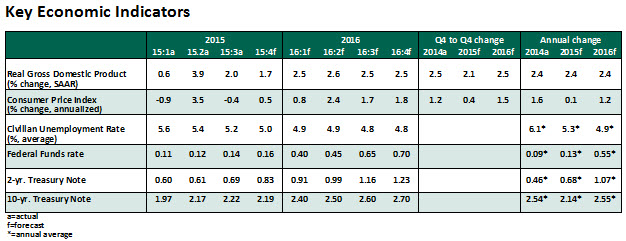

- Inflation remains below the Fed’s 2.0% target. In fact, it has held this position for a little more than three years. Lower oil prices and a strong dollar have prevented higher inflationary pressures. Both these influences are predicted to fade and lift inflation back toward the target. Health care prices are moving up slowly compared with prior experience, and it is another factor that is pushing down overall price measures.

- The labor market continues to show impressive progress. The unemployment rate is at 5.0%, and payroll employment has averaged 284,000 in the last three months, a distinct improvement from the 174,000 average seen in September 2015. A small increase in the labor force participation is expected as discouraged workers re-enter the labor force. Employment compensation has yet to show increases consistent with the age of the expansion and the pace of hiring. The Fed will need to see a trend that is higher than the latest 2.5% increase to be convinced that full employment is at hand.

- The 10-year Treasury note yield has moved down about 15 basis points since the last Fed meeting. The reduction in China’s foreign-exchange reserves to protect the currency had led to questions about U.S. government bond yields, as China is one of the largest holders of these securities. U.S. Treasury securities are the safest in the world, and it is hard to conceive of a sharp increase in yields if China sells its holdings.

- Spillovers from unfavorable economic developments in China present a risk to the forecast. Also, a further appreciation of the dollar could translate into lower import prices and a larger-than-anticipated reduction of exports.

- The Fed is not expected to implement an increase in the federal funds rate at the upcoming meeting on January 26-27. The nature of incoming data and minutes of the December Federal Open Market Committee meeting suggest that the Fed is no rush to normalize interest rates.